Filed Pursuant to Rule 433

Registration No. 333-201947

November 25, 2015

Investor Presentation November 2015 American CareSource Holdings, Inc.

2 Safe Harbor Statement & Free Writing Prospectus This free writing prospectus contains a presentation relating to the proposed public offering of securities of American CareSource Holdings, Inc . (the “Company," "we" or "us") and should be read together with the preliminary prospectus dated November 23 , 2015 that is included in Amendment No . 6 to the Registration Statement on Form S - 1 (File No . 333 - 201947 ) . The registration statement has not yet been declared effective . This presentation highlights basic information about us and the proposed public offering . Any statements that are not historical facts contained in this presentation (including, but not limited to statements that contain words such as “will,” “believes,” “plans,” “anticipates,” “expects,” and “estimates”), including with respect to the Company’s plans, objectives and expectations for future operations, projections of the Company’s future operating results or financial condition, and expectations regarding the healthcare industry and economic conditions, are forward - looking statements . Substantial risks and uncertainties could cause actual results to differ materially from those indicated by such forward - looking statements, including, but not limited to, our ability to attract and maintain patients, clients and providers and achieve our financial results ; our ability to raise additional capital to meet our liquidity needs ; changes in national healthcare policy, federal and state regulation, including without limitation the impact of the Patient Protection and Affordable Care Act, the Health Care and Educational Affordability Reconciliation Act and medical loss ratio regulations ; our intent to consummate the Medac Asset Acquisition ; our ability to complete the disposition of our ancillary network business to HealthSmart ; general economic conditions, including economic downturns and increases in unemployment ; our ability to successfully implement our growth strategy for the urgent and primary care business ; our ability to identify, acquire and integrate target urgent and primary care centers ; increased competition in the urgent and primary care market ; our ability to recruit and retain qualified physicians and other healthcare professionals ; reduction in reimbursement rates from governmental and commercial payors ; lower than anticipated demand and other risk factors detailed from time to time in the Company’s filings with the Securities and Exchange Commission (the “SEC”) . Except as otherwise required by law, the Company undertakes no obligation to update or revise these forward - looking statements to reflect events or circumstances after the date of this presentation . Because this presentation is a summary, it does not contain all of the information you should consider before investing in our common stock . Before you invest, you should carefully read the preliminary prospectus, the registration statement and any other documents incorporated by reference therein for more complete information about us and this proposed public offering before investing in our common stock . You may obtain these documents free of charge by searching the SEC online database (EDGAR) on the SEC web site at http : //www . sec . gov . Alternatively, a copy of the preliminary prospectus relating to the offering may be obtained, when available, by contacting Aegis Capital Corp . , Prospectus Department, 810 Seventh Ave, 18 th floor New York, NY 10019 , telephone : 212 . 600 . 2725 , e - mail : prospectus@aegiscap . com .

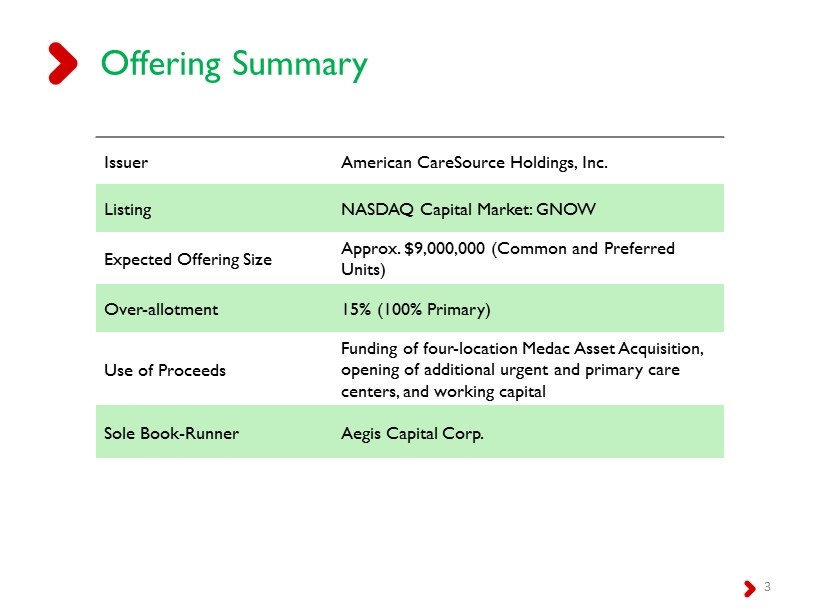

3 Offering Summary Issuer American CareSource Holdings, Inc. Listing NASDAQ Capital Market: GNOW Expected Offering Size Approx. $9,000,000 (Common and Preferred Units ) Over - allotment 15% (100% Primary) Use of Proceeds Funding of four - location Medac Asset Acquisition, opening of additional urgent and primary care centers, and working capital Sole Book - Runner Aegis Capital Corp.

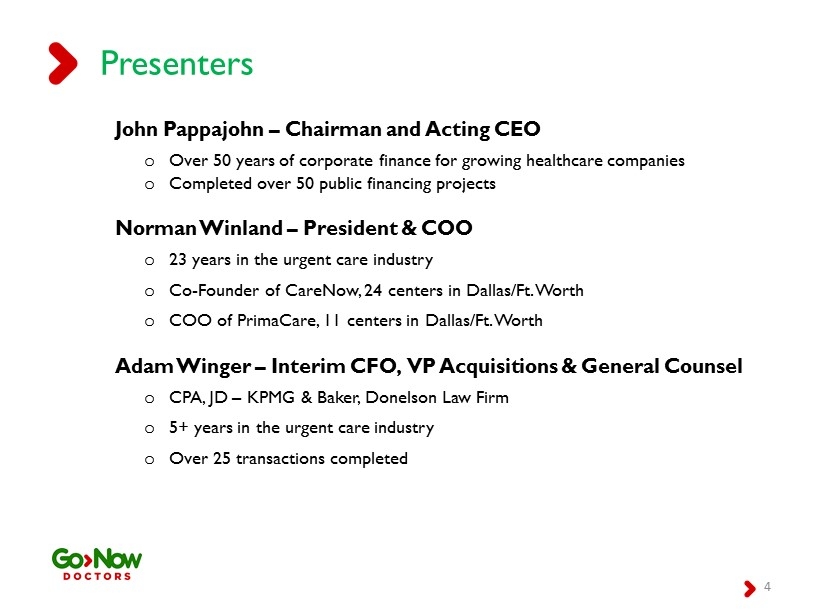

4 Presenters John Pappajohn – Chairman and Acting CEO o Over 50 years of corporate finance for growing healthcare companies o Completed over 50 public financing projects Norman Winland – President & COO o 23 years in the urgent care industry o Co - Founder of CareNow , 24 centers in Dallas/Ft. Worth o COO of PrimaCare , 11 centers in Dallas/Ft. Worth Adam Winger – Interim CFO, VP Acquisitions & General Counsel o CPA, JD – KPMG & Baker, Donelson Law Firm o 5+ years in the urgent care industry o Over 25 transactions completed

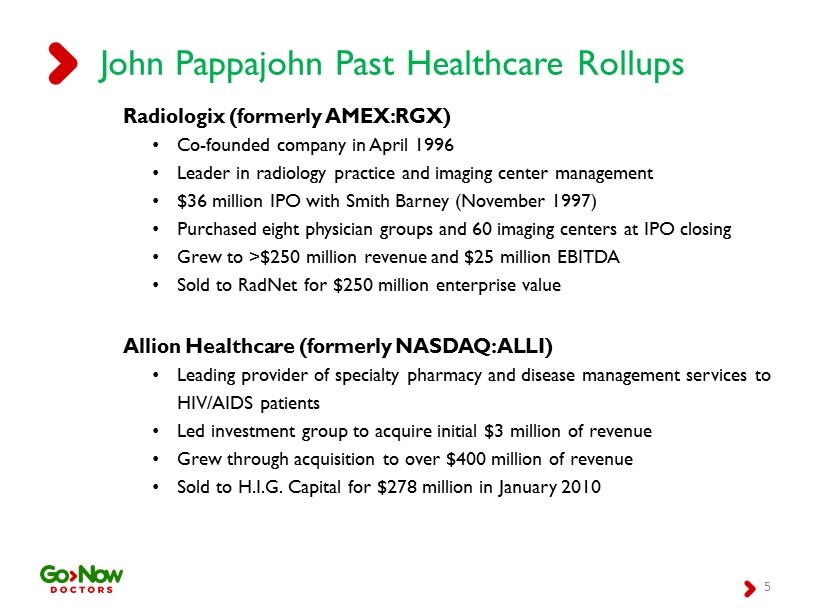

5 John Pappajohn Past Healthcare Rollups Radiologix (formerly AMEX:RGX) • Co - founded company in April 1996 • Leader in radiology practice and imaging center management • $36 million IPO with Smith Barney (November 1997) • Purchased eight physician groups and 60 imaging centers at IPO closing • Grew to >$250 million revenue and $25 million EBITDA • Sold to RadNet for $250 million enterprise value Allion Healthcare (formerly NASDAQ:ALLI) • Leading provider of specialty pharmacy and disease management services to HIV/AIDS patients • Led investment group to acquire initial $3 million of revenue • Grew through acquisition to over $400 million of revenue • Sold to H.I.G. Capital for $278 million in January 2010

6 Urgent and primary care brand of American CareSource Holdings, Inc .

7 Executive Summary Urgent Care Business • Owner and operator of convenient, affordable, and comprehensive medical care centers • Care for busy families and employers • Like going to the “store” for health care • Quality care from great doctors & comfortable facilities • Delivered every day, evenings & weekends, with no appointment • Pursuing high - growth strategy in large, fragmented industry

8 The Opportunity Publicly - traded, Pure - Play Urgent Care Consolidator • Plans to Exit the Legacy Business Expansive, Fragmented, and Growing Industry • Approximately 9,000 Urgent Care Centers in U.S. in 2013 • 71% of 2012 Owners owned 1 - 2 centers Planned Aggressive Growth Strategy • 90 Centers by end of 2017 Attractive Arbitrage Opportunity • Acquisition targets of small operators at 4X – 5X EBITDA multiples • Recent large operator purchase price multiples between 10X - 15X EBITDA • New center investment of $550K can yield $3.2 million of enterprise value Experienced Board and Management Team Source: IBISWorld Industry Report 2013

9 Model Clinic Financial Profile Model Clinic P&L Net Revenue $ 1,403,000 Fixed Costs (salaries, wages and rent) (743,000) Other Operating Expense (338,000) EBITDA $ 323,000 Profit Margin 23% Key Assumptions : • 33 patients per day • Clinic Open 362 days per year • Net Reimbursement Rate of $ 118 per patient

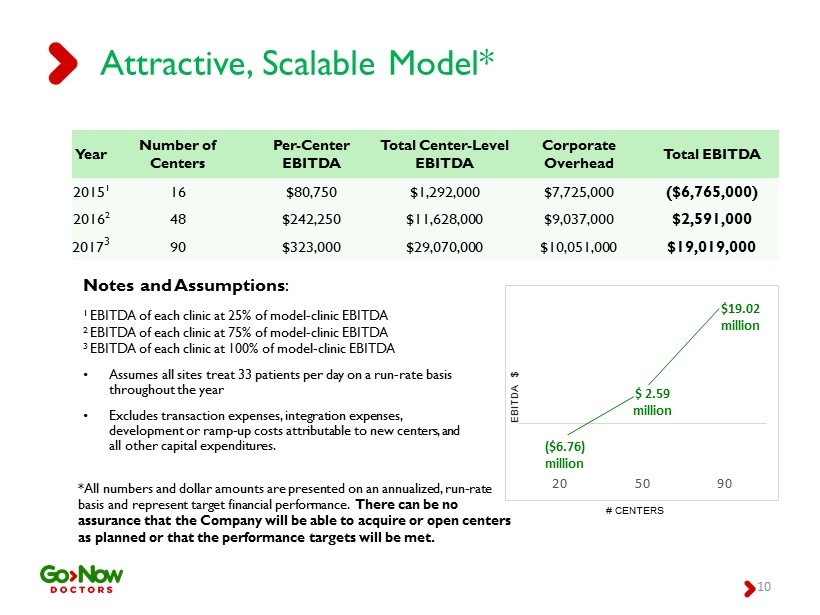

10 Attractive, Scalable Model* Year Number of Centers Per - Center EBITDA Total Center - Level EBITDA Corporate Overhead Total EBITDA 2015 1 16 $80,750 $1,292,000 $7,725,000 ($6,765,000) 2016 2 48 $242,250 $11,628,000 $9,037,000 $2,591,000 2017 3 90 $323,000 $ 29,070,000 $10,051,000 $19,019,000 Notes and Assumptions : 1 EBITDA of each clinic at 25% of model - clinic EBITDA 2 EBITDA of each clinic at 75% of model - clinic EBITDA 3 EBITDA of each clinic at 100% of model - clinic EBITDA • Assumes all sites treat 33 patients per day on a run - rate basis throughout the year • Excludes transaction expenses, integration expenses, development or ramp - up costs attributable to new centers, and all other capital expenditures. ($6.76) million $ 2.59 million $19.02 million 20 50 90 # CENTERS *A ll numbers and dollar amounts are presented on an annualized, run - rate basis and represent target financial performance. There can be no assurance that the Company will be able to acquire or open centers as planned or that the performance targets will be met. EBITDA $

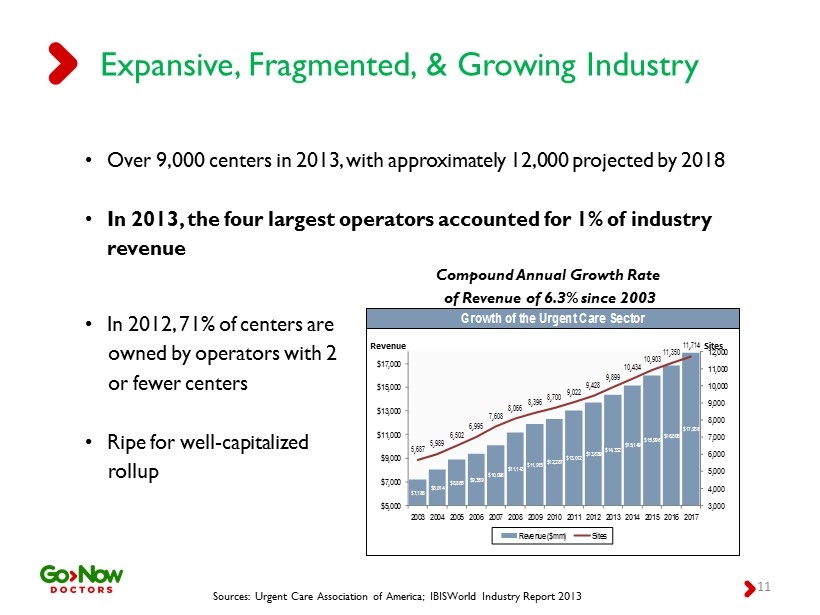

11 Expansive, Fragmented, & Growing Industry • Over 9,000 centers in 2013, with approximately 12,000 projected by 2018 • In 2013, the four largest operators accounted for 1% of industry revenue Compound Annual Growth Rate of Revenue of 6.3% since 2003 • In 2012, 71% of centers are owned by operators with 2 or fewer centers • Ripe for well - capitalized rollup Sources: Urgent Care Association of America; IBISWorld Industry Report 2013 Growth of the Urgent Care Sector $7,188 $8,014 $8,865 $9,359 $10,096 $11,143 $11,915 $12,287 $13,012 $13,689 $14,332 $15,149 $15,996 $16,806 $17,936 5,687 5,989 6,502 6,995 7,608 8,066 8,396 8,700 9,022 9,428 9,899 10,434 10,903 11,350 11,714 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000 11,000 12,000 $5,000 $7,000 $9,000 $11,000 $13,000 $15,000 $17,000 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Revenue ($mm) Sites Revenue Sites

12 Retail Healthcare Delivery Advantages Over the Emergency Room • Shorter Wait Times • Conveniently Located • More Inviting and Comfortable Environment • More Affordable *90 % of patients wait less than 30 minutes to see a physician Advantages Over Traditional Primary Care Physician • Immediate Access, No Appointment • Extended Hours - Open Evenings, Weekends, Holidays • Convenient Locations Sources: Urgent Care Association of America, IBISWorld Industry Report 2013, NCHS Data Brief August 2012 Emergency Room Urgent Care Total Time in Facility 4 hours 1 hour* Gross Cost of Care $922 $215

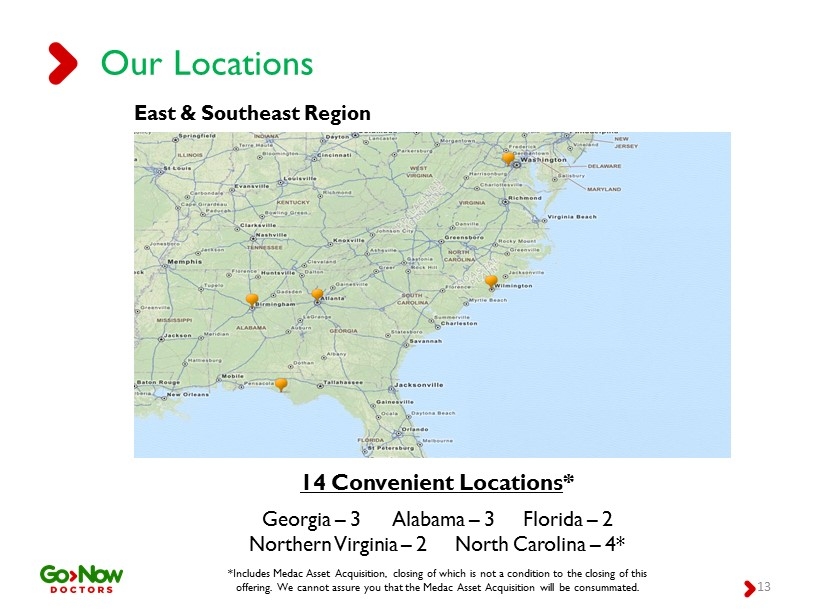

13 Our Locations East & Southeast Region 14 Convenient Locations * Georgia – 3 Alabama – 3 Florida – 2 Northern Virginia – 2 North Carolina – 4* *Includes Medac Asset Acquisition, c losing of which is not a condition to the closing of this offering. We cannot assure you that the Medac Asset Acquisition will be consummated.

14 Locally - Clustered Clinics Atlanta, Georgia Birmingham, Alabama • Clustering promotes staffing efficiencies • Efficiencies of scale in marketing are achieved • Clustering accomplished through de novo development

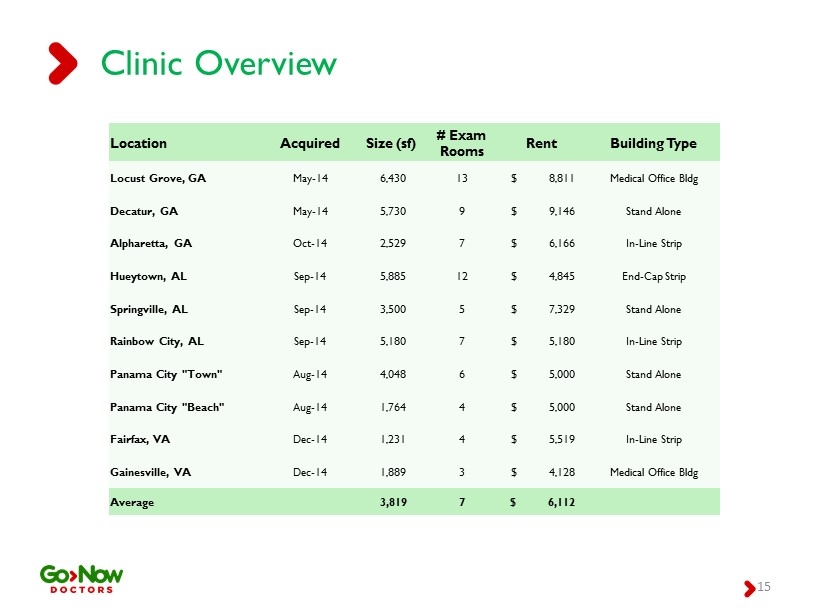

15 Clinic Overview Location Acquired Size (sf) # Exam Rooms Rent Building Type Locust Grove, GA May - 14 6,430 13 $ 8,811 Medical Office Bldg Decatur, GA May - 14 5,730 9 $ 9,146 Stand Alone Alpharetta, GA Oct - 14 2,529 7 $ 6,166 In - Line Strip Hueytown, AL Sep - 14 5,885 12 $ 4,845 End - Cap Strip Springville, AL Sep - 14 3,500 5 $ 7,329 Stand Alone Rainbow City, AL Sep - 14 5,180 7 $ 5,180 In - Line Strip Panama City "Town" Aug - 14 4,048 6 $ 5,000 Stand Alone Panama City "Beach" Aug - 14 1,764 4 $ 5,000 Stand Alone Fairfax, VA Dec - 14 1,231 4 $ 5,519 In - Line Strip Gainesville, VA Dec - 14 1,889 3 $ 4,128 Medical Office Bldg Average 3,819 7 $ 6,112

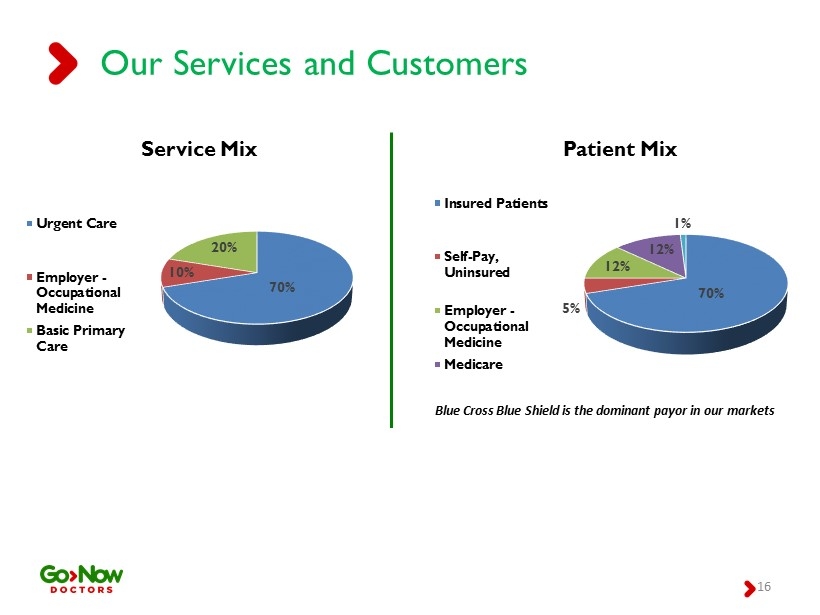

16 Our Services and Customers 70% 10% 20% Service Mix Urgent Care Employer - Occupational Medicine Basic Primary Care 70% 5% 12% 12% 1% Patient Mix Insured Patients Self-Pay, Uninsured Employer - Occupational Medicine Medicare Blue Cross Blue Shield is the dominant payor in our markets

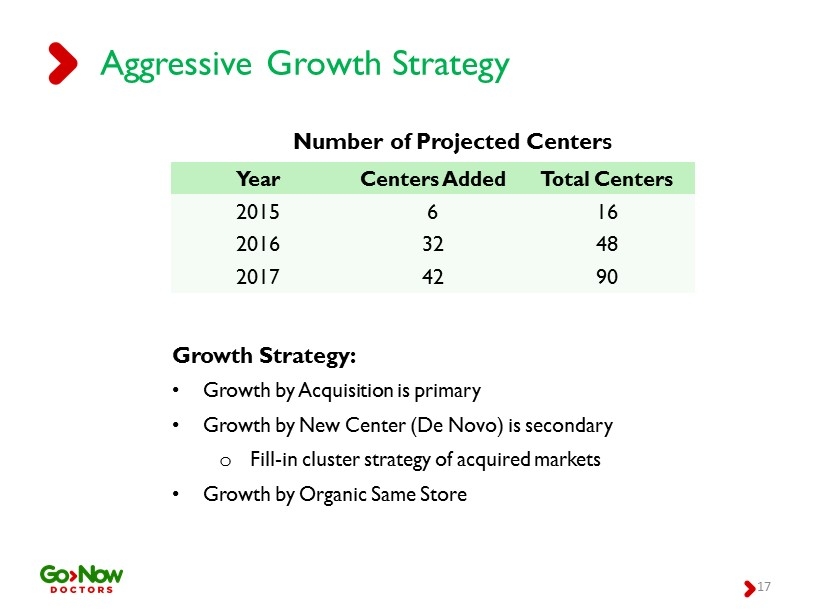

17 Aggressive Growth Strategy Year Centers Added Total Centers 2015 6 16 2016 32 48 2017 42 90 Number of Projected Centers Growth Strategy: • Growth by Acquisition is primary • Growth by New Center (De Novo ) is secondary o Fill - in cluster strategy of acquired markets • Growth by Organic Same Store

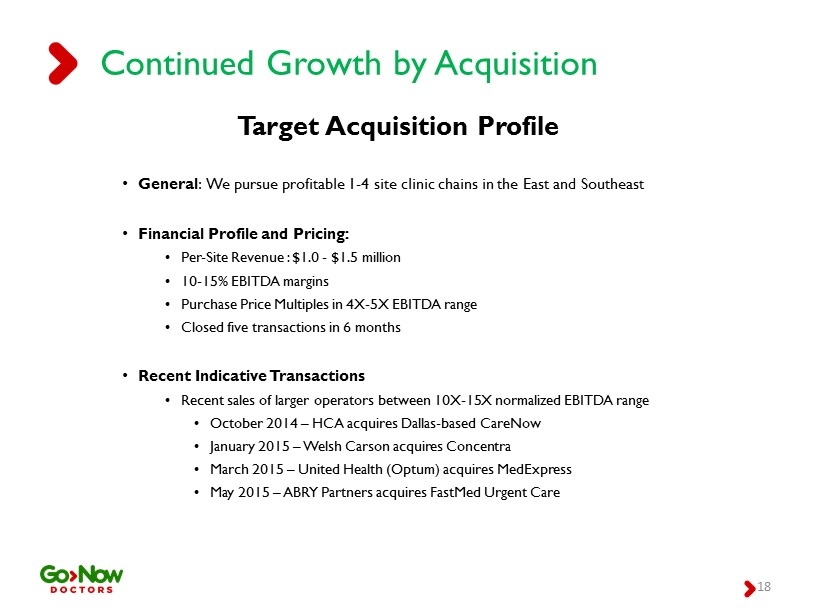

18 Continued Growth by Acquisition Target Acquisition Profile • General : We pursue profitable 1 - 4 site clinic chains in the East and Southeast • Financial Profile and Pricing: • Per - Site Revenue : $1.0 - $1.5 million • 10 - 15% EBITDA margins • Purchase Price Multiples in 4X - 5X EBITDA range • Closed five transactions in 6 months • Recent Indicative Transactions • Recent sales of larger operators between 10X - 15X normalized EBITDA range • October 2014 – HCA acquires Dallas - based CareNow • January 2015 – Welsh Carson acquires Concentra • March 2015 – United Health ( Optum ) acquires MedExpress • May 2015 – ABRY Partners acquires FastMed Urgent Care

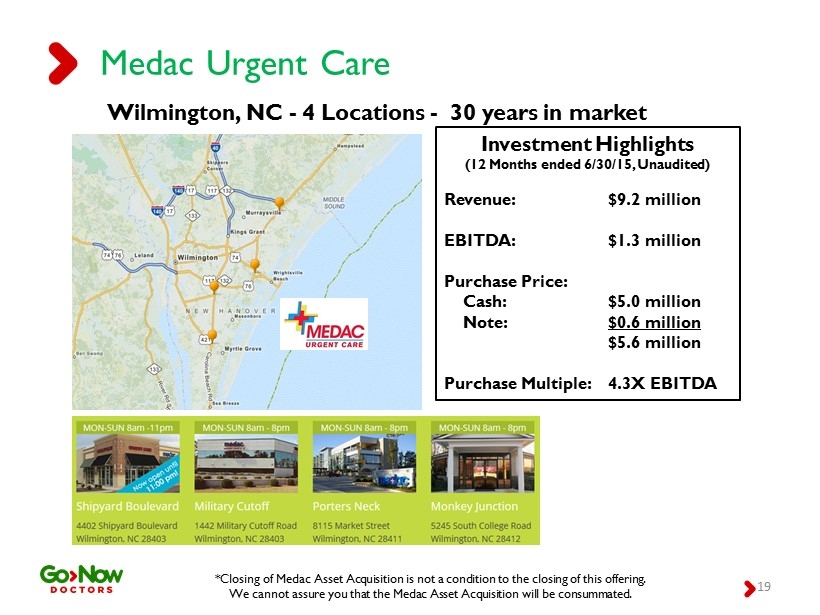

19 Medac Urgent Care Wilmington, NC - 4 Locations - 30 years in market Investment Highlights (12 Months ended 6/30/15, Unaudited) Revenue: $9.2 million EBITDA: $1.3 million Purchase Price: Cash: $5.0 million Note: $0.6 million $5.6 million Purchase Multiple: 4.3X EBITDA *Closing of Medac Asset Acquisition is not a condition to the closing of this offering. We cannot assure you that the Medac Asset Acquisition will be consummated.

20 Acquisition Pipeline and Lead Sourcing Pipeline • Various stages of discussion with several owners Lead Sourcing • Extensive broker/banker and industry relationships • Trade shows such as UCAOA • Unique offering structure with public equity

21 De Novo Strategy Site Selection • Identify complimentary locations in existing markets • Industry leader in site selection on our team • Access to an e xtensive database of urgent care operators • Numerous sites have been targeted Target Retail Space • End cap strip mall locations • Free standing, b uild - to - suit construction • High - visibility, ease of access, high traffic counts • Moms pass the site multiple times per week

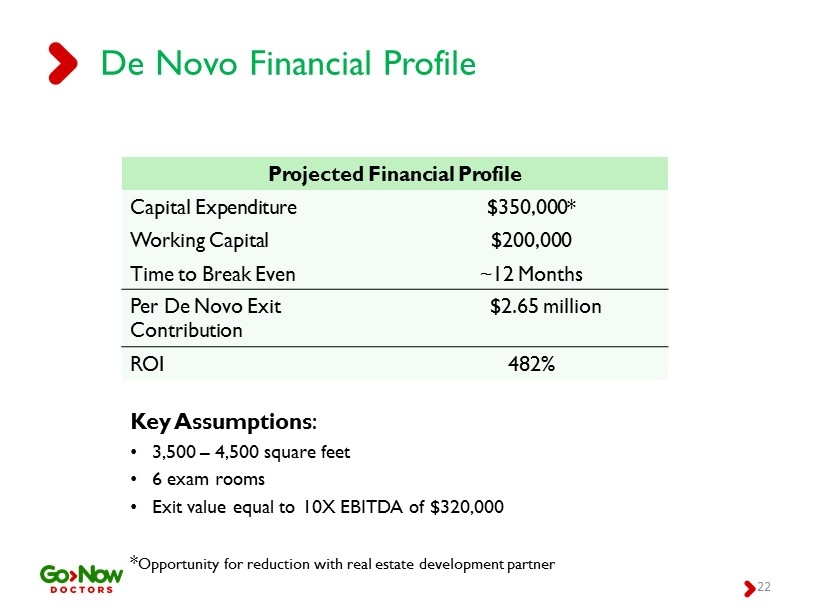

22 De Novo Financial Profile Projected Financial Profile Capital Expenditure $350,000* Working Capital $200,000 Time to Break Even ~1 2 Months Per De Novo Exit Contribution $2.65 million ROI 482% Key Assumptions : • 3,500 – 4,500 square feet • 6 exam rooms • Exit value equal to 10X EBITDA of $320,000 * Opportunity for reduction with real estate development partner

23 Same Store Organic Growth • Short, memorable, retail name • Busy families want convenient care • Like going to the “store” for healthcare • Communicates immediate access to care, no appointment • Applies to both urgent and primary care • Green = Go. Red = Urgent. Renderings of post - rebranding signage, which we intend to use at certain of our GoNow Doctors locations.

24 Same Store Organic Growth Implement marketing & advertising • 23% Projected patient growth for existing 10 centers Broaden service offering • Increase occupational medicine patients • Increase self - pay patients with simplified pricing • Expand hours and days open at select centers Increase insurance reimbursement Improved physician recruitment Implement best practices across platform • GPO contract to reduce expenses • Standardize vendors • Centralize certain activities at corporate

25 Marketing & Advertising Strategy Who We Target • Mother of an insured household with school - age children. • Busy suburban families where convenience is the priority. Tools We Use • Grass roots advertising, billboards, radio, and print advertising • Online SEO marketing & social media • Expert demographic analytics help us know our customer • Branded promo items that make it into mom’s purse Grass Roots Advertising • Cost - Effective , Community Marketing: School sports programs, school nurses, elementary school folders, children’s dance studios, gymnastic events, day care relationships, school bands, children’s sports teams, parent - child related event sponsorships, and family publications.

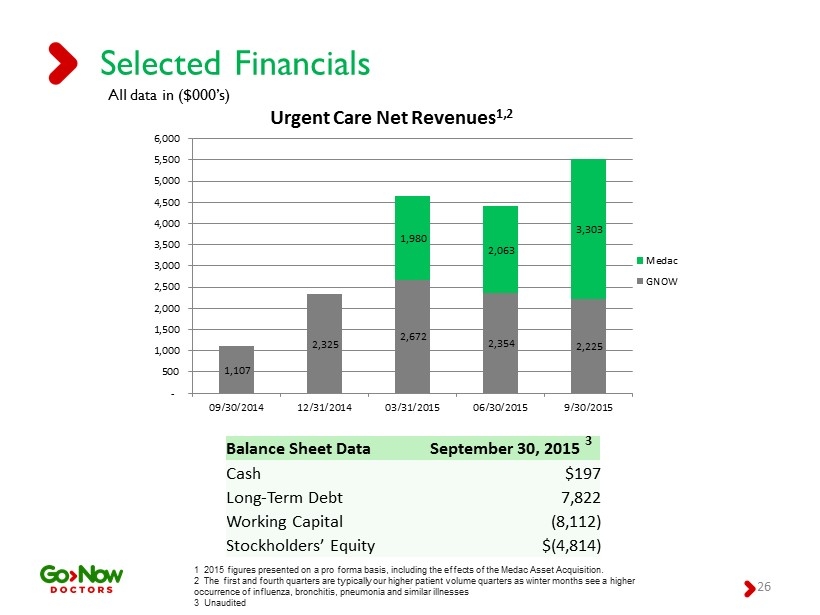

26 Selected Financials All data in ($000’s) Balance Sheet Data September 30, 2015 Cash $197 Long - Term Debt 7,822 Working Capital (8,112) Stockholders’ Equity $(4,814) 1 2015 figures presented on a pro forma basis, including the effects of the Medac Asset Acquisition. 2 The first and fourth quarters are typically our higher patient volume quarters as winter months see a higher occurrence of influenza, bronchitis , pneumonia and similar illnesses 3 Unaudited 3 1,107 2,325 2,672 2,354 2,225 1,980 2,063 3,303 - 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 09/30/2014 12/31/2014 03/31/2015 06/30/2015 9/30/2015 Urgent Care Net Revenues 1,2 Medac GNOW

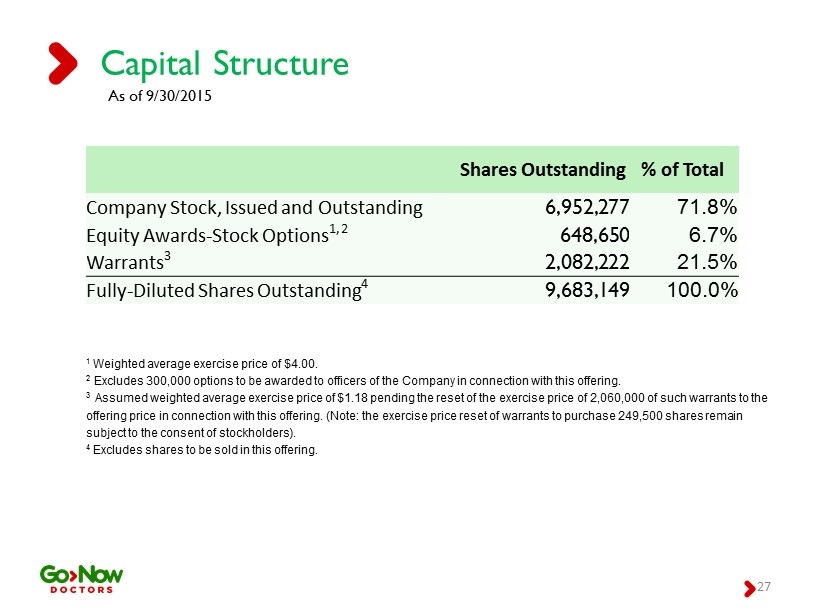

27 Capital Structure As of 9/30/2015 Shares Outstanding % of Total Company Stock, Issued and Outstanding 6,952,277 71.8% Equity Awards - Stock Options 1, 2 648,650 6.7% Warrants 3 2,082,222 21.5% Fully - Diluted Shares Outstanding 4 9,683,149 100.0% 1 Weighted average exercise price of $4.00. 2 Excludes 300,000 options to be awarded to officers of the Company in connection with this offering. 3 Assumed weighted average exercise price of $1.18 pending the reset of the exercise price of 2,060,000 of such warrants to the offering price in connection with this offering. (Note: the exercise price reset of warrants to purchase 249,500 shares remai n subject to the consent of stockholders). 4 E xcludes shares to be sold in this offering.

28 Summary • Publicly - traded pure - play urgent care company • Urgent care industry is ripe for consolidation • By 2017, we plan to have built or acquired 90 clinics • Highly attractive arbitrage opportunity • Highly experienced board and management team

American CareSource (CE) (USOTC:GNOW)

Gráfica de Acción Histórica

De Abr 2024 a May 2024

.")

American CareSource (CE) (USOTC:GNOW)

Gráfica de Acción Histórica

De May 2023 a May 2024

.")