UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2022

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to

_____________

Commission File No. 001-39418

Polished.com

Inc.

|

(Exact name of registrant as specified in its charter)

|

|

Delaware |

|

83-3713938 |

(State or other jurisdiction of

incorporation or organization) |

|

(I.R.S. Employer

Identification No.) |

| |

|

|

|

1870

Bath Avenue, Brooklyn, NY |

|

11214 |

| (Address of principal executive offices) |

|

(Zip code) |

| |

|

|

|

800-299-9470 |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b)

of the Act:

|

Title

of each class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which registered |

| Common Stock, par value $0.0001 per share |

|

POL |

|

NYSE American LLC |

| Warrants to Purchase Common Stock |

|

POL WS |

|

NYSE American LLC |

Securities registered pursuant to Section 12(g)

of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). Yes ☐ No ☒

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller

reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated

filer ☐ |

Accelerated

filer ☐ |

| Non-accelerated filer

☒ |

Smaller

reporting company ☒ |

| |

Emerging

growth company ☒ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether

any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the

registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The

aggregate market value of the common stock held by non-affiliates of the registrant was approximately $47.3 million computed by

reference to the closing sale price of the common stock on the New York Stock Exchange on June 30, 2022, the last trading day of the

registrant’s most recently completed second fiscal quarter.

As of July 26, 2023, there were a total of 105,386,867 shares of the

registrant’s common stock issued and outstanding.

Polished.com

Inc.

Annual Report on Form 10-K

Year Ended December 31, 2022

TABLE OF CONTENTS

EXPLANATORY NOTE

Polished.com Inc. (the “Company”) is filing this comprehensive

annual report on Form 10-K for the fiscal years ended December 31, 2022 and 2021 and the quarterly periods ended March 31, 2022, June

30, 2022, September 30, 2022 and March 31, 2023 (the “Comprehensive Form 10-K”) as part of its efforts to become current in

its filing obligations under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Although we have regularly

made filings through current reports on Form 8-K when deemed appropriate, this Comprehensive Form 10-K is our first periodic filing with

the Securities and Exchange Commission (the “SEC”) since the filing of our quarterly report on Form 10-Q for the quarter ended

March 31, 2022 as a result of the matters related to investigation described in this Annual Report under the heading “Item 7

Management’s Discussion and Analysis of Financial Condition and Results of Operation – Investigation”. As a result

of the foregoing, our former auditor withdrew its previously issued audit opinion on our December 31, 2021 consolidated financial statements,

issued on March 31, 2022, and declined to be associated with the quarterly financial statements for the periods ended June 30, 2021, September

30, 2021, and March 31, 2022, filed on August 8, 2021, November 16, 2021 and May 12, 2022, respectively. Included in this Comprehensive

Form 10-K are our audited financial statements for the fiscal year ended December 31, 2022, and our select, unaudited quarterly financial

information for the periods ended June 30, 2022, September 30, 2022 and March 31, 2023, in each case which have not been previously filed

with the SEC.

In addition, the Comprehensive Form 10-K also

restates the Company’s previously issued consolidated financial statements as of and for the fiscal year ended December 31, 2021

(see Note 2, “Summary of Significant Accounting Policies – Restatement,” in “Item 8 Financial Statements

and Supplementary Data”, for additional information), which have been re-audited by our new independent registered public accounting

firm, Sadler, Gibb & Associates, LLC. See Item 9. Changes In and Disagreements with Accountants

on Accounting and Financial Disclosure. The relevant unaudited interim financial information for the period ended March 31, 2022 has also

been restated. See Note 2, “Summary of Significant Accounting Policies – Restatement,” in “Item 8 Financial

Statements and Supplementary Data”, for such restated information.

The impact of the restatement is discussed in detail in this Annual

Report under the headings “Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operation –

Investigation.”

Control Considerations

Management has determined that the Company’s

ineffective internal control over financial reporting and resulting material weaknesses were attributed to: the Company’s lack of

structure and responsibility, insufficient number of qualified resources and inadequate oversight and accountability over the performance

of controls; ineffective assessment and identification of changes in risk impacting internal control over financial reporting; inadequate

selection and development of effective control activities, general controls over technology and effective policies and procedures; ineffective

evaluation and determination as to whether the components of internal control were present and functioning; and the lack of an accounting

system that is required for a company or our size. See Item 9A, Controls and Procedures, for additional information related to these material

weaknesses in internal control over financial reporting and the related remedial measures.

INTRODUCTORY NOTES

Use of Terms

Except as otherwise indicated by the context and

for the purposes of this Annual Report on Form 10-K, the terms “Company,” “we,” “us,” or “our”

refer to Polished.com Inc., a Delaware corporation, and its consolidated subsidiaries, including but not limited to, 1 Stop Electronics

Center, Inc., a New York corporation (“1 Stop”), Gold Coast Appliances, Inc., a New York corporation (“Gold Coast”),

Superior Deals Inc., a New York corporation (“Superior Deals”), Joe’s Appliances LLC, a New York limited liability company

(“Joe’s Appliances”), and YF Logistics LLC, a New Jersey limited liability company (“YF Logistics” and together

with 1 Stop, Gold Coast, Superior Deals, and Joe’s Appliances, “Appliances Connection”), and AC Gallery Inc., a Delaware

corporation (“AC Gallery”).

Cautionary Statement Regarding Forward-Looking

Statements

This report contains forward-looking statements

that are based on our management’s beliefs and assumptions and on information currently available to us. All statements other than

statements of historical facts are forward-looking statements. These statements relate to future events or to our future financial performance

and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance

or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied

by these forward-looking statements. Forward-looking statements include, but

are not limited to, statements about:

| |

● |

delinquency in connection with the filing of our

ongoing SEC reports and the risk that the SEC will initiate an administrative proceeding to suspend or revoke the registration of our

common stock under the Exchange Act due to our previous failure to file such reports or of the NYSE American to delist our stock from

the exchange;

|

| |

|

|

| |

● |

cybersecurity or data security breaches such as

the hacking attack we disclosed in May 2023, the improper disclosure of confidential, personal or proprietary data and changes to laws

and regulations governing cybersecurity and data privacy, including any related costs, fines or lawsuits, and our ability to continue

ongoing operations and safeguard the integrity of our information technology infrastructure, data, and employee, customer and vendor information;

|

| ● | our

ability to acquire new customers and sustain and/or manage our growth; |

| ● | the

effect of supply chain delays and disruptions on our operations and financial condition; |

| ● | our

goals and strategies; |

| ● | the

identification of material weaknesses in our internal control over financial reporting and

disclosure controls and procedures that, if not corrected, could affect the reliability of

our consolidated financial statements and have other adverse consequences such as a failure

to meet reporting obligations; |

| ● | our

future business development, financial condition and results of operations; |

| ● | expected

changes in our revenue, costs or expenditures; |

| ● | growth

of and competition trends in our industry; |

| ● | our

expectations regarding demand for, and market acceptance of, our products; |

| ● | our

expectations regarding our relationships with investors, institutional funding partners and

other parties we collaborate with; |

| ● | fluctuations

in general economic and business conditions in the markets in which we operate; and |

| ● | relevant

government policies and regulations relating to our industry. |

In

some cases, you can identify forward-looking statements by terms such as “may,” “could,” “will,”

“should,” “would,” “expect,” “plan,” “intend,” “anticipate,”

“believe,” “estimate,” “predict,” “potential,” “project” or “continue”

or the negative of these terms or other comparable terminology. These statements are only predictions. You should not place undue reliance

on forward-looking statements because they involve known and unknown risks, uncertainties and other factors, which are, in some cases,

beyond our control and which could materially affect results. Factors that may cause actual results to differ materially from current

expectations include, among other things, those listed under Item 1A “Risk Factors” and elsewhere in this report.

If one or more of these risks or uncertainties occur, or if our underlying assumptions prove to be incorrect, actual events or results

may vary significantly from those implied or projected by the forward-looking statements. No forward-looking statement is a guarantee

of future performance.

The forward-looking statements made in this report

relate only to events or information as of the date on which the statements are made in this report. Except as expressly required by the

federal securities laws, there is no undertaking to publicly update or revise any forward-looking statements, whether as a result of new

information, future events, changed circumstances or any other reason.

Risk Factors Summary

We are subject to a variety of risks and uncertainties

that could adversely affect our business, financial condition and operating results. These risks are discussed in more detail under “Risk

Factors” in Item 1A of this report, but are not limited to, risks related to:

Risks Related to Our Business and Industry

| |

● |

Prior to the filing of this annual report on Form

10-K, we have been delinquent in our SEC reporting obligations for over 12 months. Although we expect to file our periodic reports in

a timely fashion going forward, we cannot provide assurance that our business and the price of our common stock will not be materially

adversely affected by our previous failure to file required periodic reports.

|

| |

|

|

| |

● |

The Investigation and subsequent restatement of our financial statements

has consumed a significant amount of our time and resources and may lead to, among other things, shareholder litigation, loss of investor

confidence, negative impacts on our stock price, a material adverse effect on our reputation, business and stock price and certain other

risks.

|

| |

|

|

| |

● |

Macroeconomic trends including inflation and rising

interest rates may adversely affect our financial condition and results of operations.

|

| ● | Our continued revenue growth will depend upon, among other

factors, our ability to acquire more customers, build our brands and launch new brands, introduce new products or offerings and

improve existing products, and successfully compete in the products and services retail industry, especially in the e-commerce sector. |

| ● | Our business model and growth strategy depend on our marketing

efforts and ability to maintain our brand and attract customers to our platform in a cost-effective manner, including our ability to

develop new features to enhance the consumer experience on our websites, mobile-optimized websites and mobile applications, which we

collectively refer to as our “sites.” |

| ● | We may be unsuccessful in launching or marketing new products

or services, or launching existing products and services into new markets, or may be unable to successfully integrate new offerings into

our existing platform, which would result in significant expense and could adversely affect our results. |

| ● | We have experienced rapid growth since inception, which may

not be indicative of future growth, and, if we continue to grow rapidly, we may experience difficulties in managing our growth and expanding

our operations and service offerings. |

| ● | We depend on our relationships with third parties, and changes

in our relationships with these parties could adversely affect our revenues and profits. We may be unable to expand our relationships

with existing suppliers or source new or additional suppliers, negotiate acceptable pricing and other terms with third-party service

providers, suppliers and outsourcing partners and maintain our relationships with such entities. |

| ● | Our suppliers have imposed conditions in our business arrangements

with them. If we are unable to continue satisfying these conditions, or such suppliers impose additional restrictions with which we cannot

comply, it could have a material adverse effect on our business. |

| ● | We may be unable to optimize, operate and manage the expansion of the capacity of our fulfillment

centers, and our plans to expand capacity and develop new facilities may be adversely affected by global events. |

| ● | Our business is dependent upon our ability to acquire, accurately

value and manage inventory. |

| ● | If we fail to maintain adequate cybersecurity with respect

to our systems and ensure that our third-party service providers do the same with respect to their systems, our business may be harmed. |

| ● | Our internal information technology systems may fail or suffer

security breaches, loss or leakage of data, and other disruptions, which could disrupt our business or result in the loss of critical

and confidential information. |

| ● | Our limited operating history makes it difficult to evaluate

our current business and future prospects and the risk of your investment. |

| ● | Certain of our directors and officers could be in a position

of conflict of interest. |

| ● | We have identified a material weakness in our internal control

over financial reporting and may identify additional material weaknesses in the future or otherwise fail to maintain an effective system

of internal controls, which may result in material misstatements of our financial statements or cause us to fail to meet our reporting

obligations or fail to prevent fraud, which would harm our business and could negatively impact the price of our common stock. |

| |

● |

Our business, financial condition and results

of operations could be adversely affected by disruptions in the global economy resulting from the ongoing military conflict between Russia

and Ukraine.

|

| |

|

|

| |

● |

The ongoing global COVID-19 pandemic and any future pandemics or other public health emergencies, could materially affect our operations, liquidity, financial condition and operating results. |

Risks Related

to Our Indebtedness and Liquidity

| ● | If we require additional financing to fuel our continued

business growth, this additional financing may not be available on reasonable terms or at all. |

| ● | Our current debt and our ability to increase future leverage

could limit our operating flexibility and ability to grow, and adversely affect our financial condition and cash flows. |

Risks Related to Laws and Regulations

| ● | Government regulation of the internet and e-commerce is evolving,

and unfavorable changes or failure by us to comply with existing or future regulations in a cost-efficient manner could substantially

harm our business and results of operations. |

| ● | Failure to comply with applicable laws and regulations relating

to privacy, data protection and consumer protection, or the expansion of current or the enactment of new laws or regulations relating

to privacy, data protection and consumer protection, could adversely affect our business and our financial condition. |

| ● | We may be subject to product liability and other similar

claims if people or property are harmed by the products we sell. The market price, trading volume and marketability of our common stock

may, from time to time, be significantly affected by numerous factors beyond our control, which may materially adversely affect the market

price of our common stock, the marketability of our common stock and our ability to raise capital through future equity financings. |

Risks Related to Ownership of Our Common

Stock

| ● | We

have a limited number of shares of common stock available for issuance, which may limit our

ability to raise capital. |

| ● | We have not paid in the past and do not expect to declare

or pay dividends in the foreseeable future. |

| ● | For as long as we are an “emerging growth company,”

or a “smaller reporting company” we will not be required to comply with certain reporting requirements that apply to some

other public companies, and such reduced disclosures requirement may make our common stock less attractive. |

| |

● |

We may not be able to maintain a listing of our common stock and warrants on NYSE American. |

PART

I

ITEM 1. BUSINESS.

Overview

Our Company is a content-driven

and technology-enabled shopping destination for appliances, furniture and home goods.

Our goal is to give

customers a wide array of choices and a premium experience through detail on the best brands, volume purchasing, and rebates with

manufacturer discounts, supported by human customer service agents.

Corporate History and Structure

Our Company was incorporated in the State of

Delaware on January 10, 2019, to form an acquisition platform. In April 2019, we acquired substantially all of the assets of

Goedeker Television, a brick and mortar operation with an online presence serving the St. Louis metro area. Since that acquisition,

we have grown into a nationwide omnichannel retailer. Through our June 2021 acquisition of Appliances Connection, we have evolved

into a growth-oriented e-commerce platform, offering an expansive selection of household appliances throughout the United States. In

July 2021, we added to our platform by acquiring Appliances Gallery. On July 20, 2022, we changed our corporate name from 1847

Goedeker Inc. to Polished.com Inc. With warehouse fulfillment centers in the Northeast and Midwest, as well as showrooms in

Brooklyn, New York, Largo, Florida and St. Louis, Missouri, we offer one-stop shopping for national and global brands. We carry many

household name-brands, including Bosch, Cafe, Frigidaire Pro, Whirlpool, LG, and Samsung, and many major luxury appliance brands

such as Miele, Thermador, La Cornue, Dacor, Ilve, Jenn-Air and Viking, among others. We also sell furniture, fitness equipment,

plumbing fixtures, televisions, outdoor appliances, and patio furniture, as well as commercial appliances for builder and business

clients.

Key Acquisitions

Acquisition of Goedeker Television

On April 5, 2019, we acquired substantially all

of the assets of Goedeker Television (the “Goedeker Television Acquisition”). As a result of this transaction, we acquired

the former business of Goedeker Television, which was founded in 1951, and continue to operate this business. Prior to the Goedeker Television

Acquisition, we had no operations other than operations relating to our incorporation and organization.

Acquisition of Appliances Connection

Appliances Connection was founded in 1998 and

is one of the leading retailers of household appliances. In addition to selling appliances, it also sells furniture, fitness equipment,

plumbing fixtures, televisions, outdoor appliances, and patio furniture, as well as commercial-grade appliances for builder and business

clients. It also provides appliance installation services and appliance removal services. Appliances Connection serves retail customers,

builders, architects, interior designers, restaurants, schools and other businesses. We completed the acquisition of Appliances Connection

on June 2, 2021, for an aggregate purchase price of $224.7 million, consisting of (i) $180.0 million in cash, (ii) 5,895,973 shares of

the Company’s common stock valued at $12.3 million, and (iii) $32.4 million as a result of the post-closing net working capital

adjustment provision (such acquisition, the “Appliances Connection Acquisition”). We recorded $0.9 million in acquisition-related expenses.

Acquisition of AC Gallery

On July 29, 2021, we acquired substantially all

of the assets of, and assumed substantially all of the liabilities of, Appliance Gallery, Inc., a retail appliance store in Largo, Florida

(“Appliance Gallery”), for a total purchase price of $1.4 million (such acquisition, the “Appliance Gallery Acquisition”).

Name Change

On July 20, 2022, we changed our corporate name from 1847

Goedeker Inc. to Polished.com Inc., pursuant to a Certificate of Amendment to the Amended and Restated Certificate of Incorporation

(the “Certificate of Amendment”) filed with the Delaware Secretary of State on July 20, 2022 (the “Name

Change”). Pursuant to Delaware law, a shareholder vote was not necessary to effectuate the Name Change and the Name Change

does not affect the rights of the Company’s stockholders. The only change in the Certificate of Amendment was the change of

the Company’s corporate name. We also amended and restated our Bylaws on July 20, 2022 to reflect the Name Change and to make

other minor cleanup and conforming changes thereto.

In connection with the Name Change, our common

stock and warrants to purchase common stock ceased trading under the ticker symbols “GOED” and “GOED WS,” respectively,

and began trading on the NYSE American under the new ticker symbols “POL” and “POL WS,” respectively.

Investigation

On August 15, 2022, the Company filed a Form 12b-25

with the Securities and Exchange Commission related to its 10-Q for the six months ended June 30, 2022 reporting that the Audit Committee

had begun an independent investigation regarding certain allegations made by certain former employees related to the Company’s business

operations.

On December 22, 2022, the Company issued a press release stating that

the Board had completed its assessment of the results of the Audit Committee’s previously disclosed investigation. The investigation,

which was supported by independent legal counsel and advisors, produced the following key findings pertaining to the Company’s business

operations under former management during the 2021-2022 period:

| |

● |

The Company was charged by its former Chief Executive Officer approximately $800,000 for expenses unrelated to the Company and its operations. |

| |

● |

The Company appears to not have had in place all the necessary documentation for all of its employees and, in turn, may have failed to comply with certain legal requirements. The Company subsequently put in place enhanced controls to remedy any labor issues, including but not limited to hiring a controller with significant relevant experience, hiring a new human resources director who is leading an overhaul of certain employee policies and initiating the installation of enhanced payroll software that requires all new employees to provide I-9 information and verifies the validity of key information, and believes it is now in full compliance with legal requirements. |

| |

● |

The Company’s controls, software and procedures for managing and tracking inventory, including damaged inventory, were insufficient. The Company subsequently put in place enhanced controls to remedy such issues, including but not limited to initiating the installation of enhanced software and systems for inventory management, ensuring the implementation of standardized policies for the handling and sale of damaged inventory and developing a plan to convert the Company to a new ERP and system for accounting. |

The Company entered into a settlement agreement

with Albert Fouerti, our former Chief Executive Officer, regarding matters relating to the investigation. Among other things, Mr. Fouerti

agreed not to compete for a period of two years following the execution of the settlement agreement.

Resignation of Auditors

On December 20, 2022, the Company received a letter (the “Letter”)

from the Company’s independent registered public accounting firm, Friedman LLP (“Friedman”), informing the Company of

its decision to resign effective December 20, 2022 as the auditors of the Company.

In the Letter, Friedman advised the Company that

based on the results of the Board’s internal investigation as reported to Friedman, it appeared there may be material adjustments

and/or disclosures necessary to previously reported financial information. Additionally, the Board’s internal investigation identified

facts, that if further investigated by Friedman, might cause Friedman to no longer to be able to rely on the representations of (i) management

that was in place at the time Friedman issued its audit report for the year ended December 31, 2021, or (ii) management that was in place

at the time of Friedman’s association with the quarterly financial statements for the periods ended June 30, 2021, September 30,

2021 and March 31, 2022. Prior to the Letter, in the past two years, the Company had not received from Friedman an adverse opinion or

a disclaimer of opinion, and Friedman’s opinion was not qualified or modified as to uncertainty, audit scope, or accounting principles.

The resignation by Friedman was neither recommended nor approved by the Audit Committee or the Board and there were no disagreements with

management and Friedman. Friedman had previously reported a material weakness to the Audit Committee, which was included on the Company’s

Form 10-K for the year ended December 31, 2021, filed on March 31, 2022, regarding the ineffectiveness of the Company’s internal

controls over financial reporting.

In connection with the Letter, Friedman advised

the Company that it was withdrawing its previously issued audit opinion on our December 31, 2021 consolidated financial statements, issued

on March 31, 2022, and declined to be associated with the quarterly financial statements for the periods ended June 30, 2021, September

30, 2021, and March 31, 2022, filed on August 8, 2021, November 16, 2021 and May 12, 2022, respectively.

Engagement of New Independent Registered

Public Accounting Firm

On December 26, 2022, the Audit Committee approved

the engagement of Sadler, Gibb & Associates, LLC (“Sadler”) as the Company’s independent registered public accounting

firm for the fiscal years ended December 31, 2022 and 2021.

Cybersecurity Incident

On March 16, 2023, we experienced a hacking attack

that impacted the check-out page on the Company’s e-commerce website. In response, the Company deployed containment measures, launched

an investigation with assistance from third-party cybersecurity experts and notified appropriate law enforcement authorities. The Company

considers the matter remediated. The investigation determined that certain personal information, including names, addresses, zip codes,

payment card numbers, expiration dates, and CVVs, was extracted from the Company’s systems as part of this incident. The investigation

could not determine with precision which payment card data was included in the timeframe of exposure. Out of an abundance of caution,

the Company notified all payment card users who made transactions on the Company’s e-commerce website within the window of exposure.

As of May 24, 2023, the Company provided appropriate notice to approximately 9,290 individuals, as well as to regulatory authorities in

accordance with applicable law. The Company has incurred, and may continue to incur, certain expenses related to this attack. Further,

the Company remains subject to risks and uncertainties as a result of the incident, including as a result of the data that was extracted

from the Company’s network as noted above. Additionally, security and privacy incidents have led to, and may continue to lead to,

additional regulatory scrutiny. Although we are unable to predict the full impact of this incident, including how it could negatively

impact our operations or results of operations on an ongoing basis, we presently do not expect that it will have a material effect on

the Company’s operations.

The Company has engaged outside consultants through

its outside counsel to help assess and expand the Company’s cyber defenses and payment card protections and policies.

Credit Agreement Amendment

In July 2023, the Company’s lender amended

the credit agreement to waive defaults on the May 9, 2022 credit agreement. The amendment establishes a new EBITDA covenant and requires

the Company to maintain minimum liquidity of $8 million including restricted cash and $3 million excluding restricted cash. Liquidity

as defined in the credit agreement amendment includes cash and certain qualifying customer accounts receivable. The credit agreement amendment

requires the Company to pay the existing loan by August 31, 2024. The Company has begun discussions with investment bankers to place financing

to replace the existing credit agreement by August 31, 2024. See Item 7 “Management’s Discussion and Analysis of Financial

Condition and Results of Operations—Debt.”

Industry

The U.S. major home appliances market is highly

fragmented with big box retailers, online retailers, and thousands of local and regional retailers competing for share in what has historically

been a high touch sale process. According to Statista, revenue in the U.S. major household appliances market (excluding small appliances)

is projected to reach $23.2 billion in 2022 and grow at an annual growth rate of 3.08% from 2022 to 2026.

According to the U.S. Census Bureau, there are

approximately 76 million households in the United States with annual incomes over $25,000 aged between 25 and 65 years, many of whom are

accustomed to purchasing goods online. As younger generations age, start new families and move into new homes, we expect online sales

of household appliances to increase. In addition, we believe the online household appliances market will further grow as older generations

of consumers become increasingly comfortable purchasing online, particularly if the process is easy and efficient.

Our

Products

We sell a vast assortment of household appliances,

including refrigerators, ranges, ovens, dishwashers, microwaves, freezers, washers and dryers. In addition to appliances, we also offer

a broad assortment of products in the furniture, décor, bed & bath, lighting, outdoor living, electronics categories, fitness

equipment, plumbing fixtures, air conditioners, fireplaces, fans, dehumidifiers, humidifiers, air purifiers and televisions. While these

are not individually high-volume categories, they complement the appliance to produce a one-stop home goods offering for customers.

Vendor/Supplier Relationships

We offer more than 400 vendors and over 500,000

SKUs available for purchase through our website. We believe that this depth of vendor relationships gives consumers numerous options in

all product categories resulting in a true one-stop shopping destination. Our principal vendors and suppliers are Dynamic Marketing Inc

(a buying coop), Frigidaire, General Electric, LG, Whirlpool, Bosch, Viking, Miele, Samsung, Fisher Paykel and Ilve.

We are a member and 1.6% equity interest holder

of Dynamic Marketing, Inc. (“DMI”), a 60-member appliance purchasing cooperative. DMI purchases consumer electronics and appliances

at wholesale prices from various vendors, and then makes such products available to its members, who sell such products to end consumers.

DMI’s purchasing group arrangement provides its members with leverage and purchasing power with appliance vendors, and increases

our ability to compete with competitors, including big box appliance and electronics retailers. For the years ended December 31, 2022

and 2021, the Company purchased a substantial portion of finished goods from DMI, representing 69% and 72% of purchases, respectively.

During the year ended December 31, 2022, Dynamic

Marketing Inc accounted for approximately 69% of our purchases; no other vendor accounted for more than 10% of our purchases during the

same period.

Our business model allows us to constantly review

and evaluate each supplier relationship, and we are open to building new supplier/vendor relationships. Products are purchased from all

suppliers on an at-will basis. Relationships with suppliers are subject to change from time to time. Please see Item 1A “Risk

Factors” for a description of the risks related to our supplier relationships.

Marketing

Our marketing efforts drive new and repeat customers

and promote our websites as online communities relating to major appliances and other products. Our strategy is to inspire the customer

at each point of their shopping journey, delivering curated messaging, content and advice in an effort to increase engagement and repeat

purchasing. We utilize a combination of paid and earned media, including search engine marketing, email, digital display, social media,

retargeting, radio and events, in our media strategy. We also have programs to engage appliance enthusiasts and build community through

design and customer portals that are intended both to inspire and provide help the business-to-business (“B2B”) and business-to-consumer

(“B2C”) customers with their projects.

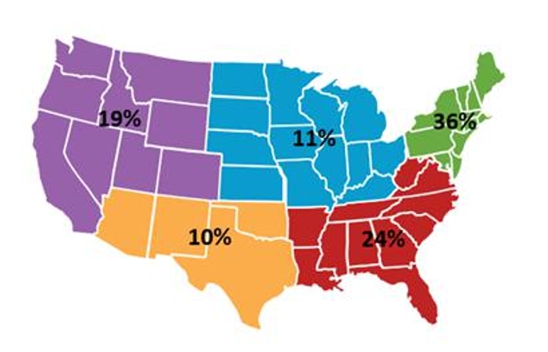

Customers and Markets

We have physical stores and warehouses located in Brooklyn, New York,

Somerset, New Jersey, Hamilton, New Jersey, St. Charles, Missouri and Largo, Florida. Our internal logistics network and third-party distribution,

delivery and installation agreements allow us to serve, sell and ship to customers nationwide. The diagram below represents our sales

by region for 2022:

Logistics

In our fulfillment of large durable goods, we have

created an infrastructure that allows us to deliver products in most states. We want to scale this infrastructure by continuing to improve

execution, fulfillment center locations, and delivery timing. This proprietary logistic process enables us to provide our customers’

products quickly and to provide a better shipping and delivery experience than they might otherwise experience. Additionally, we believe

this logistics network will help us reduce expenses, touchpoints, damages and returns.

Technology

We are continuing to build out our custom-built,

proprietary technology and operational platform to deliver the best experience for both our customers and suppliers. Our success has been

built on a culture of data-driven decision-making and proprietary software for order management and customer fulfillment. We believe that

control of our technology systems, which gives us the ability to update them often, is a competitive advantage. Our team of engineers

has built a technology solution for durable goods. Our software consists of a large set of tools and systems with which our customers

directly interact, that are specifically tuned for shopping the major appliance category by mixing lifestyle imagery with easy-to-use

navigation tools and personalization features designed to increase customer conversion. We have designed operations software to deliver

the reliable and consistent experience consumers desire, with proprietary software enhancing our performance in areas such as integration

with our suppliers, our warehouse and logistics network and our customer service operation. Much of our customer marketing technology

was internally developed, including campaign management and bidding algorithms for online advertising. This allows us to leverage our

internal data and target customers efficiently across various channels. We also partner with select marketing and trade partners where

we find solutions that meet our marketing objectives and inspire our B2B and B2C customers.

Competition

While we are primarily focused on the online U.S.

appliances, furniture and other home goods market, we compete across all segments of the market. Our competition includes online retailers

and marketplaces, furniture stores, big box retailers, department stores and specialty retailers.

Competitive Strengths

The U.S. appliance market is

highly fragmented, with thousands of local and regional retailers competing for a share. We believe this fragmented market presents an

opportunity to streamline business and make brands and products available to everyone across the country. We are standardizing a consistent

end-to-end experience to provide products to the consumer no matter where they are located in the country.

We are strengthening our e-commerce

platform and increasing our showroom and distribution center model to provide a smooth path to purchase. We are also investing in our

brand presence and marketing efforts to drive customer acquisition and engagement. Our goal is to be the appliance destination for our

customers from inspiration to installation.

Our competitive strengths include:

| ● | Name and reputation. In 2022, we introduced our Polished name and continue to build off our

Goedeker legacy in offering competitively priced name-brand products and services, which has been recognized over 50+ years in the

business. |

| ● | Product selection and pricing. Our comprehensive product

selection and competitive pricing model, with support from inspiration to delivery and installation, means we provide a complete solution

for customers. |

| ● | Strong customer relationships. We focus on the needs

and experience of customers, whether they are in the market for a replacement, renovation or new construction project. This customer-centric

approach is evidenced by our repeat customers, over-indexing the industry. |

| ● | Highly trained and professional staff. Our team is

trained to educate and support customers when selecting and buying products. A large percentage of customer orders involve a phone conversation

with a sales team member—a differentiator when competing with online-only companies as well as brick-and-mortar outlets. |

| ● | Website ease of use. Our proprietary, purpose-built

technology platform is designed to provide consumers a compelling user experience as they browse, research and purchase our products.

We use personalization, based on past browsing and shopping patterns, to create a more engaging consumer interaction. |

| ● | Proprietary technology and content. Investments in

our technology platform create a scalable process and support the customer at every point in the journey, including call center tools,

digital marketing optimization, B2B design portals, product reviews and lifestyle content. |

Growth Strategies

Our mission is to change the way consumers buy appliances

and, in doing so, become the leading online retailer of home appliances. The strategies of the Company to achieve this mission, while

increasing value for our stockholders, will include:

| |

● |

Rebrand the combined company. We plan to drive brand awareness through strategic omni-channel marketing. |

| |

● |

Strengthening

the Company’s Leadership Team. We have made significant executive and senior management hires and are continuing to

build our talent pool and hire highly-skilled employees. Recruiting top-tier talent at all levels remains a priority, especially as

the Company evolves and grows. |

| |

● |

Secure design and builder trade business. We have created new tools and benefits to engage and simplify appliance shopping and buying for B2B projects with builders, contractors, architects and interior designers who are making or influencing the purchasing decision for their clients. |

| |

● |

Category expansion and Deeper Connectivity with Customers. We will be adding new, complementary categories and services to our selection to meet our customers’ ever-changing needs. We are in the process of enhancing the content and resources available on our site that will ultimately help us create more meaningful relationships with customers. |

| ● | Drive continued operational excellence. We are committed

to improving productivity and profitability through operational initiatives designed to grow revenue and expand margins. Some of our

key initiatives for operational excellence include: |

| |

o |

Logistics

and shipping optimization. We have identified the geographic areas in which we want to establish a presence to reach more

customers and further penetrate markets that are experiencing high levels of housing development and home remodeling. Although we

currently are holding off on entering into agreements due to inventory and supply chain issues, we expect to add at least two new

fulfillment centers over the next year. We believe that adding fulfillment centers in other parts of the country will

minimize product touchpoints and damage, as well as expedite delivery. With access to vendor warehouse operations, we expect to

capitalize on buying opportunities and capture time-sensitive customers more frequently. |

| o | Price optimization. We are building a data-based understanding of price elasticity dynamics, promotional

strategies and other price management tools to drive optimized pricing for our products. |

Intellectual Property

We own several registered domain names, including

for our www.polished.com website and the Appliances Connection websites www.appliancesconnection.com, 1stopcamera.com, goldcoastappliances.com,

and joesappliances.com. The agreements with our suppliers generally provide us with limited, nonexclusive licenses to use the supplier’s

trademarks, service marks and trade names for the sole purpose of promoting and selling their products.

To protect our intellectual property, we rely

on a combination of laws and regulations, as well as contractual restrictions. We rely on the protection of laws regarding unregistered

copyrights for certain content we create. We also rely on trade secret laws to protect our proprietary technology and other intellectual

property. To further protect our intellectual property, we enter into confidentiality agreements with our executive officers and directors.

As of December 31, 2022, in an effort to protect

our brand, we had three registered trademarks in the United States.

Human Capital

As of December 31, 2022, we employed 391 total

employees, all of which were full-time employees.

We have not experienced any work stoppages and

we consider our relationship with our employees to be good. None of our employees are subject to a collective bargaining agreement or

represented by a labor union. Our people are integral to our business, and we are highly dependent on our ability to attract and retain

qualified personnel.

Government Regulation

Our business is subject to the laws of the U.S.

jurisdictions in which we operate and the rules and regulations of various governing bodies, which may differ among jurisdictions as to

how, or whether, laws governing personal privacy, data security, consumer protection or sales and other taxes, among others, apply to

the Internet and e-commerce. These laws are continually evolving. For example, certain applicable privacy laws and regulations require

us to provide customers with our policies on sharing information with third parties, and advance notice of any changes to these policies.

Related laws may govern the manner in which we store or transfer sensitive information or impose obligations on us in the event of a security

breach or inadvertent disclosure of such information. Additionally, tax regulations in jurisdictions where we do not currently collect

state or local taxes may subject us to the obligation to collect and remit such taxes, or to additional taxes, or to requirements intended

to assist jurisdictions with their tax collection efforts. New legislation or regulation, the application of laws from jurisdictions whose

laws do not currently apply to our business, or the application of existing laws and regulations to the Internet and e-commerce generally

could result in significant additional taxes on our business. Further, we could be subject to fines or other payments for any past failures

to comply with these requirements. The continued growth and demand for e-commerce is likely to result in more laws and regulations that

impose additional compliance burdens on e-commerce companies.

Emerging Growth Company and Smaller Reporting

Company

We qualify as an “emerging growth company”

under the JOBS Act and a “smaller reporting company” within the meaning of the Securities Act. As a result, we are permitted

to, and intend to, rely on exemptions from certain disclosure requirements.

For so long as we are an emerging growth company,

we will not be required to:

| ● | have an auditor report on our internal controls over financial

reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act; |

| ● | comply with any requirement that may be adopted by the Public

Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional

information about the audit and the consolidated financial statements (i.e., an auditor discussion and analysis); |

| ● | submit certain executive compensation matters to stockholder

advisory votes, such as “say-on-pay” and “say-on-frequency;” and |

| ● | disclose certain executive compensation related items such

as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation

to median employee compensation. |

In addition, Section 107 of the JOBS Act also

provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities

Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain

accounting standards until those standards would otherwise apply to private companies. We have elected to take advantage of the benefits

of this extended transition period. Our consolidated financial statements may therefore not be comparable to those of companies that comply

with such new or revised accounting standards.

We will remain an emerging growth company until

the earliest of (i) the last day of the fiscal year following the fifth anniversary of our initial public offering, (ii) the last day

of the first fiscal year in which our total annual gross revenues are $1.235 billion or more, (ii) the date that we become a “large

accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that

is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter or (iv)

the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

We may continue to qualify as a smaller reporting

company if either (i) the market value of our common stock held by non-affiliates is less than $250 million or (ii) our annual revenue

was less than $100 million during the most recently completed fiscal year and the market value of our common stock held by non-affiliates

is less than $700 million. As a result, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements, including,

but not limited to presenting only the two most recent fiscal years of audited financial statements in our Annual Report on Form 10-K

and reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements.

Additional Information About the Company

The following documents are available free of

charge through the Company’s website, www.polished.com: the Company’s annual report on Form 10-K, quarterly reports on Form

10-Q, current reports on Form 8-K, and any amendments to those reports that are filed with or furnished to the Securities and Exchange

Commission (“SEC”) pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”).

These materials are made available through the Company’s website as soon as reasonably practicable after they are electronically

filed with, or furnished to, the SEC. In addition to its reports filed or furnished with the SEC, the Company publicly discloses material

information from time to time in its press releases, at annual meetings of stockholders, in publicly accessible conferences and investor

presentations, and through its website (principally in its News and Investor Relations pages). References to the Company’s website

in this Form 10-K are provided as a convenience and do not constitute, and should not be deemed, an incorporation by reference of the

information contained on, or available through, the website, and such information should not be considered part of this Form 10-K.

ITEM

1A. RISK FACTORS.

An

investment in our common stock involves a high degree of risk. You should carefully consider the following risk factors, together with

the other information contained in this report, before purchasing our common stock. We have listed below (not necessarily in order of

importance or probability of occurrence) what we believe to be the most significant risk factors, but additional risks and uncertainties

not presently known to us or that we currently believe to be immaterial may become material and adversely affect our business. Any of

the following factors could harm our business, financial condition, results of operations or prospects, and could result in a partial

or complete loss of your investment. Some statements in this report, including statements in the following risk factors, constitute forward-looking

statements. Please refer to the section titled “Cautionary Statement Regarding Forward-Looking Statements.”

Risks

Related to our Business and Industry

Prior to the filing of this annual report

on Form 10-K, we have been delinquent in our SEC reporting obligations for over 12 months. Although we expect to file our periodic reports

in a timely fashion going forward, we cannot provide assurance that our business and the price of our common stock will not be materially

adversely affected by our previous failure to file required periodic reports.

Despite the filing of this annual report on Form

10-K, we face a continuing risk that the SEC will initiate an administrative proceeding to suspend or revoke the registration of our common

stock under the Exchange Act due to our previous failure to file quarterly reports on Form 10-Q since March 31, 2022.

Furthermore, the Company is not in compliance

with the continued listing standards of NYSE American LLC (the “Exchange”), as set forth in Sections 134 and 1101 of the NYSE

American Company Guide (the “Company Guide”), since the Company failed to timely file (the “Filing Delinquency”)

its Form 10-Qs for the periods ended June 30, 2022 and September 30, 2022 (collectively, the “Delayed Reports”). The Filing

Delinquency will be cured via the filing of the Delayed Reports. Pursuant to Section 1007 of the Company Guide, the Company

submitted to NYSE Regulation on February 13, 2023 an extension request as the Company was unable to cure the Filing Delinquency within

the initial six-month cure period automatically granted to the Company when it became delinquent. On February 21, 2023, NYSE Regulation

notified the Company that it had accepted the Company’s request to extend the cure period through July 31, 2023. NYSE Regulation

staff will review the Company periodically for compliance with adherence to the milestones in the Company’s plan to regain compliance

If the Company does not make progress consistent with the plan during the plan period or if the Company does not complete its Delayed

Filings with the Securities and Exchange Commission by the end of the maximum 12-month cure period on August 22, 2023, Exchange staff

will initiate delisting proceedings as appropriate. The Company may appeal an Exchange staff delisting determination in accordance with

Section 1010 and Part 12 of the Company Guide.

In addition, there may be continued concern on

the part of customers, investors and employees about our financial condition and extended filing delay status, which may result in the

loss of business opportunities, limitations on our ability to raise capital, including the temporal unavailability of the abbreviated

Form S-3, and general reputational harm. Any of the foregoing could materially adversely affect our business, results of operations, financial

condition and stock price.

The Investigation and subsequent restatement of our financial

statements has consumed a significant amount of our time and resources and may lead to, among other things, shareholder litigation, loss

of investor confidence, negative impacts on our stock price, a material adverse effect on our reputation, business and stock price and

certain other risks.

As described in this Annual Report under the headings

“Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operation – Investigation”

and elsewhere herein, the Company launched an investigation (the “Investigation”) due to certain of the Company’s business

operations under former management during the 2021-2022 period, which resulted in our former auditor withdrawing its previously issued

audit opinion on our December 31, 2021 consolidated financial statements, issued on March 31, 2022, and declining to be associated with

the quarterly financial statements for the periods ended June 30, 2021, September 30, 2021, and March 31, 2022, filed on August 8, 2021,

November 16, 2021 and May 12, 2022, respectively. Consequently, we have restated our previously issued consolidated financial statements

as of and for the year ended December 31, 2021 and for the quarter ended March 31, 2022. See Note 2, “Summary of Significant

Accounting Policies – Restatement,” in “Item 8 Financial Statements and Supplementary Data”, for additional

information.

The Investigation and subsequent restatement process was highly time

and resource-intensive and involved substantial attention from management and significant legal and accounting costs. Furthermore, as

a result of the circumstances giving rise to the restatement, we have become subject to a number of additional risks and uncertainties,

including unanticipated costs for accounting and legal fees in connection with or related to the restatement, shareholder litigation and

government investigations, including potential inquires from the Securities and Exchange Commission (“SEC”) regarding our

financial statements or matters relating thereto. Any such proceeding could result in substantial defense costs regardless of the outcome

of the litigation or investigation and any future inquiries from the SEC as a result of our historical financial statements will, regardless

of the outcome, likely consume a significant amount of our resources in addition to those resources already consumed in connection with

the Investigation and restatement itself. If we do not prevail in any such litigation, we could be required to pay substantial damages

or settlement costs. In addition, the restatement and related matters could impair our reputation and could cause our counterparties to

lose confidence in us. Each of these occurrences could have an adverse effect on our business, results of operations, financial condition

and stock price.

Macroeconomic trends including inflation and rising interest

rates may adversely affect our financial condition and results of operations.

Macroeconomic trends, including increases in inflation

and rising interest rates, may adversely impact our business, financial condition and results of operations. Inflation in the United States

has recently accelerated and is currently expected to continue at an elevated level in the near-term. Rising inflation could have an adverse

impact on our operating expenses and our credit facilities. There is no guarantee we will be able to mitigate the impact of rising inflation.

The Federal Reserve has started raising interest rates to combat inflation and restore price stability and it is expected that rates will

continue to rise throughout the remainder of 2023. Increases in interest rates on any of our debt will result in higher debt service costs,

which will adversely affect our cash flows. We cannot assure you that our access to capital and other sources of funding will not become

constrained, which could adversely affect the availability and terms of future borrowings. Such future constraints could increase our

borrowing costs, which would make it more difficult or expensive to obtain additional financing or refinance existing obligations and

commitments, which could slow or deter future growth.

Our

business is dependent on general economic conditions and consumer discretionary spending, and reductions in such spending might adversely

affect the Company’s business, operations, liquidity, financial results and stock price.

Our

business depends on consumer discretionary spending, and our results are highly dependent on U.S. consumer confidence and the health

of the U.S. economy. Consumer spending may be affected by many factors outside of the Company’s control, including general economic

conditions; consumer disposable income; consumer confidence and perception of economic conditions; the threat or outbreak of war, terrorism

or public unrest (including, without limitation, the conflict in Ukraine) which may cause supply chain disruptions, increase fuel costs

and transportation costs, and create general economic instability; wage and unemployment levels; consumer debt and inflationary pressures;

the costs of basic necessities and other goods; effects of weather and natural disasters caused by climate change or otherwise; and epidemics,

contagious disease outbreaks, and other public health concerns including the COVID-19 pandemic. Adverse economic changes in any

of the regions in which we sell our products could reduce consumer confidence and could negatively affect net revenue and have a material

adverse effect on our operating results.

Consumers

may view a substantial portion of the products we offer as discretionary items rather than necessities. As a result, our results of operations

are sensitive to changes in macro-economic conditions that impact consumer spending, including discretionary spending. Decreases in consumer

discretionary spending may result in a decrease in comparable sales, and average value per transaction, which might cause us to increase

promotional activities, which will have a negative impact on our gross margins, all of which could negatively affect the Company’s

business, operations, liquidity, financial results and stock price, particularly if consumer spending levels are depressed for a prolonged

period of time.

Our

business model and growth strategy depend on our marketing efforts and ability to maintain our brand and attract customers to our platform

in a cost-effective manner, including our ability to develop new features to enhance the consumer experience on our websites, mobile-optimized

websites and mobile applications.

Our

success depends on our ability to acquire and retain customers in a cost-effective manner through marketing efforts and maintenance of

our brand. In order to expand our customer base, we must appeal to and acquire customers who have historically used other means of commerce

to purchase home goods and may prefer alternatives to our offerings, such as the websites of our competitors or our suppliers’

own websites. We have made significant investments related to customer acquisition and expect to continue to spend significant amounts

to acquire additional customers. Our advertising efforts consist primarily of email marketing, online advertisements and promotions,

digital marketing and social media. These efforts are expensive and may not result in the cost-effective acquisition of customers. We

cannot assure you that the net profit from new customers we acquire will ultimately exceed the cost of acquiring those customers through

enhancements to the customer experience on our websites, mobile-optimized websites and mobile operations. If we fail to deliver a quality

shopping experience, or if consumers do not perceive the products we offer to be of high value and quality, we may not be able to acquire

new customers. If we are unable to acquire new customers who purchase products in numbers sufficient to grow our business, we may not

be able to generate the scale necessary to drive beneficial network effects with our suppliers or efficiencies in our logistics network,

our net revenue may decrease, and our business, financial condition and operating results may be materially adversely affected.

We

believe that many of our new customers originate from word-of-mouth and other non-paid referrals from existing customers. Therefore,

we must ensure that our existing customers remain loyal to us in order to continue receiving those referrals. If our efforts to satisfy

our existing customers are not successful, we may not be able to acquire new customers in sufficient numbers to continue to grow our

business, or we may be required to incur significantly higher marketing expenses in order to acquire new customers.

Our

success depends in part on our ability to increase our net revenue per active customer. If our efforts to increase customer loyalty and

repeat purchasing as well as maintain high levels of customer engagement are not successful, our growth prospects and revenue will be

materially adversely affected.

Our

ability to grow our business depends on our ability to retain our existing customer base and generate increased revenue and repeat purchases

from this customer base, and maintain high levels of customer engagement. To do this, we must continue to provide our customers and potential

customers with a unified, convenient, efficient and differentiated shopping experience by:

| ● | providing

imagery, tools and technology that attract customers who historically would have bought elsewhere; |

| ● | maintaining

a high-quality and diverse portfolio of products; |

| ● | delivering

products on time and without damage; and |

| ● | maintaining

and further developing our online and mobile platforms. |

If

we fail to increase net revenue per active customer, generate repeat purchases or maintain high levels of customer engagement, our growth

prospects, operating results and financial condition could be materially adversely affected.

Our

continued revenue growth will depend upon, among other factors, our ability to acquire more customers, build our brands and launch new

brands, introduce new products or offerings and improve existing product.

Maintaining

and enhancing our brands is critical to acquiring and expanding our base of customers and suppliers. Our ability to maintain and enhance

our brands depends largely on our ability to maintain customer confidence in our product and customer service offerings, including by

delivering products on time and without damage. If customers do not have a satisfactory shopping experience, they may seek out alternative

offerings from our competitors and may not return to our sites as often in the future, or at all. In addition, unfavorable publicity

regarding, for example, our practices relating to privacy and data protection, product quality, delivery problems, competitive pressures,

litigation or regulatory activity could seriously harm our reputation. Such negative publicity also could have an adverse effect on the

size, engagement, and loyalty of our customer base and result in decreased revenue, which could adversely affect our business and financial

results. A significant portion of our customers’ brand experience also depends on third parties outside of our control, including

suppliers and logistics providers such as R+L Carriers, AM Home Delivery and other third-party delivery agents. If these third parties

do not meet our or our customers’ expectations, our brands may suffer irreparable damage.

In

addition, maintaining and enhancing these brands may require us to make substantial investments in launching new brands or introducing

new products or offerings, and these investments may not be successful. If we fail to promote, maintain, and improve our brands and products,

or if we incur excessive expenses in this effort, our business, operating results and financial condition may be materially adversely

affected. We anticipate that, as our market becomes increasingly competitive, maintaining and enhancing our brands or products may become

increasingly difficult and expensive. Maintaining and enhancing our brands will depend largely on our ability to provide high quality

products to our customers and a reliable, trustworthy and profitable sales channel to our suppliers, which we may not be able to do successfully.

Customer

complaints or negative publicity about our sites, products, delivery times, customer data handling and security practices or customer

support, especially on blogs, social media websites and our sites, could rapidly and severely diminish consumer use of our sites and

consumer and supplier confidence in us and result in harm to our brands.

We

may be unsuccessful in launching or marketing new products or services, or launching existing products and services into new markets,

or may be unable to successfully integrate new offerings into our existing platform, which would result in significant expense and may

not achieve desired results.

Our

business success depends to some extent on our ability to expand our customer offerings by launching new brands, products and services

and by expanding our existing offerings into new markets. Launching new brands and services or expanding geographically requires significant

upfront investments, including investments in marketing, information technology and additional personnel. We may not be able to generate

satisfactory revenue from these efforts to offset these costs. Any lack of market acceptance of our efforts to launch new brands, products

and services or to expand our existing offerings, or failure to successfully integrate new offerings into our existing offerings, platforms,

and markets, could have a material adverse effect on our business, prospects, financial condition and results of operations. Further,

as we continue to expand our fulfillment capability or add new businesses with different requirements, our logistics networks become

increasingly complex and operating them becomes more challenging. There can be no assurance that we will be able to operate our networks

effectively.

We

have also entered and may continue to enter into new markets in which we have limited or no experience, which may not be successful or

appealing to our customers. These activities may present new and difficult technological and logistical challenges, and resulting service

disruptions, failures or other quality issues may cause customer dissatisfaction and harm our reputation and brand. Further, our current

and potential competitors in new market segments may have greater brand recognition, financial resources, longer operating histories

and larger customer bases than we do in these areas. As a result, we may not be successful enough in these newer areas to recoup our

investments in them. If this occurs, our business, financial condition and operating results may be materially adversely affected.

We

have experienced rapid growth since inception, which may not be indicative of future growth. If we fail to manage our growth effectively,

we may experience difficulties in expanding our operations and service offerings and our business, financial condition and operating

results could be harmed.

To

manage our growth effectively, we must continue to implement our operational plans and strategies, improve and expand our infrastructure

of people and information systems and expand, train and manage our employee base. We have rapidly increased employee headcount since

our inception to support the growth in our business. To support continued growth, we must effectively integrate, develop and motivate

a large number of new employees. We face significant competition for personnel and increased labor shortages. Failure to manage our hiring

needs effectively or successfully integrate our new hires may have a material adverse effect on our business, financial condition and

operating results.

Additionally,

the growth of our business places significant demands on our operations, as well as our management and other employees. Surges in online

traffic and orders associated with any promotional activities or new brand or product offerings could place increased strain on our operations,

including our logistics network, and may cause or exacerbate slowdowns or interruptions. The growth of our business may require significant

additional resources to meet these daily requirements, which may not scale in a cost-effective manner or may negatively affect the quality

of our sites and customer experience. We are also required to manage relationships with a growing number of suppliers, customers and

other third parties. Our information technology systems and our internal controls and procedures may not be adequate to support future

growth of our supplier and employee base. If we are unable to manage the growth of our organization effectively, our business, financial

condition and operating results may be materially adversely affected.

Our

business, and e-commerce generally, is highly competitive. Competition presents an ongoing threat to the success of our business.

Our

business is rapidly evolving and intensely competitive, and we have many competitors in different industries. Our competition includes

furniture stores, big box retailers, department stores, specialty retailers, and online retailers and marketplaces in the United States.

We

expect competition in e-commerce generally to continue to increase. We believe that our ability to compete successfully depends upon

many factors both within and beyond our control, including:

| ● | the

size and composition of our customer base; |

| ● | the

number of suppliers and products we feature on our sites; |

| ● | our

selling and marketing efforts; |

| ● | the

quality, price and reliability of products we offer; |

| ● | the

convenience of the shopping experience that we provide; |

| ● | our

ability to distribute our products and manage our operations; and |

| ● | our

reputation and brand strength. |

Many

of our current competitors have, and potential competitors may have, longer operating histories, greater brand recognition, larger fulfillment

infrastructures, greater technical capabilities, faster and less costly shipping, significantly greater financial, marketing and other

resources and larger customer bases than we do. These factors may allow our competitors to derive greater net revenue and profits from

their existing customer base, acquire customers at lower costs or respond more quickly than we can to new or emerging technologies and

changes in consumer habits. These competitors may engage in more extensive research and development efforts, undertake more far-reaching

marketing campaigns and adopt more aggressive pricing policies, which may allow them to build larger customer bases or generate net revenue

from their customer bases more effectively than we do.

Our