UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

PROXY STATEMENT PURSUANT TO SECTION 14(A)

OF THE SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ |

Preliminary Proxy Statement |

| ¨ |

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| x |

Definitive Proxy Statement |

| ¨ |

Definitive Additional Materials |

| ¨ |

Soliciting Material under §240.14a-12 |

STONEBRIDGE ACQUISITION CORPORATION

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement,

if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ¨ |

Fee paid previously with preliminary materials. |

| ¨ |

Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a6(i)(1) and 0-11 |

LETTER TO SHAREHOLDERS OF STONEBRIDGE ACQUISITION

CORPORATION

ONE WORLD TRADE CENTER, SUITE 8500

NEW YORK, NY 10007

TO BE HELD ON JANUARY 17, 2024

Dear StoneBridge Acquisition Corporation Shareholder:

You are cordially invited to virtually attend

an extraordinary general meeting of StoneBridge Acquisition Corporation, a Cayman Islands exempted company (the “Company,”

“StoneBridge,” “we,” “us” or “our”),

which will be held on January 17, 2024, at 11:00 a.m. Eastern Standard Time (the “Extraordinary General Meeting”)

at the offices of Winston & Strawn LLP located at 800 Capitol Street, Suite 2400, Houston, Texas, 77002 United States, and virtually

via live webcast at https://www.cstproxy.com/stonebridgespac/2024 and via teleconference using the following dial-in information:

Telephone access (listen-only):

Within the U.S. and Canada: 1 800-450-7155 (toll-free)

Outside of the U.S. and Canada: +1 857-999-9155 (standard rates apply)

Conference ID: 8943610#

The attached Notice of the

Extraordinary General Meeting and proxy statement describe the business StoneBridge will conduct at the Extraordinary General Meeting

and provide information about StoneBridge that you should consider when you vote your shares. As set forth in the attached proxy statement,

the Extraordinary General Meeting will be held for the purpose of considering and voting on the following proposals:

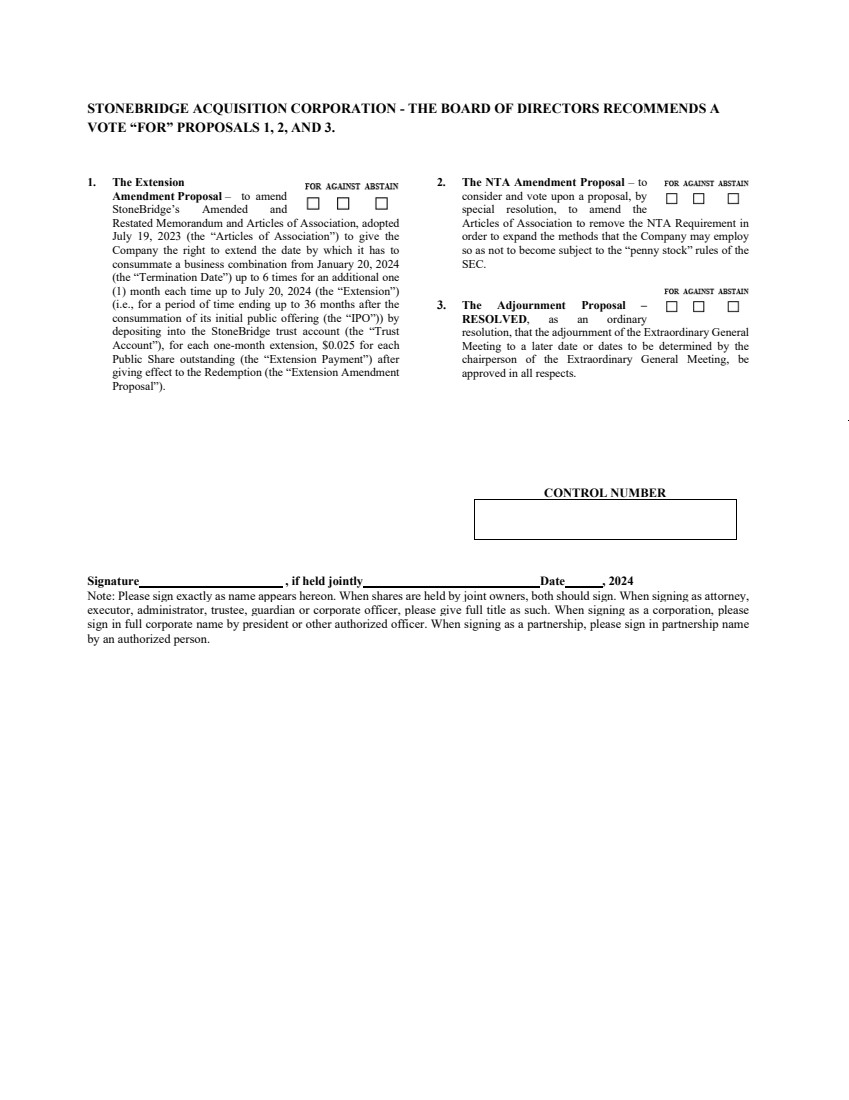

Proposal No. 1—Extension Amendment Proposal—A

proposal, by special resolution, to amend StoneBridge’s Amended and Restated Memorandum and Articles of Association, as amended

on July 19, 2023 (the “Articles of Association”) to give the Company the right to extend the date by which it

has to consummate a business combination (the “Combination Period”) from January 20, 2024 (the “Termination

Date”) up to 6 times for an additional one (1) month each time up to July 20, 2024 (the “Extension”)

(i.e., for a period of time ending up to 36 months after the consummation of its initial public offering (the “IPO”))

by depositing into the StoneBridge trust account (the “Trust Account”), for each one-month extension, $0.025

for each Public Share (as defined below) outstanding (the “Extension Payment”) after giving effect to the Redemption

(the “Extension Amendment Proposal”);

Proposal No. 2—NTA Amendment Proposal—A

proposal, by special resolution, to amend the Articles of Association to remove the net tangible asset (the “NTA”)

requirement in order to expand the methods that the Company may employ so as not to become subject to the “penny stock” rules

of the United States Securities and Exchange Commission (the “SEC”) (the “NTA Amendment Proposal”);

and

Proposal No. 3—Adjournment Proposal—A

proposal, by ordinary resolution to adjourn the Extraordinary General Meeting to a later date or dates, if necessary, to permit further

solicitation and vote of proxies if, based upon the tabulated vote at the time of the Extraordinary General Meeting, there are not sufficient

votes to approve the Extension Amendment Proposal, the NTA Amendment Proposal, or to provide additional time to effectuate the Extension

(the “Adjournment Proposal”).

Each of the Extension Amendment

Proposal, the NTA Amendment Proposal and the Adjournment Proposal is more fully described in the accompanying proxy statement. Please

take the time to read carefully each of the proposals in the accompanying proxy statement before you vote. Approval of the Extension Amendment

Proposal is a condition to the implementation of the Extension. Approval of the NTA Amendment Proposal is a condition to the removal of

the NTA Requirement. Notwithstanding the foregoing, even if the Extension Amendment Proposal and NTA Amendment Proposal are approved,

StoneBridge may nevertheless choose not to hold the Extraordinary General Meeting or not to amend the Articles of Association and may

liquidate on the Termination Date.

The purpose of the Extension

Amendment Proposal, NTA Amendment Proposal, and, if necessary, the Adjournment Proposal, is to allow StoneBridge additional time and flexibility

to complete an initial business combination (a “Business Combination”). Additionally, the purpose of the Extension

Amendment Proposal and NTA Amendment Proposal is to simultaneously (i) provide those StoneBridge shareholders who do not wish to extend

the Termination Date or remove the NTA Requirement with the opportunity to exercise their redemption rights earlier than they would if

StoneBridge liquidated on the Termination Date and (ii) allow those StoneBridge shareholders who wish for StoneBridge to continue its

search for a Business Combination to remain shareholders.

Currently, the company has

until the Termination Date, or January 20, 2024, to consummate the Business Combination and must maintain net tangible assets of at least

$5,000,001 upon consummation of the Business Combination. The Board has determined that it is in the best interests of StoneBridge to

(i) seek an extension of the Termination Date and have StoneBridge shareholders approve the Extension Amendment Proposal to allow for

additional time to consummate a Business Combination, and (ii) seek removal of the NTA Requirement and have StoneBridge shareholders approve

the NTA Amendment Proposal. The Board believes that the current Termination Date and NTA Requirement will not provide sufficient time

and flexibility to complete a Business Combination. Given StoneBridge’s commitment of time, effort and financial resources to date

with respect to identifying a Business Combination target, circumstances warrant providing shareholders with additional time and opportunity

to consider a prospective Business Combination. However, even if the Extension Amendment Proposal and NTA Amendment Proposal are approved

and the Extension is implemented and NTA Requirement removed, there is no assurance that StoneBridge will be able to consummate a Business

Combination within the Combination Period, as extended, given the actions that must occur prior to closing of a Business Combination

In order to avail ourselves

of the additional one-month extension periods to consummate the Business Combination, our sponsor, StoneBridge Acquisition Sponsor LLC

(the “Sponsor”) or its affiliates or designees (together with the Sponsor, the “Lender”),

upon five days’ advance notice prior to the applicable Business Combination deadline, must deposit into the Trust Account for each

such one-month extension, on or prior to the date of the applicable Business Combination deadline $0.025 for each outstanding Class A

ordinary share, par value $0.0001 per share and issued as part of the units issued in the IPO (each a “Public Share”

or “Class A ordinary share”), after giving effect to the Redemption. If we complete our Business Combination,

we would repay such loaned amounts out of the proceeds of the Trust Account released to us or, at the option of the Lender, convert such

loaned amounts into private placement warrants of the post business combination entity at a price of $1.00 per warrant. If we do not complete

a Business Combination, we will not repay such loans. In the event that we receive notice from our Sponsor five days prior to the applicable

Business Combination deadline of its wish for us to effect an extension, we intend to issue a press release announcing such intention

at least three days prior to the applicable Business Combination deadline. In addition, we intend to issue a press release the day after

the applicable Business Combination deadline announcing whether or not the funds had been timely deposited. Our Sponsor and its affiliates

or designees are not obligated to fund the Trust Account to extend the time for us to complete our initial business combination.

As contemplated by the Articles

of Association, in the event that any amendment is made to the Articles of Association to, among other things, modify the timing of the

Company’s obligation to allow redemption in connection with a Business Combination, the holders of Public Shares (the “Public

Shareholders”) may elect to redeem their Public Shares upon the approval of the effectiveness of such amendment in exchange

for a pro rata share of the aggregate amount then on deposit in the Trust Account, including interest earned on the Trust Account (net

of taxes paid or payable, if any), divided by the number of then outstanding Public Shares (the “Redemption”). You

may elect to redeem your Public Shares in connection with the Extraordinary General Meeting, regardless of whether you vote for or against

the proposals, by following the instructions set forth in the accompanying proxy statement.

A Public Shareholder, together

with any affiliate of such Public Shareholder or any other person with whom such Public Shareholder is acting in concert or as a “group”

(as defined in Section 13(d)(3) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)), will

be restricted from redeeming its Public Shares with respect to more than an aggregate of 15% of the Public Shares. Accordingly, if a Public

Shareholder, alone or acting in concert or as a group, seeks to redeem more than 15% of the Public Shares, then any such shares in excess

of that 15% limit would not be redeemed for cash.

On the Record Date (defined

below), the redemption price per Public Share was approximately $11.31 (which is expected to be the same approximate price per Public

Share on the date of the scheduled vote at the Extraordinary General Meeting), based on the aggregate amount on deposit in the Trust

Account of approximately $27,439,803 as of the Record Date (including interest not previously released to StoneBridge to pay its taxes),

divided by the total number of then outstanding Public Shares. The closing price of the Public Shares on the Nasdaq Capital Market (“Nasdaq”)

on the Record Date was $11.16. Accordingly, if the market price of the Public Shares were to remain the same until the date of the Extraordinary

General Meeting, exercising redemption rights would result in a holder of Public Shares receiving approximately $0.15 more per share

than if the Public Shares were sold in the open market. StoneBridge cannot assure shareholders that they will be able to sell their Public

Shares in the open market, even if the market price per Public Share is lower than the redemption price stated above, as there may not

be sufficient liquidity in its securities when such shareholders wish to sell their shares. StoneBridge believes that such redemption

right enables its holders of Public Shares to determine whether to sustain their investments for an additional period if StoneBridge

does not complete a Business Combination on or before the Termination Date.

If the Extension Amendment

Proposal is not approved and a Business Combination is not consummated by the Termination Date, or such later date that may be approved

by StoneBridge shareholders, or if the NTA Amendment Proposal is not approved and the NTA Requirement is not removed or satisfied at the

time of the consummation of the Business Combination, StoneBridge (i) will cease all operations except for the purpose of winding

up; (ii) as promptly as reasonably possible but not more than ten (10) business days thereafter subject to lawfully available

funds therefor, redeem 100% of the Public Shares in consideration of a per-share price, payable in cash, equal to the aggregate amount

then on deposit in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to

the Company (less taxes payable and up to $100,000 of interest to pay dissolution expenses), divided by the total number of then issued

and outstanding Public Shares, which redemption will completely extinguish rights of the holders of Public Shares (including the right

to receive further liquidating distributions, if any), subject to applicable law; and (iii) as promptly as reasonably possible following

such redemption, subject to the approval of StoneBridge’s remaining shareholders and the Board in accordance with applicable law,

liquidate and dissolve, subject in each case to StoneBridge’s obligations under Cayman Islands law, to provide for claims of creditors

and other requirements of applicable law.

Subject to the foregoing,

the approval of the Extension Amendment Proposal and the NTA Amendment Proposal requires a special resolution under Cayman Islands law,

being the affirmative vote of the holders of at least two-thirds (2/3) of the issued and outstanding Class A ordinary shares and Class

B ordinary shares (defined below) (together, the “Ordinary Shares”) entitled to vote and who, being present

in person or represented by proxy at the Extraordinary General Meeting or any adjournment thereof, vote on such matter. As of the date

of this proxy statement, the Company’s Class B ordinary shares, par value $0.0001 per share (the “Founder Shares”

or “Class B ordinary shares”), represent 67.3% of the Company’s outstanding Ordinary Shares. Accordingly,

if all outstanding Ordinary Shares are present at the Extraordinary General Meeting, then in addition to the Founder Shares, the Company

will not need any Public Shares to vote in favor of the Extension Amendment Proposal and the NTA Amendment Proposal to approve such proposal.

Further, if only a minimum quorum of outstanding Ordinary Shares is present at the Extraordinary General Meeting, then no Public Shares

will need to vote in favor of the Extension Amendment Proposal to approve such proposal.

Our Articles of Association

currently provides that the Company will not consummate any Business Combination unless it has net tangible assets of at least $5,000,001

upon consummation of such Business Combination (the “NTA Requirement”). The purpose of the NTA Amendment Proposal

is to add an additional basis on which the Company may rely, as it has since its IPO, so as not be to be subject to the “penny stock”

rules of the SEC.

If the NTA Amendment Proposal

is not approved, and there are significant requests for redemption such that the NTA Requirement is not satisfied, the NTA Requirement

would prevent the Company from being able to consummate a Business Combination, and because we have only a limited time to complete an

initial Business Combination, we may be required to liquidate. If we liquidate, our warrants will expire worthless and our investors would

lose the investment opportunity associated with an investment in the combined company, including through any potential price appreciation

of our securities.

Approval of the Adjournment

Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of the holders of a simple majority of the

issued and outstanding Ordinary Shares entitled to vote and who, being present in person or represented by proxy at the Extraordinary

General Meeting or any adjournment thereof, vote on such matter. Regardless of whether all or a minimum quorum of outstanding Ordinary

Shares are present at the Extraordinary General Meeting, then in addition to the Founder Shares, the Company will need none of the Public

Shares to vote in favor of the Adjournment Proposal to approve such proposal. The Adjournment Proposal will only be put forth for a vote

if there are not sufficient votes to approve the Extension Amendment Proposal and NTA Amendment Proposal at the Extraordinary General

Meeting.

The Board has fixed the close

of business on December 27, 2023 (the “Record Date”) as the date for determining StoneBridge shareholders entitled

to receive notice of and vote at the Extraordinary General Meeting and any adjournment thereof. Only holders of record of Ordinary Shares

on the Record Date are entitled to have their votes counted at the Extraordinary General Meeting or any adjournment thereof. On the Record

Date, there were 2,425,969 issued and outstanding Public Shares and 5,000,000 issued and outstanding Founder Shares. StoneBridge’s

warrants do not have voting rights.

As of the date of this proxy

statement, the Sponsor, individually, and collectively with the members of the board of directors of StoneBridge, owns approximately 67.3%

of the issued and outstanding StoneBridge Ordinary Shares (including 100% of the issued and outstanding StoneBridge Class B Ordinary Shares).

Accordingly, the Sponsor will be able to approve the Extension Amendment Proposal, the NTA Amendment Proposal and, if presented, the Adjournment

Proposal even if all other outstanding shares are voted against such proposals.

On December 19, 2023,

StoneBridge held an extraordinary general meeting of shareholders pursuant to which the StoneBridge shareholders of record approved the

Business Combination Agreement including the Business Combination and transactions contemplated thereby, among other related proposals.

Thus, you are not being asked to vote on a Business Combination at this time. If the Extension is implemented and you do not elect to

redeem all your Public Shares, you will retain the right to vote on any future Business Combination that is proposed to the StoneBridge

shareholders at a future date, in the event the currently approved Business Combination is not consummated, when and if it is submitted

to shareholders (provided that you are a shareholder on the applicable record date) and the right to redeem your remaining Public Shares

for cash in the event another Business Combination is approved and completed or in the event we have not consummated any Business Combination

within the Combination Period, as extended. There is no guarantee that we will be able to complete a Business Combination before the expiration

of the Combination Period, as extended.

After careful consideration

of all relevant factors, the Board has determined that the Extension Amendment Proposal, the NTA Amendment Proposal and the Adjournment

Proposal are in the best interests of StoneBridge and its shareholders, and has declared it advisable and recommends that you vote or

give instruction to vote “FOR” such proposals.

StoneBridge’s directors

and officers have interests in the Extension Amendment Proposal, the NTA Amendment Proposal and the Adjournment Proposal that may be different

from, or in addition to, your interests as a shareholder. These interests include, among others, ownership, directly or indirectly through

the Sponsor, of Founder Shares and Private Placement Warrants (as defined below) that may become exercisable in the future. See the section

entitled “Extraordinary General Meeting of StoneBridge—Interests of the Initial Shareholders” in the accompanying

proxy statement.

Enclosed is the proxy statement

containing detailed information about the Extraordinary General Meeting, the Extension Amendment Proposal, the NTA Amendment Proposal

and the Adjournment Proposal. Whether or not you plan to attend the Extraordinary General Meeting, StoneBridge urges you to read this

material carefully and vote your shares. You may do so by signing, dating and returning the enclosed proxy promptly, or following the

instructions contained in the proxy card or voting instructions. If you grant a proxy, you may revoke it at any time prior to the Extraordinary

General Meeting or vote in person online at the Extraordinary General Meeting. If your shares are held in an account at a brokerage firm

or bank, you must instruct your broker or bank how to vote your shares, or you may cast your vote online at the Extraordinary General

Meeting by obtaining a proxy from your brokerage firm or bank.

By Order of the Board of Directors

of StoneBridge Acquisition Corporation

Bhargav Marepally, Chief Executive Officer

January 8, 2024

Your vote is very important. Whether

or not you plan to attend the Extraordinary General Meeting, please vote as soon as possible by following the instructions in this proxy

statement to make sure that your shares are represented at the Extraordinary General Meeting. If you hold your shares in “street

name” through a bank, broker or other nominee, you will need to follow the instructions provided to you by your bank, broker or

other nominee to ensure that your shares are represented and voted at the Extraordinary General Meeting. The approval of the Extension

Amendment Proposal and the NTA Amendment Proposal requires a special resolution under Cayman Islands law, being the affirmative vote of

the holders of at least two-thirds (2/3) of issued and outstanding Ordinary Shares entitled to vote and who, being present in person or

represented by proxy at the Extraordinary General Meeting or any adjournment thereof, vote on such matter. Approval of the Adjournment

Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of the holders of at least a simple majority

of the issued and outstanding Ordinary Shares entitled to vote and who, being present in person or represented by proxy at the Extraordinary

General Meeting or any adjournment thereof, vote on such matter. The presence, in person (including virtually) or by proxy, at the Extraordinary

General Meeting of the holders of one-third of the outstanding Ordinary Shares entitled to vote as of the Record Date at the Extraordinary

General Meeting shall constitute a quorum for the conduct of business at the Extraordinary General Meeting. Accordingly, if you fail to

vote in person (including virtually) or by proxy at the Extraordinary General Meeting, or if your broker, bank or nominee submits a broker

non-vote with respect to your Ordinary Shares, your shares will not be counted towards the number of Ordinary Shares required to validly

establish a quorum. If a valid quorum is otherwise established, such failure to vote or broker non-vote will have no effect on the outcome

of any vote on the Extension Amendment Proposal, the NTA Amendment Proposal or Adjournment Proposal. Abstentions and broker non-votes,

while considered present for the purposes of establishing a quorum, will not count as a vote cast at the Extraordinary General Meeting

and will have no effect on the outcome of any vote on the Extension Amendment Proposal, the NTA Amendment Proposal or Adjournment Proposal.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST

(1) IF YOU HOLD PUBLIC SHARES THROUGH UNITS, ELECT TO SEPARATE YOUR UNITS INTO THE UNDERLYING PUBLIC SHARES AND PUBLIC WARRANTS PRIOR

TO EXERCISING YOUR REDEMPTION RIGHTS WITH RESPECT TO THE PUBLIC SHARES, (2) SUBMIT A WRITTEN REQUEST TO THE TRANSFER AGENT BY 5:00 P.M.

EASTERN TIME ON JANUARY 15, 2024, THE DATE THAT IS TWO BUSINESS DAYS PRIOR TO THE SCHEDULED VOTE AT THE EXTRAORDINARY GENERAL MEETING,

THAT YOUR PUBLIC SHARES BE REDEEMED FOR CASH, INCLUDING THE LEGAL NAME, PHONE NUMBER, AND ADDRESS OF THE BENEFICIAL OWNER OF THE SHARES

FOR WHICH REDEMPTION IS REQUESTED, AND (3) DELIVER YOUR PUBLIC SHARES TO THE TRANSFER AGENT, PHYSICALLY OR ELECTRONICALLY USING THE DEPOSITORY

TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM, IN EACH CASE IN ACCORDANCE WITH THE PROCEDURES AND DEADLINES DESCRIBED

IN THE ACCOMPANYING PROXY STATEMENT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK

OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

Important Notice Regarding the Availability

of Proxy Materials for the Extraordinary General Meeting of Shareholders to be held on January 17, 2024: This notice of meeting and the

accompanying proxy statement are being made available on or about January 8, 2024, at https://www.cstproxy.com/stonebridgespac/2024.

NOTICE OF EXTRAORDINARY GENERAL MEETING

OF STONEBRIDGE ACQUISITION CORPORATION

TO BE HELD ON JANUARY 17, 2024

To the Shareholders of StoneBridge Acquisition

Corporation:

NOTICE IS HEREBY GIVEN that

an Extraordinary General Meeting (the “Extraordinary General Meeting”) of the shareholders of StoneBridge Acquisition

Corporation, a Cayman Islands exempted company (the “Company,” “StoneBridge,” “we,”

“us” or “our”), will be held on January 17, 2024, at 11:00 a.m. Eastern Time at the

offices of Winston & Strawn LLP located at 800 Capitol Street, Suite 2400, Houston, Texas, 77002 United States, and virtually, via

live webcast at https://www.cstproxy.com/stonebridgespac/2024 and via teleconference using the following dial-in information:

Telephone access (listen-only):

Within the U.S. and Canada: 1 800-450-7155 (toll-free)

Outside of the U.S. and Canada: +1 857-999-9155 (standard rates apply)

Conference ID: 8943610#

You are cordially invited

to attend the Extraordinary General Meeting for the purpose of considering and voting on the following proposals, more fully described

below in this proxy statement, which is dated January 8, 2024 and is first being mailed to shareholders on or about January 8, 2024:

Proposal No. 1—Extension Amendment Proposal—A

proposal, by special resolution, to amend StoneBridge’s Articles of Association to give the Company the right to extend the Combination

Period from January 20, 2024 up to 6 times for an additional one (1) month each time up to July 20, 2024 (i.e., for a period of time ending

up to 36 months after the consummation of its IPO) by depositing into the Trust Account, for each one-month extension, the Extension Payment

after giving effect to the Redemption;

Proposal No. 2—NTA Amendment Proposal—A

proposal, by special resolution, to amend the Articles of Association to remove the NTA Requirement in order to expand the methods that

the Company may employ so as not to become subject to the “penny stock” rules of the SEC; and

Proposal No. 3—Adjournment Proposal—A

proposal, by ordinary resolution to adjourn the Extraordinary General Meeting to a later date or dates, if necessary, to permit further

solicitation and vote of proxies if, based upon the tabulated vote at the time of the Extraordinary General Meeting, there are not sufficient

votes to approve the Extension Amendment Proposal , the NTA Amendment Proposal, or to provide additional time to effectuate the Extension.

Each of the Extension Amendment

Proposal, the NTA Amendment Proposal and the Adjournment Proposal is more fully described in the accompanying proxy statement. Please

take the time to read carefully each of the proposals in the accompanying proxy statement before you vote. Approval of the Extension Amendment

Proposal is a condition to the implementation of the Extension. Approval of the NTA Amendment Proposal is a condition to the removal of

the NTA Requirement. Even if the Extension Amendment Proposal and NTA Amendment Proposal are approved, we may nevertheless choose not

to hold the Extraordinary General Meeting or not to amend the Articles of Association and may liquidate on the Termination Date.

The purpose of the Extension

Amendment Proposal, the NTA Amendment Proposal, and, if necessary, the Adjournment Proposal, is to allow StoneBridge additional time and

flexibility to complete an initial business combination (“Business Combination”). Additionally, the purpose of the

Extension Amendment Proposal and the NTA Amendment Proposal is to simultaneously (i) provide those StoneBridge shareholders who do not

wish to extend the Termination Date or remove the NTA Requirement with the opportunity to exercise their redemption rights earlier than

they would if StoneBridge liquidated on the Termination Date and (ii) allow those StoneBridge shareholders who wish for StoneBridge to

continue its search for a Business Combination to remain shareholders.

Currently, the company has

(i) until the Termination Date, or January 20, 2024, to consummate the Business Combination and (ii) maintain net tangible assets of

at least $5,000,001 upon consummation of the Business Combination. The Board has determined that it is in the best interests of StoneBridge

to (i) seek an extension of the Termination Date and have StoneBridge shareholders approve the Extension Amendment Proposal to allow

for additional time to consummate a Business Combination, and (ii) seek removal of the NTA Requirement and have StoneBridge shareholders

approve the NTA Amendment Proposal. The Board believes that the current Termination Date and NTA Requirement will not provide sufficient

time and flexibility to complete a Business Combination. Given StoneBridge’s commitment of time, effort and financial resources

to date with respect to identifying a Business Combination target, circumstances warrant providing shareholders with additional time

and opportunity to consider a prospective Business Combination. However, even if the Extension Amendment Proposal and NTA Amendment Proposal

are approved and the Extension is implemented and NTA Requirement removed, there is no assurance that StoneBridge will be able to consummate

a Business Combination within the Combination Period, as extended, given the actions that must occur prior to closing of a Business Combination.

In order to avail ourselves

of the additional one-month extension periods to consummate the Business Combination, the Sponsor or its affiliates or designees (together

with the Sponsor, the “Lender”), upon five days’ advance notice prior to the applicable Business Combination

deadline, must deposit into the Trust Account for each such one-month extension, on or prior to the date of the applicable Business Combination

deadline $0.025 for each Public Share outstanding after giving effect to the Redemption. If we complete our Business Combination, we would

repay such loaned amounts out of the proceeds of the Trust Account released to us or, at the option of the Lender, convert such loaned

amounts into private placement warrants of the post business combination entity at a price of $1.00 per warrant. If we do not complete

a Business Combination, we will not repay such loans. In the event that we receive notice from our Sponsor five days prior to the applicable

Business Combination deadline of its wish for us to effect an extension, we intend to issue a press release announcing such intention

at least three days prior to the applicable Business Combination deadline. In addition, we intend to issue a press release the day after

the applicable Business Combination deadline announcing whether or not the funds had been timely deposited. Our Sponsor and its affiliates

or designees are not obligated to fund the Trust Account to extend the time for us to complete our initial business combination.

As contemplated by the Articles

of Association, in the event that any amendment is made to the Articles of Association to, among other things, modify the timing of the

Company’s obligation to allow redemption in connection with a Business Combination, the holders Public Shares (the “Public

Shareholders”) may elect to redeem their Public Shares upon the approval of the effectiveness of such amendment in exchange

for a pro rata share of the aggregate amount then on deposit in the Trust Account, including interest earned on the Trust Account (net

of taxes paid or payable, if any), divided by the number of then outstanding Public Shares. You may elect to redeem your Public Shares

in connection with the Extraordinary General Meeting, regardless of whether you vote for or against the proposals, by following the instructions

in the accompanying proxy statement.

A Public Shareholder, together

with any affiliate of such Public Shareholder or any other person with whom such Public Shareholder is acting in concert or as a “group”

(as defined in Section 13(d)(3) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)), will

be restricted from redeeming its Public Shares with respect to more than an aggregate of 15% of the Public Shares. Accordingly, if a Public

Shareholder, alone or acting in concert or as a group, seeks to redeem more than 15% of the Public Shares, then any such shares in excess

of that 15% limit would not be redeemed for cash.

On the Record Date (defined

below), the redemption price per Public Share was approximately $11.31 (which is expected to be the same approximate price per Public

Share on the date of the scheduled vote at the Extraordinary General Meeting), based on the aggregate amount on deposit in the Trust Account

of approximately $27,439,803 as of the Record Date (including interest not previously released to StoneBridge to pay its taxes), divided

by the total number of then outstanding Public Shares. The closing price of the Public Shares on Nasdaq on the Record Date was $11.16.

Accordingly, if the market price of the Public Shares were to remain the same until the date of the Extraordinary General Meeting, exercising

redemption rights would result in a holder of Public Shares receiving approximately $0.15 more per share than if the Public Shares were

sold in the open market. StoneBridge cannot assure shareholders that they will be able to sell their Public Shares in the open market,

even if the market price per Public Share is lower than the redemption price stated above, as there may not be sufficient liquidity in

its securities when such shareholders wish to sell their shares. StoneBridge believes that such redemption right enables its holders of

Public Shares to determine whether to sustain their investments for an additional period if StoneBridge does not complete a Business Combination

on or before the Termination Date.

If the Extension Amendment

Proposal is not approved and a Business Combination is not consummated by the Termination Date, or such later date that may be approved

by StoneBridge shareholders, or if the NTA Amendment Proposal is not approved and the NTA Requirement is not removed or satisfied at the

time of the consummation of the Business Combination StoneBridge will (i) cease all operations except for the purpose of winding up; (ii) as

promptly as reasonably possible but not more than ten (10) business days thereafter subject to lawfully available funds therefor,

redeem 100% of the Public Shares in consideration of a per-share price, payable in cash, equal to the aggregate amount then on deposit

in the Trust Account, including interest earned on the funds held in the Trust Account and not previously released to the Company (less

taxes payable and up to $100,000 of interest to pay dissolution expenses), divided by the total number of then issued and outstanding

Public Shares, which redemption will completely extinguish rights of the holders of Public Shares (including the right to receive further

liquidating distributions, if any), subject to applicable law; and (iii) as promptly as reasonably possible following such redemption,

subject to the approval of StoneBridge’s remaining shareholders and the Board in accordance with applicable law, liquidate and dissolve,

subject in each case to StoneBridge’s obligations under Cayman Islands law, to provide for claims of creditors and other requirements

of applicable law.

Pursuant to our Articles

of Association, a Public Shareholder may request to redeem all or a portion of such holder’s Public Shares for cash if the Extension

is consummated. As a holder of Public Shares, you will be entitled to receive cash for any Public Shares to be redeemed only if you:

| (i) |

(a) hold Public Shares or (b) hold Public Shares through Units (as defined below) and elect to separate your Units into the underlying Public Shares and Public Warrants (as defined below) prior to exercising your redemption rights with respect to the Public Shares; |

| (ii) |

submit a written request to Continental Stock Transfer & Trust Company (the “Trustee” or “Transfer Agent”) including the legal name, phone number and address of the beneficial owner of the Public Shares for which redemption is requested, that StoneBridge redeem all or a portion of your Public Shares for cash; and |

| (iii) |

deliver your share certificates for Public Shares (if any) along with other applicable redemption forms to the Trustee, physically or electronically through The Depository Trust Company (“DTC”). |

Holders must complete the

procedures for electing to redeem their Public Shares in the manner described above prior to 5:00 p.m., Eastern Time, on January 15, 2024

(two business days prior to the scheduled vote at the Extraordinary General Meeting) in order for their Public Shares to be redeemed.

Public Shareholders may elect to redeem Public Shares regardless of if or how they vote in respect of the Extension Amendment Proposal

or NTA Amendment Proposal. If the Extension is not consummated, the Public Shares will be returned to the respective holder, broker or

bank.

Subject to the foregoing,

the approval of the Extension Amendment Proposal and NTA Amendment Proposal requires a special resolution under Cayman Islands law, being

the affirmative vote of the holders of at least two-thirds (2/3) of the holders of the issued and outstanding Ordinary Shares entitled

to vote and who, being present in person or represented by proxy at the Extraordinary General Meeting or any adjournment thereof, vote

on such matter. As of the date of this proxy statement, the Company’s Class B ordinary shares, par value $0.0001 per share (the

“Founder Shares”), represent 67.3% of the Company’s outstanding Ordinary Shares. Accordingly, if all outstanding

Ordinary Shares are present at the Extraordinary General Meeting, then in addition to the Founder Shares, the Company will not need any

Public Shares to vote in favor of the Extension Amendment Proposal and NTA Amendment Proposal to approve such proposals. If only a minimum

quorum of outstanding Ordinary Shares is present at the Extraordinary General Meeting, then no Public Shares will need to vote in favor

of the Extension Amendment Proposal and NTA Amendment Proposal to approve such proposals.

Our Articles of Association

currently provides that the Company will not consummate any Business Combination unless it has net tangible assets of at least $5,000,001

upon consummation of such Business Combination (the “NTA Requirement”). The purpose of the NTA Amendment Proposal

is to add an additional basis on which the Company may rely, as it has since its IPO, so as not be to be subject to the “penny stock”

rules of the SEC.

If the NTA Amendment Proposal

is not approved, and there are significant requests for redemption such that the NTA Requirement is not satisfied, the NTA Requirement

would prevent the Company from being able to consummate a Business Combination, and because we have only a limited time to complete an

initial Business Combination, we may be required to liquidate. If we liquidate, our warrants will expire worthless and our investors would

lose the investment opportunity associated with an investment in the combined company, including through any potential price appreciation

of our securities.

Approval of the Adjournment

Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of the holders of a simple majority of the

issued and outstanding Ordinary Shares entitled to vote and who, being present in person or represented by proxy at the Extraordinary

General Meeting or any adjournment thereof, vote on such matter. Regardless of whether all or a minimum quorum of outstanding Ordinary

Shares are present at the Extraordinary General Meeting, then in addition to the Founder Shares, the Company will need none of the outstanding

Public Shares, to vote in favor of the Adjournment Proposal to approve such proposal. The Adjournment Proposal will only be put forth

for a vote if there are not sufficient votes to approve the Extension Amendment Proposal or NTA Amendment Proposal at the Extraordinary

General Meeting.

Record holders of Ordinary

Shares at the close of business on December 27, 2023 (the “Record Date”) are entitled to vote or have their

votes cast at the Extraordinary General Meeting. On the Record Date, there were 2,425,969 issued and outstanding Public Shares and 5,000,000

issued and outstanding Founder Shares. StoneBridge’s warrants do not have voting rights.

This proxy statement contains

important information about the Extraordinary General Meeting, the Extension Amendment Proposal, the NTA Amendment Proposal and the Adjournment

Proposal. Whether or not you plan to attend the Extraordinary General Meeting, StoneBridge urges you to read this material carefully and

vote your shares.

As of the date of this proxy

statement, the Sponsor, individually, and collectively with the members of the board of directors of StoneBridge, owns approximately 67.3%

of the issued and outstanding StoneBridge Ordinary Shares (including 100% of the issued and outstanding StoneBridge Class B Ordinary Shares).

Accordingly, the Sponsor will be able to approve the Extension Amendment Proposal, the NTA Amendment Proposal and, if presented, the Adjournment

Proposal even if all other outstanding shares are voted against such proposals.

This proxy statement is dated January 8, 2024

and is first being mailed to shareholders on or about January 8, 2024.

By Order of the Board of Directors of StoneBridge

Acquisition Corporation

Bhargav Marepally. Chief Executive Officer

TABLE OF CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements contained

in this proxy statement constitute forward-looking statements within the meaning of the federal securities laws. Forward-looking statements

relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning

matters that are not historical facts. Forward-looking statements reflect StoneBridge’s current views with respect to, among other

things, its capital resources and results of operations. Likewise, StoneBridge’s financial statements and all of StoneBridge’s

statements regarding market conditions and results of operations are forward-looking statements. In some cases, you can identify these

forward-looking statements by the use of terminology such as “outlook,” “believes,” “expects,” “potential,”

“continues,” “may,” “will,” “should,” “could,” “seeks,” “approximately,”

“predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative

version of these words or other comparable words or phrases.

The forward-looking statements

contained in this proxy statement reflect StoneBridge’s current views about future events and are subject to numerous known and

unknown risks, uncertainties, assumptions and changes in circumstances that may cause its actual results to differ significantly from

those expressed in any forward- looking statement. StoneBridge does not guarantee that the transactions and events described will happen

as described (or that they will happen at all). The following factors, among others, could cause actual results and future events to differ

materially from those set forth or contemplated in the forward-looking statements:

| |

• |

StoneBridge’s ability to complete a Business Combination, including approval by the shareholders of StoneBridge; |

| |

• |

the anticipated benefits of a Business Combination; |

| |

• |

the volatility of the market price and liquidity of the Public Shares and other securities of StoneBridge; |

| |

• |

the use of funds not held in the Trust Account or available to StoneBridge from interest income on the Trust; Account balance; |

| |

• |

the competitive environment in which our successor will operate following a Business Combination; and |

| |

• |

proposed changes in SEC rules related to special purpose acquisition companies. |

While forward-looking statements

reflect StoneBridge’s good faith beliefs, they are not guarantees of future performance. StoneBridge disclaims any obligation to

publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, new information, data

or methods, future events or other changes after the date of this proxy statement, except as required by applicable law. For a further

discussion of these and other factors that could cause StoneBridge’s future results, performance or transactions to differ significantly

from those expressed in any forward-looking statement, please see the section entitled “Risk Factors” in StoneBridge’s

Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the SEC on March 28, 2023, and in other reports StoneBridge

filed with the SEC, including StoneBridge’s Quarterly Reports on Form 10-Q for the period ended September 30, 2023, filed with the

SEC on November 6, 2023. You should not place undue reliance on any forward-looking statements, which are based only on information currently

available to StoneBridge.

QUESTIONS AND ANSWERS ABOUT THE EXTRAORDINARY

GENERAL MEETING

| Q. | Why am I receiving this proxy

statement? |

| A. | StoneBridge is a blank check company

incorporated under the laws of the Cayman Islands on February 2, 2021, for the purpose of effecting a merger, share exchange, asset acquisition,

share purchase, reorganization or similar business combination, with one or more businesses, without limitation as to business, industry

or sector. StoneBridge’s registration statement on Form S-1 (File No. 333-253641) for StoneBridge’s IPO was declared

effective by the SEC on July 15, 2021. On July 20, 2021, StoneBridge consummated its IPO of 20,000,000 units (the “Units”).

Each Unit consists of one Class A ordinary share and one-half of one redeemable warrant, with each whole warrant entitling the holder

to purchase one Class A ordinary share at $11.50 per share beginning 30 days after the completion of a Business Combination (the “Public

Warrants”). The Units were sold at an offering price of $10.00 per Unit, generating gross proceeds of $200,000,000. Simultaneously

with the consummation of the IPO and the sale of the Units, StoneBridge consummated the private placement of an aggregate of 8,000,000

warrants (the “Private Placement Warrants”) issued to the Sponsor at a price of $1.00 per warrant, generating total

proceeds of $8,000,000. Each Private Placement Warrant is exercisable for one Class A ordinary share beginning 30 days after the completion

of a Business Combination. |

A

total of $202,000,000 of the net proceeds from StoneBridge’s IPO and sale of the Private Placement Warrants were deposited in the

Trust Account established for the benefit of the holders of Public Shares.

Like

most blank check companies, the Articles of Association provides for the return of the IPO proceeds held in trust to the holders of Public

Shares sold in the IPO if there is no qualifying Business Combination(s) consummated on or before the Termination Date.

On

October 13, 2022, StoneBridge notified the trustee of the Company’s Trust Account that it was extending the time available to the

Company to consummate a Business Combination from October 20, 2022 to January 20, 2023. The extension was the first of up to two (2)

three-month extensions permitted under the Company’s then-existing governing documents. In connection with such extension, the

Sponsor deposited an aggregate of $1,000,000 into the Trust Account, on behalf of the Company on October 13, 2022.

On

January 20, 2023, StoneBridge held an extraordinary general meeting of shareholders, pursuant to which, the Company’s shareholders

approved, by special resolution, a proposal to amend the Company’s Articles of Association to give the Company the right to extend

the date by which it has to consummate a Business from January 20, 2023 up to 6 times for an additional one (1) month each time up to

July 20, 2023 by depositing into the Trust Account, for each one-month extension, $0.05 for each Class A ordinary share outstanding,

after giving effect to any shareholder redemptions, which amount shall not exceed $150,000 per extension. In connection with such extension,

the Sponsor deposited an aggregate of $150,000 into the Trust Account, on behalf of the Company on January 20, 2023, extending the time

available to the Company to consummate its initial business combination from January 20, 2023 to February 20, 2023. On February 16, 2023,

March 13, 2023, April 14, 2023. May 17, 2023, and June 14, 2023, the Sponsor deposited $150,000 into the Trust Account on each date,

on behalf of the Company, to extend the time available to the Company to consummate its initial business combination to the 20th of each

such month.

On

July 19, 2023, StoneBridge held an extraordinary general meeting of shareholders, pursuant to which, the Company’s shareholders

approved, by special resolution, a proposal to amend StoneBridge’s Articles of Association to give the Company the right to extend

the Combination Period from July 20, 2023 up to 6 times for an additional one (1) month each time up to January 20, 2024 (i.e., for a

period of time ending up to 30 months after the consummation of its IPO) by depositing into the Trust Account, for each one-month extension,

$0.025 for each Public Share after giving effect to any shareholder redemptions. In connection with such extension, the Sponsor deposited

$60,649.23 into the Trust Account, on behalf of the Company on July 19, 2023, extending the time available to the Company to consummate

its initial business combination from July 20, 2023 to August 20, 2023. On August 15, 2023, September 13, 2023, October 12, 2023. November

17, 2023, and December 13, 2023, the Sponsor deposited $60,649.23 into the Trust Account on each date, on behalf of the Company, to extend

the time available to the Company to consummate its initial business combination to the 20th of each such month.

On

December 19, 2023, StoneBridge held an extraordinary general meeting of shareholders, pursuant to which, the Company’s shareholders

approved, by ordinary resolution, the Business Combination and other transactions contemplated by, and StoneBridge’s entry into,

the business combination agreement, dated as of January 5, 2023 (as amended on June 22, 2023 by the First Amendment to Business Combination

Agreement, December 28, 2023 by the Second Amendment to Business Combination Agreement, and as may be further amended, supplemented,

or otherwise modified from time to time, the “Business Combination Agreement”), by and among StoneBridge, StoneBridge

Acquisition Pte. Ltd., a Singapore private company limited by shares and a direct wholly owned subsidiary of Stonebridge (“Amalgamation

Sub”), DigiAsia Bios Pte. Ltd., a Singapore private company limited by shares, and Prashant Gokarn, solely in his

capacity as the management representative. In connection with the approval of the Business Combination, StoneBridge shareholders approved

other proposals related to the Business Combination.

Currently,

the Company has until the Termination Date, or January 20, 2024, to consummate the Business Combination and must maintain net tangible

assets of at least $5,000,001 upon consummation of the Business Combination. The Board has determined that it is in the best interests

of StoneBridge to (i) seek an extension of the Termination Date and have StoneBridge shareholders approve the Extension Amendment Proposal

to allow for additional time to consummate a Business Combination, and (ii) seek removal of the NTA Requirement and have StoneBridge

shareholders approve the NTA Amendment Proposal. The Board believes that the current Termination Date and NTA Requirement will not provide

sufficient time and flexibility to complete a Business Combination. Given StoneBridge’s commitment of time, effort and financial

resources to date with respect to identifying a Business Combination target, circumstances warrant providing shareholders with additional

time and opportunity to consider a prospective Business Combination. However, even if the Extension Amendment Proposal and NTA Amendment

Proposal are approved and the Extension is implemented and NTA Requirement removed, there is no assurance that StoneBridge will be able

to consummate a Business Combination within the Combination Period, as extended, given the actions that must occur prior to closing of

a Business Combination.

| Q. | When and where is the Extraordinary

General Meeting? |

| A. | The Extraordinary General Meeting

will be held on January 17, 2024, at 11:00 a.m. Eastern Time at the offices of Winston & Strawn LLP located at 800 Capitol Street,

Suite 2400, Houston, Texas, 77002 United States, and virtually via live webcast by visiting https://www.cstproxy.com/stonebridgespac/2024

and entering the voter control number included on your proxy card and via teleconference using the following dial-in information: |

Telephone access (listen-only):

Within the U.S. and Canada: 1 800-450-7155 (toll-free)

Outside of the U.S. and Canada: +1 857-999-9155 (standard rates apply)

Conference ID: 8943610#

| Q. | What do I need in order to

be able to participate in the Extraordinary General Meeting online? |

| A. | Any shareholder wishing to attend

the Extraordinary General Meeting virtually should register for the Extraordinary General Meeting by January 16, 2024 by 4:30 p.m. Eastern

Time at https://www.cstproxy.com/stonebridgespac/2024. You can virtually attend the Extraordinary General Meeting via the internet by

visiting https://www.cstproxy.com/stonebridgespac/2024 and entering the voter control number included on your proxy card. You will need

the voter control number included on your proxy card in order to be able to vote your shares or submit questions during the Extraordinary

General Meeting. If you do not have a voter control number, you will be able to listen to the Extraordinary General Meeting only and

you will not be able to vote or submit questions during the Extraordinary General Meeting. |

| Q. | What are the specific proposals

on which I am being asked to vote at the Extraordinary General Meeting? |

| A. | StoneBridge shareholders are being

asked to consider and vote on the following proposals: |

Proposal No. 1—Extension Amendment Proposal—A

proposal, by special resolution, to amend StoneBridge’s Articles of Association to give the Company the right to extend the Combination

Period from January 20, 2024 up to 6 times for an additional one (1) month each time up to July 20, 2024 (i.e., for a period of time ending

up to 36 months after the consummation of its IPO) by depositing into the Trust Account, for each one-month extension, the Extension Payment

after giving effect to the Redemption;

Proposal No. 2—NTA Amendment Proposal—A

proposal, by special resolution, to amend the Articles of Association to remove the NTA Requirement in order to expand the methods that

the Company may employ so as not to become subject to the “penny stock” rules of the SEC; and

Proposal No. 3—Adjournment Proposal—A

proposal, by ordinary resolution to adjourn the Extraordinary General Meeting to a later date or dates, if necessary, to permit further

solicitation and vote of proxies if, based upon the tabulated vote at the time of the Extraordinary General Meeting, there are not sufficient

votes to approve the Extension Amendment Proposal, NTA Amendment Proposal, or to provide additional time to effectuate the Extension.

| Q. | Are the proposals conditioned

on one another? |

| A. | Approval of the Extension Amendment

Proposal is a condition to the implementation of the Extension. If the Extension is implemented and one or more StoneBridge shareholders

elect to redeem their Public Shares, StoneBridge will remove from the Trust Account and deliver to the holders of such redeemed Public

Shares an amount equal to the pro rata portion of funds available in the Trust Account with respect to such redeemed Public Shares, as

described in more detail in this proxy statement, and will retain the remainder of the funds in the Trust Account for StoneBridge’s

use in connection with consummating a Business Combination on or before the expiration of the Combination Period, as extended. |

If the Extension Amendment Proposal is not approved

and a Business Combination is not consummated by the Termination Date, or such later date that may be approved by StoneBridge shareholders,

or if the NTA Amendment Proposal is not approved and the NTA Requirement is not removed or satisfied at the time of the consummation of

the Business Combination, StoneBridge (i) will cease all operations except for the purpose of winding up; (ii) as promptly as reasonably

possible but not more than ten (10) business days thereafter subject to lawfully available funds therefor, redeem 100% of the Public Shares

in consideration of a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including

interest earned on the funds held in the Trust Account and not previously released to the Company (less taxes payable and up to $100,000

of interest to pay dissolution expenses), divided by the total number of then issued and outstanding Public Shares, which redemption will

completely extinguish rights of the holders of Public Shares (including the right to receive further liquidating distributions, if any),

subject to applicable law; and (iii) as promptly as reasonably possible following such redemption, subject to the approval of StoneBridge’s

remaining shareholders and the Board in accordance with applicable law, liquidate and dissolve, subject in each case to StoneBridge’s

obligations under Cayman Islands law to provide for claims of creditors and other requirements of applicable law.

The Sponsor and all of StoneBridge’s directors

and officers (the “initial shareholders”) waived their rights to participate in any liquidating distribution

with respect to the 5,000,000 Founder Shares held by them. There will be no distribution from the Trust Account with respect to StoneBridge’s

warrants, which will expire worthless in the event StoneBridge dissolves and liquidates the Trust Account.

Even if the Extension Amendment Proposal and NTA Amendment Proposal

are approved, StoneBridge may nevertheless choose not to hold the Extraordinary General Meeting or not to amend the Articles of Association

and may liquidate on the Termination Date.

The NTA Amendment Proposal and the Adjournment

Proposal are not conditioned on the approval of any other proposal.

| Q. | Why is StoneBridge proposing

the Extension Amendment Proposal, the NTA Amendment Proposal and the Adjournment Proposal? |

| A. | The Articles of Association provides

for the return of the IPO proceeds held in the Trust Account to the holders of Public Shares sold in the IPO if there is no qualifying

business combination(s) consummated on or before the Termination Date. The purpose of the Extension Amendment Proposal, and, if necessary,

the Adjournment Proposal, is to allow StoneBridge additional time to complete a Business Combination. Additionally, the purpose of the

Extension Amendment Proposal is to simultaneously (i) provide those StoneBridge shareholders who do not wish to extend the Termination

Date with the opportunity to exercise their redemption rights earlier than they would if StoneBridge liquidated on the Termination Date

and (ii) allow those StoneBridge shareholders who wish for StoneBridge to continue its search for a Business Combination to remain shareholders. |

Currently, the Company has until the Termination

Date, or January 20, 2024, to consummate the Business Combination and must maintain net tangible assets of at least $5,000,001 upon consummation

of the Business Combination. The Board has determined that it is in the best interests of StoneBridge to (i) seek an extension of the

Termination Date and have StoneBridge shareholders approve the Extension Amendment Proposal to allow for additional time to consummate

a Business Combination, and (ii) seek removal of the NTA Requirement and have StoneBridge shareholders approve the NTA Amendment Proposal.

The Board believes that the current Termination Date and NTA Requirement will not provide sufficient time and flexibility to complete

a Business Combination. Given StoneBridge’s commitment of time, effort and financial resources to date with respect to identifying

a Business Combination target, circumstances warrant providing shareholders with additional time and opportunity to consider a prospective

Business Combination. However, even if the Extension Amendment Proposal and NTA Amendment Proposal are approved and the Extension is implemented

and NTA Requirement removed, there is no assurance that StoneBridge will be able to consummate a Business Combination within the Combination

Period, as extended, given the actions that must occur prior to closing of a Business Combination

If the Extension Amendment Proposal or the NTA

Amendment Proposal are not approved by StoneBridge shareholders, StoneBridge may put the Adjournment Proposal to a vote in order to seek

additional time to obtain sufficient votes in support of the Extension, or to otherwise provide additional time to effectuate the Extension.

If the Adjournment Proposal is not approved by StoneBridge shareholders, the Board may not be able to adjourn the Extraordinary General

Meeting to a later date or dates in the event that there are insufficient votes for, or otherwise in connection with, the approval of

the Extension Amendment Proposal.

On December 19, 2023, StoneBridge held an extraordinary

general meeting of shareholders pursuant to which the StoneBridge shareholders of record approved the Business Combination Agreement including

the Business Combination and transactions contemplated thereby, among other related proposals. Thus, you are not being asked to vote on

a Business Combination at this time. If the Extension is implemented and you do not elect to redeem all your Public Shares, you will retain

the right to vote on any future Business Combination that is proposed to the StoneBridge shareholders at a future date, in the event the

currently approved Business Combination is not consummated, when and if it is submitted to shareholders (provided that you are a shareholder

on the applicable record date) and the right to redeem your remaining Public Shares for cash in the event another Business Combination

is approved and completed or in the event we have not consummated any Business Combination within the Combination Period, as extended.

There is no guarantee that we will be able to complete a Business Combination before the expiration of the Combination Period, as extended.

| Q. | What vote is required to approve

the proposals presented at the Extraordinary General Meeting? |

| A. | The approval of the Extension

Amendment Proposal and the NTA Amendment Proposal requires a special resolution under Cayman Islands law, being the affirmative vote

of holders of at least two-thirds (2/3) of the issued and outstanding Ordinary Shares entitled to vote and who, being present in person

or represented by proxy at the Extraordinary General Meeting or any adjournment thereof, vote on such matter. Approval of the Adjournment

Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of the holders of a simple majority of

the issued and outstanding Ordinary Shares entitled to vote and who, being present in person or represented by proxy at the Extraordinary

General Meeting or any adjournment thereof, vote on such matter. |

The presence, in person (including virtually)

or by proxy, at the Extraordinary General Meeting of the holders of one-third of the outstanding Ordinary Shares entitled to vote as of

the Record Date at the Extraordinary General Meeting shall constitute a quorum for the conduct of business at the Extraordinary General

Meeting. Accordingly, a StoneBridge’s shareholder’s failure to vote in person (including virtually) or by proxy at the Extraordinary

General Meeting, will not be counted towards the number of Ordinary Shares required to validly establish a quorum. If a valid quorum is

otherwise established, such failure to vote or broker non-vote will have no effect on the outcome of any vote on the Extension Amendment

Proposal, the NTA Amendment Proposal or Adjournment Proposal. Abstentions and broker non-votes, while considered present for the purposes

of establishing a quorum, will not count as a vote cast at the Extraordinary General Meeting and will have no effect on the outcome of

any vote on the Extension Amendment Proposal, the NTA Amendment Proposal or Adjournment Proposal.

| Q. | Why should I vote “FOR”

the Extension Amendment Proposal? |

| A. | StoneBridge believes its shareholders

will benefit from StoneBridge consummating a Business Combination and is proposing the Extension Amendment Proposal to give the Company

the right to extend the Combination Period from January 20, 2024, up to 6 times for an additional one (1) month each time up to July

20, 2024. The Board believes that the current Termination Date will not provide sufficient time to complete a Business Combination. Given

StoneBridge’s commitment of time, effort and financial resources to date with respect to identifying a Business Combination target,

circumstances warrant providing Public Shareholders with additional time and opportunity to consider a prospective Business Combination.

However, even if the Extension Amendment Proposal is approved and the Extension is implemented, there is no assurance that StoneBridge

will be able to consummate a Business Combination within the Combination Period, as extended, given the actions that must occur prior

to closing of a Business Combination. |

In order to avail ourselves of the additional

one-month extension periods to consummate the Business Combination, the Sponsor or its affiliates or designees (together with the Sponsor,

the “Lender”), upon five days’ advance notice prior to the applicable Business Combination deadline, must deposit

into the Trust Account, on or prior to the date of the applicable Business Combination deadline $0.025 for each Class A ordinary share

outstanding after giving effect to the Redemption. If we complete our Business Combination, we would repay such loaned amounts out of

the proceeds of the Trust Account released to us or, at the option of the Lender, convert such loaned amounts into private placement warrants

of the post business combination entity at a price of $1.00 per warrant. If we do not complete a Business Combination, we will not repay

such loans. In the event that we receive notice from our Sponsor five days prior to the applicable Business Combination deadline of its

wish for us to effect an extension, we intend to issue a press release announcing such intention at least three days prior to the applicable

Business Combination deadline. In addition, we intend to issue a press release the day after the applicable Business Combination deadline

announcing whether or not the funds had been timely deposited. Our Sponsor and its affiliates or designees are not obligated to fund the

Trust Account to extend the time for us to complete our initial business combination.

The Board recommends that you vote in favor of

the Extension Amendment Proposal.

| Q. | Why should I vote “FOR”

the NTA Amendment Proposal? |

| A. | StoneBridge believes a Business

Combination will provide significant benefits to our shareholders and is proposing the NTA Amendment Proposal to add an additional basis

on which the Company may rely, as it has since its IPO, to be not subject to the “penny stock” rules of the SEC. The Company

believes that the NTA Requirement is not needed. The purpose of such limitation was initially to ensure that the Company would not become

subject to the SEC’s “penny stock” rules. Because the Public Shares would not be deemed to be “penny stock”

as such securities are listed on a national securities exchange, the Company is presenting the NTA Amendment Proposal to facilitate the

consummation of a Business Combination. |

StoneBridge believes that it can rely on other

available exclusions from the penny stock rules that would not impose restrictions on its net tangible assets. While the Company does

not believe this failure to satisfy the NTA Requirement subjects it to the SEC’s penny stock rules, as the NTA Requirement is included

in its Articles of Association, if the NTA Amendment Proposal is not approved, the Company may not be able to consummate its initial Business

Combination. The Articles of Association provides that the Company will not consummate a Business Combination unless it has net tangible

assets of at least $5,000,001 upon consummation of a Business Combination. If the NTA Amendment is not approved and there are significant

requests for redemption such that the NTA Requirement would not be satisfied, the Articles of Association would prevent the Company from

being able to consummate the Business Combination even if all other conditions to closing are met, forcing us to liquidate. If we liquidate,

our warrants will expire worthless and our investors would lose the investment opportunity associated with an investment in the combined

company, including through any potential price appreciation of our securities.

The Board recommends that you vote in favor of

the NTA Amendment Proposal.

| Q. | Why should I vote “FOR”

the Adjournment Proposal? |

| A. | If the Adjournment Proposal is

not approved by StoneBridge shareholders, the Board may not be able to adjourn the Extraordinary General Meeting to a later date or dates

in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Extension Amendment Proposal,

NTA Amendment Proposal, or implementation of the Extension. |

If presented, the Board recommends that you vote

in favor of the Adjournment Proposal.

| Q. | How will the initial shareholders

vote? |

| A. | The initial shareholders have

advised StoneBridge that they intend to vote any Ordinary Shares over which they have voting control, in favor of the Extension Amendment

Proposal, the NTA Amendment Proposal and, if necessary, the Adjournment Proposal. |

The initial shareholders and their respective

affiliates are not entitled to redeem any Founder Shares in connection with the Extension Amendment Proposal or NTA Amendment Proposal.

On the Record Date, the Sponsor, StoneBridge’s directors, officers and its initial shareholders and their respective affiliates

beneficially owned and were entitled to vote an aggregate of 5,000,000 Founder Shares held by the Sponsor and the officers and directors

of StoneBridge, representing approximately 67.3% of StoneBridge’s issued and outstanding Ordinary Shares. Accordingly, if all outstanding

Ordinary Shares are present at the Extraordinary General Meeting, then in addition to the Founder Shares, the Company will not need any

Public Shares to vote in favor of each of the Extension Amendment Proposal and the NTA Amendment Proposal to approve such proposals. If

only a minimum quorum of outstanding Ordinary Shares is present at the Extraordinary General Meeting, then no Public Shares will need

to vote in favor of the Extension Amendment Proposal or the NTA Amendment Proposal to approve such proposal. To approve the Adjournment

Proposal, regardless of whether all or a minimum quorum of outstanding Ordinary Shares are present at the Extraordinary General Meeting,

then in addition to the Founder Shares, the Company will need none of the Public Shares to vote in favor of the Adjournment Proposal to

approve such proposal. The Adjournment Proposal will only be put forth for a vote if there are not sufficient votes to approve the Extension

Amendment Proposal or the NTA Amendment Proposal at the Extraordinary General Meeting.

| Q. | What if I do not want to vote

“FOR” the Extension Amendment Proposal, the NTA Amendment Proposal or the Adjournment Proposal? |

| A. | If you do not want the Extension

Amendment Proposal, the NTA Amendment Proposal or the Adjournment Proposal to be approved, you must vote “AGAINST” such proposal. |

If you fail to vote by proxy or in person (including

virtually) at the Extraordinary General Meeting, or if you do not provide voting instructions to your broker, bank or nominee, your shares

will not be counted in connection with the determination of whether a valid quorum is established and, if a valid quorum is otherwise

established, such failure to vote will have no effect on the outcome of any vote on the Extension Amendment Proposal, the NTA Amendment

Proposal and the Adjournment Proposal.

If you vote to “ABSTAIN,” such abstentions

will be counted in connection with the determination of whether a valid quorum is established but will have no effect on the outcome of

the Extension Amendment Proposal, the NTA Amendment Proposal or the Adjournment Proposal.

If the Extension Amendment Proposal and NTA Amendment

Proposal are approved, the Adjournment Proposal will not be presented for a vote.

| Q. | What happens if the Extension

Amendment Proposal is not approved? |

| A. | If there are insufficient votes

to approve the Extension Amendment Proposal, StoneBridge may put the Adjournment Proposal to a vote in order to seek additional time

to obtain sufficient votes in support of the Extension. |

If the Extension Amendment Proposal is not approved

and a Business Combination is not consummated by the Termination Date, or such later date that may be approved by StoneBridge shareholders,

StoneBridge (i) will cease all operations except for the purpose of winding up; (ii) as promptly as reasonably possible but

not more than ten (10) business days thereafter subject to lawfully available funds therefor, redeem 100% of the Public Shares in

consideration of a per-share price, payable in cash, equal to the aggregate amount then on deposit in the Trust Account, including interest

earned on the funds held in the Trust Account and not previously released to the Company (less taxes payable and up to $100,000 of interest

to pay dissolution expenses), divided by the total number of then issued and outstanding Public Shares, which redemption will completely

extinguish rights of the holders of Public Shares (including the right to receive further liquidating distributions, if any), subject

to applicable law; and (iii) as promptly as reasonably possible following such redemption, subject to the approval of StoneBridge’s

remaining shareholders and the Board in accordance with applicable law, liquidate and dissolve, subject in each case to StoneBridge’s

obligations under Cayman Islands law, to provide for claims of creditors and other requirements of applicable law.

The Sponsor and the officers, directors and the

initial shareholders of StoneBridge waived their rights to participate in any liquidation distribution with respect to the 5,000,000 Founder

Shares held by them. There will be no distribution from the Trust Account with respect to StoneBridge’s warrants, which will expire