Form 8-K - Current report

06 Noviembre 2024 - 3:32PM

Edgar (US Regulatory)

false

0001526113

0001526113

2024-11-06

2024-11-06

0001526113

us-gaap:CommonStockMember

2024-11-06

2024-11-06

0001526113

us-gaap:SeriesAPreferredStockMember

2024-11-06

2024-11-06

0001526113

us-gaap:SeriesBPreferredStockMember

2024-11-06

2024-11-06

0001526113

us-gaap:SeriesDPreferredStockMember

2024-11-06

2024-11-06

0001526113

us-gaap:SeriesEPreferredStockMember

2024-11-06

2024-11-06

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED STATES

SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of The Securities

Exchange Act of 1934

Date of Report (Date of earliest event reported):

November 6, 2024

Global Net Lease, Inc.

(Exact name of registrant as specified in its

charter)

| Maryland |

|

001-37390 |

|

45-2771978 |

(State or other jurisdiction

of incorporation) |

|

(Commission File Number) |

|

(IRS Employer

Identification No.) |

| 650 Fifth Avenue, 30th Floor |

|

|

| New York, New York |

|

10019 |

| (Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number,

including area code: (332) 265-2020

(Former name or former address, if changed since

last report.)

Check the appropriate box below if the Form 8-K filing is intended

to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| |

|

| ¨ |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| |

|

| ¨ |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| |

|

| ¨ |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange

on which registered |

| Common

Stock, $0.01 par value per share |

|

GNL |

|

New York Stock Exchange |

| 7.25%

Series A Cumulative Redeemable Preferred Stock, $0.01 par value per share |

|

GNL PR A |

|

New York Stock Exchange |

| 6.875%

Series B Cumulative Redeemable Perpetual Preferred Stock, $0.01 par value per share |

|

GNL PR B |

|

New York Stock Exchange |

| 7.50% Series D Cumulative Redeemable Perpetual Preferred Stock, $0.01 par

value per share |

|

GNL PR D |

|

New York Stock Exchange |

| 7.375%

Series E Cumulative Redeemable Perpetual Preferred Stock, $0.01 par value per share |

|

GNL PR E |

|

New York Stock Exchange |

Indicate

by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405

of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ¨

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

¨

Item 7.01 Regulation FD Disclosure.

On November 6, 2024,

Global Net Lease, Inc. (the “Company”) prepared an investor presentation that officers and other representatives of the Company

intend to present at conferences and meetings. A copy of the investor presentation is furnished as Exhibit 99.1 of this Current Report

on Form 8-K. The information set forth in Item 7.01 of this Current Report on Form 8-K and in the attached Exhibit 99.1 is deemed to be

“furnished” and shall not be deemed to be “filed” for purposes of Section 18 of the Securities Exchange Act of

1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that Section. The information set forth

in Item 7.01 of this Current Report on Form 8-K, including Exhibit 99.1, shall not be deemed incorporated by reference into any filing

under the Exchange Act or the Securities Act of 1933, as amended, regardless of any general incorporation language in such filing.

The statements in this

Current Report on Form 8-K that are not historical facts may be forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995. These forward-looking statements involve risks and uncertainties that could cause the outcome to be materially

different. The words such as “may,” “will,” “seeks,” “anticipates,” “believes,”

“expects,” “estimates,” “projects,” “potential,” “predicts,” “plans,”

“intends,” “would,” “could,” “should” and similar expressions are intended to identify

forward-looking statements, although not all forward-looking statements contain these identifying words. These forward-looking statements

are subject to a number of risks, uncertainties and other factors, many of which are outside of the Company’s control, which could

cause actual results to differ materially from the results contemplated by the forward-looking statements. These risks and uncertainties

include the risks associated with realization of the anticipated benefits of the merger with The Necessity Retail REIT, Inc. and the internalization

of the Company’s property management and advisory functions; that any potential future acquisition or disposition by the Company

is subject to market conditions and capital availability and may not be identified or completed on favorable terms, or at all. Some of

the risks and uncertainties, although not all risks and uncertainties, that could cause the Company’s actual results to differ materially

from those presented in its forward-looking statements are set forth in the Risk Factors and “Quantitative and Qualitative Disclosures

About Market Risk” sections in the Company’s Annual Report on Form 10-K, its Quarterly Reports on Form 10-Q, and all of its

other filings with the U.S. Securities and Exchange Commission, as such risks, uncertainties and other important factors may be updated

from time to time in the Company’s subsequent reports. Further, forward-looking statements speak only as of the date they are made,

and the Company undertakes no obligation to update or revise any forward-looking statement to reflect changed assumptions, the occurrence

of unanticipated events or changes to future operating results over time, unless required by law.

Item 9.01 Financial Statements and Exhibits.

(d) Exhibits.

Exhibit

Number |

|

Description |

| 99.1 |

|

Investor Presentation. |

| 104 |

|

Cover Page Interactive Data File - the cover page XBRL tags are embedded within the Inline XBRL document. |

SIGNATURES

Pursuant to the requirements

of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto

duly authorized.

| |

|

|

GLOBAL NET LEASE, INC. |

| |

|

|

|

| Date: |

November 6, 2024 |

By: |

/s/ Edward M. Weil, Jr. |

| |

|

Name: |

Edward M. Weil, Jr. |

| |

|

Title: |

Chief Executive Officer and President (Principal Executive Officer) |

Exhibit 99.1

| Global Net Lease

Third Quarter 2024 Investor Presentation Pictured – McLaren Campus in Woking, U.K. |

| 1

FORWARD LOOKING STATEMENTS

This presentation contains statements that are not historical facts and may be forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995, including statements regarding the timing and consideration related to our anticipated acquisitions and

dispostions, the intent, belief or current expectations of us, our operating partnership and members of our management team, as well as the

assumptions on which such statements are based, and generally are identified by the use of words such as “may,” “will,” “seeks,” “anticipates,”

“believes,” “expects,” “estimates,” “projects,” “potential,” “predicts,” “plans,” “intends,” “would,” “could,” “should” or similar expressions are

intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

These forward-looking statements are subject to risks, uncertainties, and other factors, many of which are outside of our control, which could

cause actual results to differ materially from the results contemplated by the forward-looking statements. These risks and uncertainties include the

risks associated with realization of the anticipated benefits of the merger with The Necessity Retail REIT, Inc. (“RTL”) and the internalization of

our property management and advisory functions; that any potential future acquisition or disposition by us is subject to market conditions and

capital availability and may not be identified or completed on favorable terms, or at all. Some of the risks and uncertainties, although not all risks

and uncertainties, that could cause our actual results to differ materially from those presented in our forward-looking statements are set forth

under “Risk Factors” and “Quantitative and Qualitative Disclosures about Market Risk” sections in our Annual Report on Form 10-K, our

Quarterly Reports on Form 10-Q and our other filings with the U.S Securities and Exchange Commission (“SEC”) as such risks, uncertainties and

other important factors may be updated from time to time in our subsequent reports. Further, forward-looking statements speak only as of the

date they are made, and we undertake no obligation to update or revise any forward-looking statement to reflect changed assumptions, the

occurrence of unanticipated events or changes to future operating results over time, unless required by law. |

| 2

This presentation also includes estimated projections of future operating results. These projections are not prepared in accordance with published

guidelines of the SEC or the guidelines established by the American Institute of Certified Public Accountants for preparation and presentation of

financial projections. This information is not fact and should not be relied upon as being necessarily indicative of future results; the projections

were prepared in good faith by management and are based on numerous assumptions that may prove to be wrong. All such statements, including

but not limited to estimates of value accretion, synergies, run-rate or annualized figures and results of future operations after making adjustments

to give effect to assumed future operations reflect assumptions as to certain business decisions and events that are subject to change. As a result,

actual results may differ materially from those contained in the estimates. Accordingly, there can be no assurance that the estimates will be realized,

or that the projections described in this presentation will be realized at all.

This presentation also contains estimates and information concerning our industry and tenants, including market position, market size and growth

rates of the markets in which we operate, that are based on industry publications and other third-party reports. This information involves a

number of assumptions and limitations, and you are cautioned not to give undue weight to these estimates. We have not independently verified the

accuracy or completeness of the data contained in these publications and reports. The industry in which we operate is subject to a high degree of

uncertainty and risk due to a variety of factors, including those described in the “Risk Factors”, “Management’s Discussion and Analysis of

Financial Condition and Results of Operations” and “Quantitative and Qualitative Disclosures about Market Risk” sections of the Company’s

Annual Report on Form 10-K, and all other filings with the SEC after that date, as such risks, uncertainties and other important factors may be

updated from time to time in the Company’s subsequent reports.

Credit Ratings

A securities rating is not a recommendation to buy, sell or hold securities and may be subject to revision or withdrawal at any time. Each rating

agency has its own methodology of assigning ratings and, accordingly, each rating should be evaluated independently of any other rating.

PROJECTIONS |

| 3

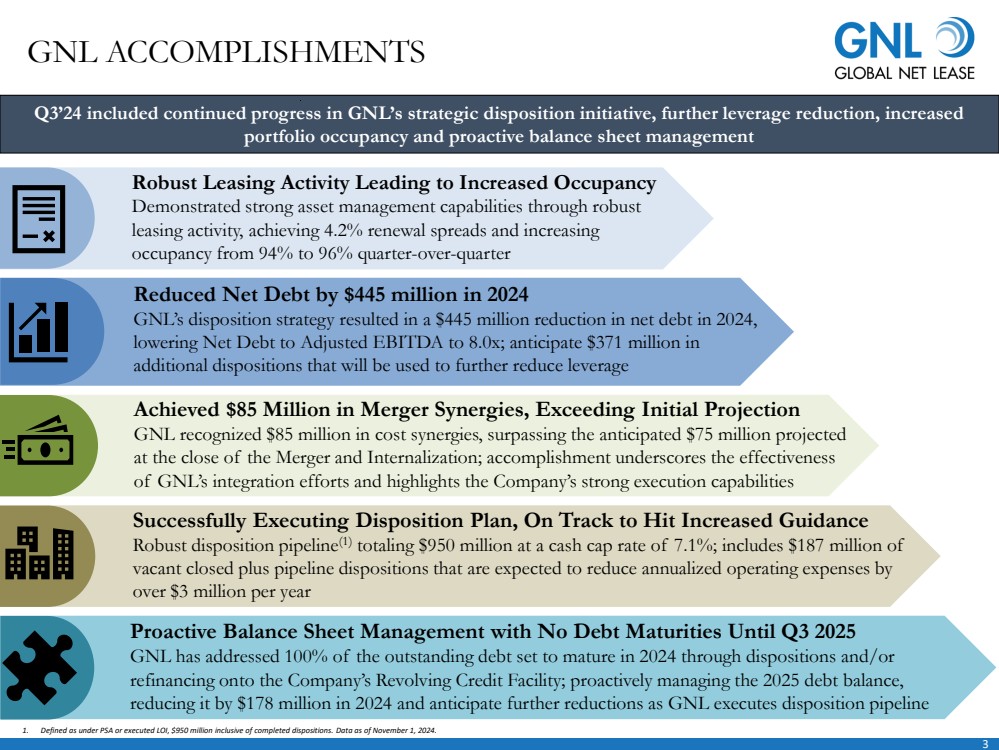

Proactive Balance Sheet Management with No Debt Maturities Until Q3 2025

GNL has addressed 100% of the outstanding debt set to mature in 2024 through dispositions and/or

refinancing onto the Company’s Revolving Credit Facility; proactively managing the 2025 debt balance,

reducing it by $178 million in 2024 and anticipate further reductions as GNL executes disposition pipeline

GNL ACCOMPLISHMENTS

Q3’24 included continued progress in GNL’s strategic disposition initiative, further leverage reduction, increased

portfolio occupancy and proactive balance sheet management

Robust Leasing Activity Leading to Increased Occupancy

Demonstrated strong asset management capabilities through robust

leasing activity, achieving 4.2% renewal spreads and increasing

occupancy from 94% to 96% quarter-over-quarter

Reduced Net Debt by $445 million in 2024

GNL’s disposition strategy resulted in a $445 million reduction in net debt in 2024,

lowering Net Debt to Adjusted EBITDA to 8.0x; anticipate $371 million in

additional dispositions that will be used to further reduce leverage

Achieved $85 Million in Merger Synergies, Exceeding Initial Projection

GNL recognized $85 million in cost synergies, surpassing the anticipated $75 million projected

at the close of the Merger and Internalization; accomplishment underscores the effectiveness

of GNL’s integration efforts and highlights the Company’s strong execution capabilities

Successfully Executing Disposition Plan, On Track to Hit Increased Guidance

Robust disposition pipeline(1) totaling $950 million at a cash cap rate of 7.1%; includes $187 million of

vacant closed plus pipeline dispositions that are expected to reduce annualized operating expenses by

over $3 million per year

1. Defined as under PSA or executed LOI, $950 million inclusive of completed dispositions. Data as of November 1, 2024. |

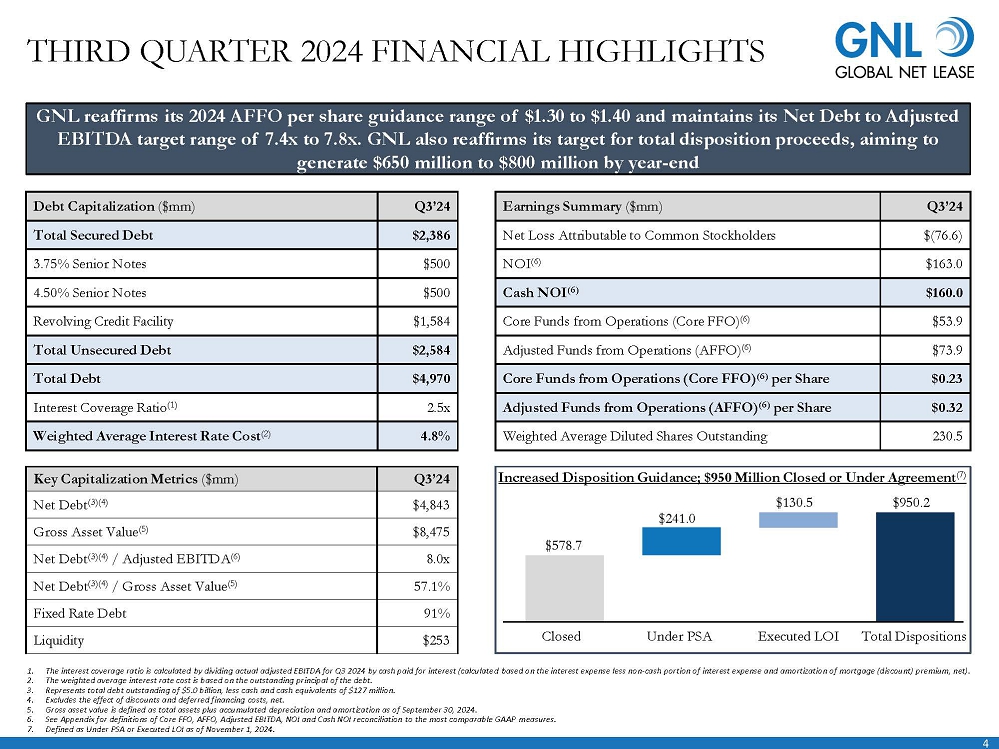

| 4

Earnings Summary ($mm) Q3’24

Net Loss Attributable to Common Stockholders $(76.6)

NOI(6) $163.0

Cash NOI(6) $160.0

Core Funds from Operations (Core FFO)(6) $53.9

Adjusted Funds from Operations (AFFO)

(6) $73.9

Core Funds from Operations (Core FFO)(6) per Share $0.23

Adjusted Funds from Operations (AFFO)(6) per Share $0.32

Weighted Average Diluted Shares Outstanding 230.5

THIRD QUARTER 2024 FINANCIAL HIGHLIGHTS

Key Capitalization Metrics ($mm) Q3’24

Net Debt(3)(4) $4,843

Gross Asset Value(5) $8,475

Net Debt(3)(4) / Adjusted EBITDA(6) 8.0x

Net Debt(3)(4) / Gross Asset Value(5) 57.1%

Fixed Rate Debt 91%

Liquidity $253

Debt Capitalization ($mm) Q3’24

Total Secured Debt $2,386

3.75% Senior Notes $500

4.50% Senior Notes $500

Revolving Credit Facility $1,584

Total Unsecured Debt $2,584

Total Debt $4,970

Interest Coverage Ratio(1) 2.5x

Weighted Average Interest Rate Cost(2) 4.8%

GNL reaffirms its 2024 AFFO per share guidance range of $1.30 to $1.40 and maintains its Net Debt to Adjusted

EBITDA target range of 7.4x to 7.8x. GNL also reaffirms its target for total disposition proceeds, aiming to

generate $650 million to $800 million by year-end

1. The interest coverage ratio is calculated by dividing actual adjusted EBITDA for Q3 2024 by cash paid for interest (calculated based on the interest expense less non-cash portion of interest expense and amortization of mortgage (discount) premium, net).

2. The weighted average interest rate cost is based on the outstanding principal of the debt.

3. Represents total debt outstanding of $5.0 billion, less cash and cash equivalents of $127 million.

4. Excludes the effect of discounts and deferred financing costs, net.

5. Gross asset value is defined as total assets plus accumulated depreciation and amortization as of September 30, 2024.

6. See Appendix for definitions of Core FFO, AFFO, Adjusted EBITDA, NOI and Cash NOI reconciliation to the most comparable GAAP measures.

7. Defined as Under PSA or Executed LOI as of November 1, 2024.

Increased Disposition Guidance; $950 Million Closed or Under Agreement(7)

Closed Under PSA Executed LOI Total Dispositions

$578.7

$241.0

$130.5 $950.2 |

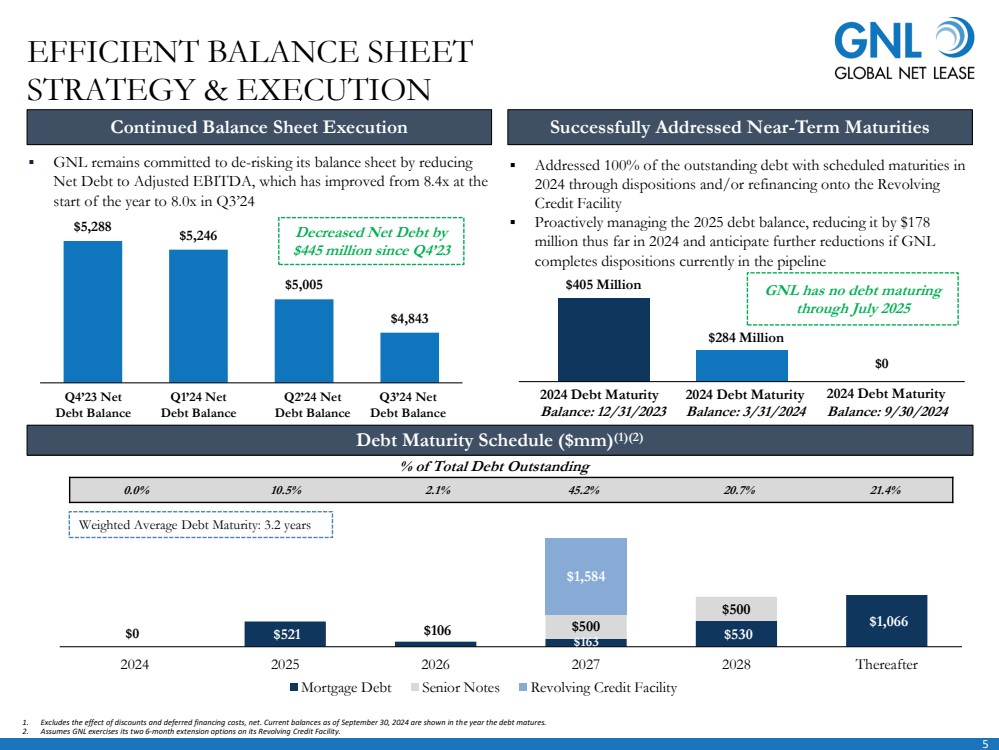

| 5

$5,288 $5,246

$5,005

$4,843

▪ GNL remains committed to de-risking its balance sheet by reducing

Net Debt to Adjusted EBITDA, which has improved from 8.4x at the

start of the year to 8.0x in Q3’24

$521 $106

$163 $530

$1,066 $500

$500

$1,584

2024 2025 2026 2027 2028 Thereafter

Mortgage Debt Senior Notes Revolving Credit Facility

EFFICIENT BALANCE SHEET

STRATEGY & EXECUTION

Debt Maturity Schedule ($mm)(1)(2)

Continued Balance Sheet Execution Successfully Addressed Near-Term Maturities

1. Excludes the effect of discounts and deferred financing costs, net. Current balances as of September 30, 2024 are shown in the year the debt matures.

2. Assumes GNL exercises its two 6-month extension options on its Revolving Credit Facility.

0.0% 10.5% 2.1% 45.2% 20.7% 21.4%

% of Total Debt Outstanding

Weighted Average Debt Maturity: 3.2 years

▪ Addressed 100% of the outstanding debt with scheduled maturities in

2024 through dispositions and/or refinancing onto the Revolving

Credit Facility

▪ Proactively managing the 2025 debt balance, reducing it by $178

million thus far in 2024 and anticipate further reductions if GNL

completes dispositions currently in the pipeline

2024 Debt Maturity

Balance: 12/31/2023

2024 Debt Maturity

Balance: 3/31/2024

GNL has no debt maturing

through July 2025

$405 Million

$284 Million

$0

2024 Debt Maturity

Balance: 9/30/2024

$0

Q1’24 Net

Debt Balance

Q4’23 Net

Debt Balance

Q2’24 Net

Debt Balance

Q3’24 Net

Debt Balance

Decreased Net Debt by

$445 million since Q4’23 |

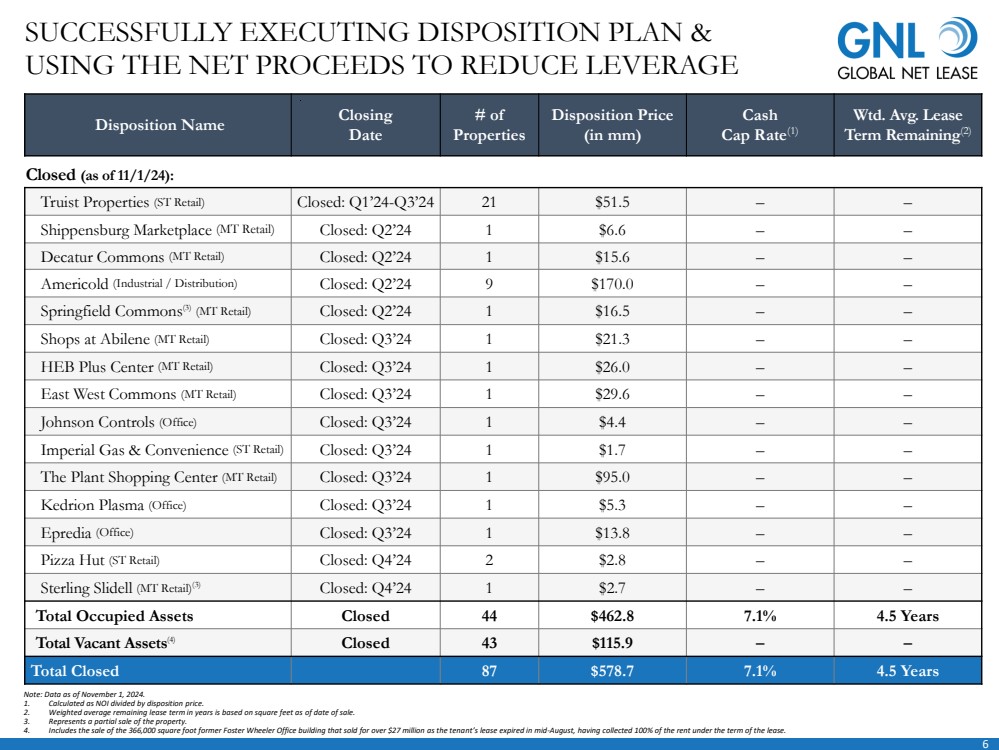

| 6

SUCCESSFULLY EXECUTING DISPOSITION PLAN &

USING THE NET PROCEEDS TO REDUCE LEVERAGE

Disposition Name Closing

Date

# of

Properties

Disposition Price

(in mm)

Cash

Cap Rate(1)

Wtd. Avg. Lease

Term Remaining(2)

Closed (as of 11/1/24):

Truist Properties (ST Retail) Closed: Q1’24-Q3’24 21 $51.5 – –

Shippensburg Marketplace (MT Retail) Closed: Q2’24 1 $6.6 – –

Decatur Commons (MT Retail) Closed: Q2’24 1 $15.6 – –

Americold (Industrial / Distribution) Closed: Q2’24 9 $170.0 – –

Springfield Commons(3) (MT Retail) Closed: Q2’24 1 $16.5 – –

Shops at Abilene (MT Retail) Closed: Q3’24 1 $21.3 – –

HEB Plus Center (MT Retail) Closed: Q3’24 1 $26.0 – –

East West Commons (MT Retail) Closed: Q3’24 1 $29.6 – –

Johnson Controls (Office) Closed: Q3’24 1 $4.4 – –

Imperial Gas & Convenience (ST Retail) Closed: Q3’24 1 $1.7 – –

The Plant Shopping Center (MT Retail) Closed: Q3’24 1 $95.0 – –

Kedrion Plasma (Office) Closed: Q3’24 1 $5.3 – –

Epredia (Office) Closed: Q3’24 1 $13.8 – –

Pizza Hut (ST Retail) Closed: Q4’24 2 $2.8 – –

Sterling Slidell (MT Retail)(3) Closed: Q4’24 1 $2.7 – –

Total Occupied Assets Closed 44 $462.8 7.1% 4.5 Years

Total Vacant Assets(4) Closed 43 $115.9 – –

Total Closed 87 $578.7 7.1% 4.5 Years

Note: Data as of November 1, 2024.

1. Calculated as NOI divided by disposition price.

2. Weighted average remaining lease term in years is based on square feet as of date of sale.

3. Represents a partial sale of the property.

4. Includes the sale of the 366,000 square foot former Foster Wheeler Office building that sold for over $27 million as the tenant’s lease expired in mid-August, having collected 100% of the rent under the term of the lease. |

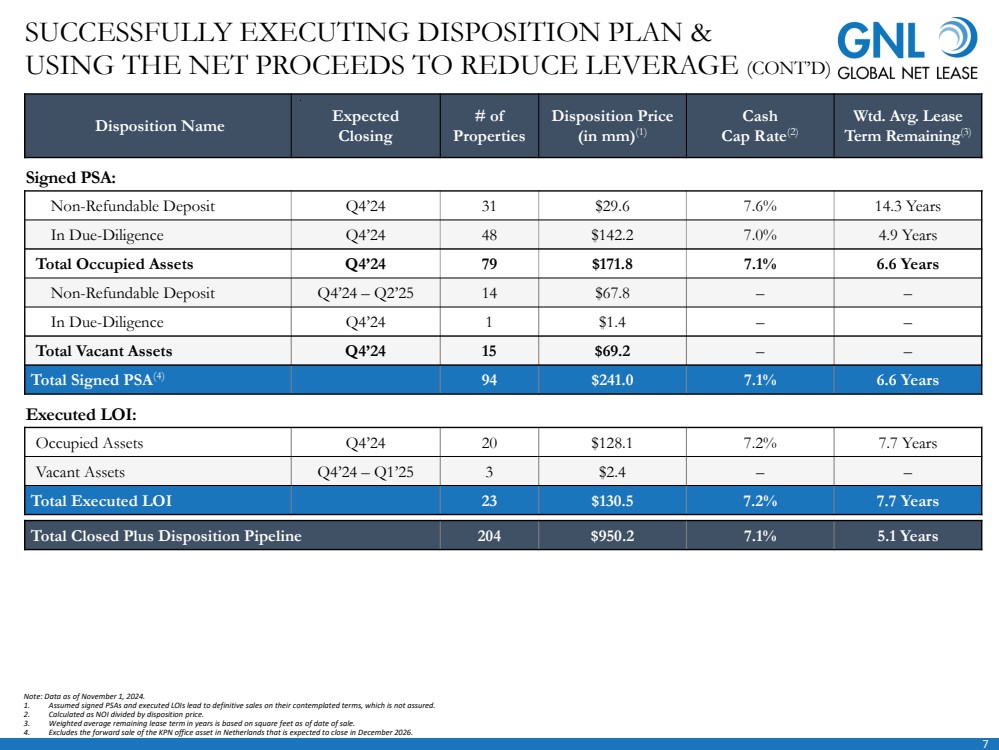

| 7

SUCCESSFULLY EXECUTING DISPOSITION PLAN &

USING THE NET PROCEEDS TO REDUCE LEVERAGE (CONT’D)

Disposition Name Expected

Closing

# of

Properties

Disposition Price

(in mm)(1)

Cash

Cap Rate(2)

Wtd. Avg. Lease

Term Remaining(3)

Signed PSA:

Non-Refundable Deposit Q4’24 31 $29.6 7.6% 14.3 Years

In Due-Diligence Q4’24 48 $142.2 7.0% 4.9 Years

Total Occupied Assets Q4’24 79 $171.8 7.1% 6.6 Years

Non-Refundable Deposit Q4’24 – Q2’25 14 $67.8 – –

In Due-Diligence Q4’24 1 $1.4 – –

Total Vacant Assets Q4’24 15 $69.2 – –

Total Signed PSA(4) 94 $241.0 7.1% 6.6 Years

Executed LOI:

Occupied Assets Q4’24 20 $128.1 7.2% 7.7 Years

Vacant Assets Q4’24 – Q1’25 3 $2.4 – –

Total Executed LOI 23 $130.5 7.2% 7.7 Years

Total Closed Plus Disposition Pipeline 204 $950.2 7.1% 5.1 Years

Note: Data as of November 1, 2024.

1. Assumed signed PSAs and executed LOIs lead to definitive sales on their contemplated terms, which is not assured.

2. Calculated as NOI divided by disposition price.

3. Weighted average remaining lease term in years is based on square feet as of date of sale.

4. Excludes the forward sale of the KPN office asset in Netherlands that is expected to close in December 2026. |

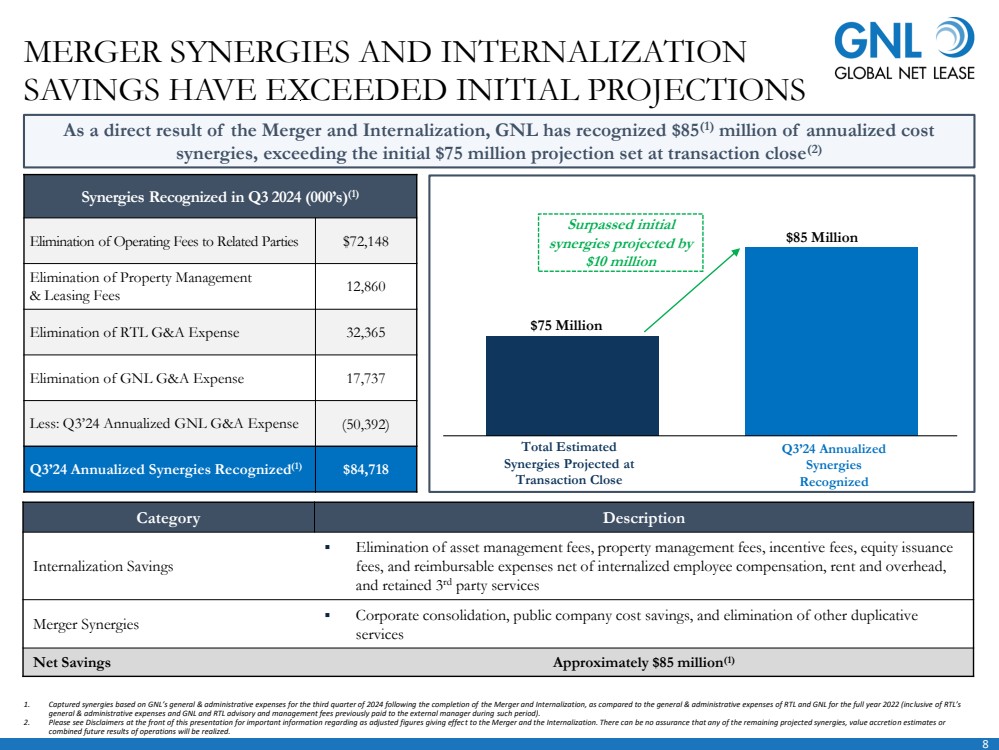

| 8

Category Description

Internalization Savings

▪ Elimination of asset management fees, property management fees, incentive fees, equity issuance

fees, and reimbursable expenses net of internalized employee compensation, rent and overhead,

and retained 3rd party services

Merger Synergies ▪ Corporate consolidation, public company cost savings, and elimination of other duplicative

services

Net Savings Approximately $85 million(1)

1. Captured synergies based on GNL’s general & administrative expenses for the third quarter of 2024 following the completion of the Merger and Internalization, as compared to the general & administrative expenses of RTL and GNL for the full year 2022 (inclusive of RTL’s

general & administrative expenses and GNL and RTL advisory and management fees previously paid to the external manager during such period).

2. Please see Disclaimers at the front of this presentation for important information regarding as adjusted figures giving effect to the Merger and the Internalization. There can be no assurance that any of the remaining projected synergies, value accretion estimates or

combined future results of operations will be realized.

MERGER SYNERGIES AND INTERNALIZATION

SAVINGS HAVE EXCEEDED INITIAL PROJECTIONS

Synergies Recognized in Q3 2024 (000’s)(1)

Elimination of Operating Fees to Related Parties $72,148

Elimination of Property Management

& Leasing Fees 12,860

Elimination of RTL G&A Expense 32,365

Elimination of GNL G&A Expense 17,737

Less: Q3’24 Annualized GNL G&A Expense (50,392)

Q3’24 Annualized Synergies Recognized(1) $84,718

As a direct result of the Merger and Internalization, GNL has recognized $85(1) million of annualized cost

synergies, exceeding the initial $75 million projection set at transaction close(2)

Total Estimated

Synergies Projected at

Transaction Close

Q3’24 Annualized

Synergies

Recognized

$75 Million

$85 Million

Surpassed initial

synergies projected by

$10 million |

| 9

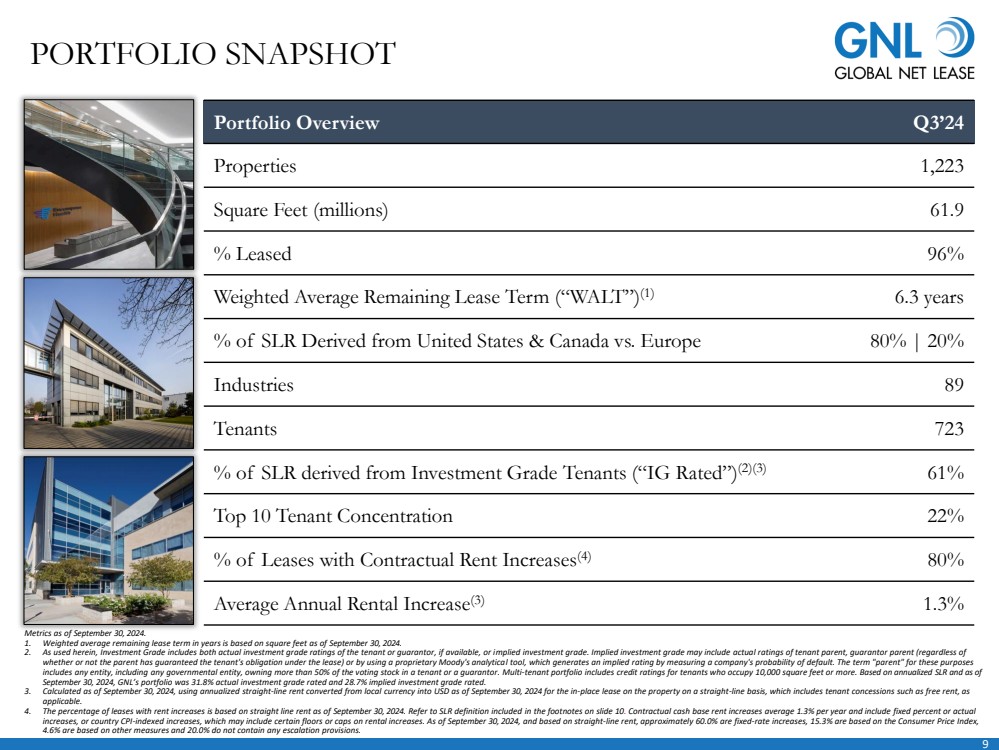

Portfolio Overview Q3’24

Properties 1,223

Square Feet (millions) 61.9

% Leased 96%

Weighted Average Remaining Lease Term (“WALT”)(1) 6.3 years

% of SLR Derived from United States & Canada vs. Europe 80% | 20%

Industries 89

Tenants 723

% of SLR derived from Investment Grade Tenants (“IG Rated”)(2)(3) 61%

Top 10 Tenant Concentration 22%

% of Leases with Contractual Rent Increases(4) 80%

Average Annual Rental Increase(3) 1.3%

Metrics as of September 30, 2024.

1. Weighted average remaining lease term in years is based on square feet as of September 30, 2024.

2. As used herein, Investment Grade includes both actual investment grade ratings of the tenant or guarantor, if available, or implied investment grade. Implied investment grade may include actual ratings of tenant parent, guarantor parent (regardless of

whether or not the parent has guaranteed the tenant's obligation under the lease) or by using a proprietary Moody's analytical tool, which generates an implied rating by measuring a company's probability of default. The term "parent" for these purposes

includes any entity, including any governmental entity, owning more than 50% of the voting stock in a tenant or a guarantor. Multi-tenant portfolio includes credit ratings for tenants who occupy 10,000 square feet or more. Based on annualized SLR and as of

September 30, 2024, GNL’s portfolio was 31.8% actual investment grade rated and 28.7% implied investment grade rated.

3. Calculated as of September 30, 2024, using annualized straight-line rent converted from local currency into USD as of September 30, 2024 for the in-place lease on the property on a straight-line basis, which includes tenant concessions such as free rent, as

applicable.

4. The percentage of leases with rent increases is based on straight line rent as of September 30, 2024. Refer to SLR definition included in the footnotes on slide 10. Contractual cash base rent increases average 1.3% per year and include fixed percent or actual

increases, or country CPI-indexed increases, which may include certain floors or caps on rental increases. As of September 30, 2024, and based on straight-line rent, approximately 60.0% are fixed-rate increases, 15.3% are based on the Consumer Price Index,

4.6% are based on other measures and 20.0% do not contain any escalation provisions.

PORTFOLIO SNAPSHOT |

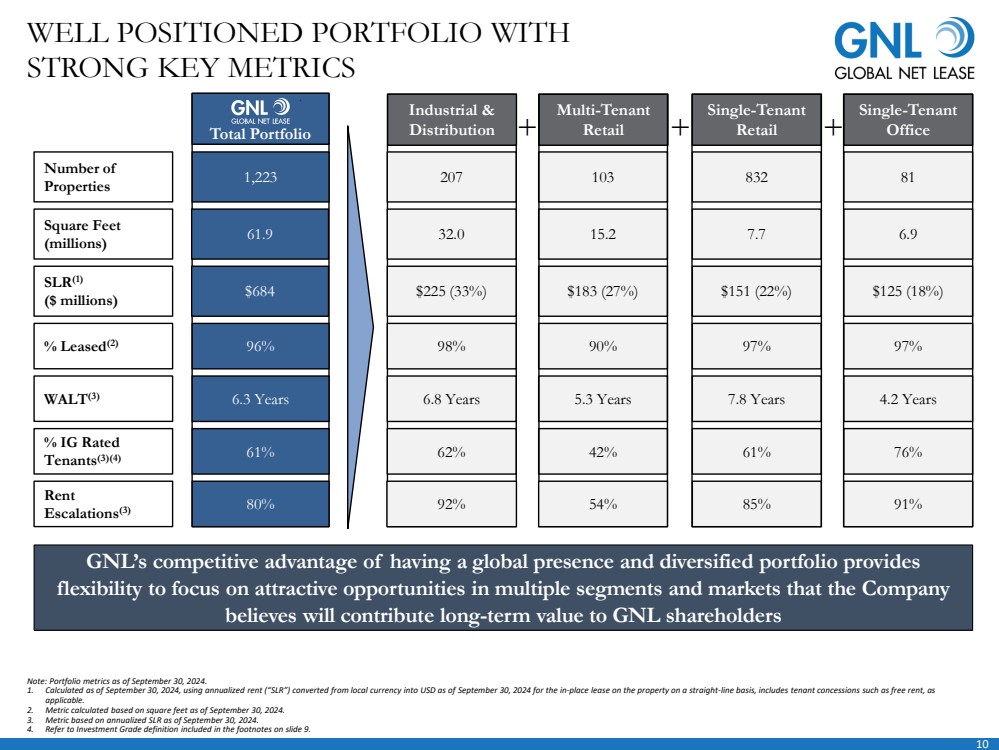

| 10

Industrial

WELL POSITIONED PORTFOLIO WITH

STRONG KEY METRICS

Note: Portfolio metrics as of September 30, 2024.

1. Calculated as of September 30, 2024, using annualized rent (“SLR”) converted from local currency into USD as of September 30, 2024 for the in-place lease on the property on a straight-line basis, includes tenant concessions such as free rent, as

applicable.

2. Metric calculated based on square feet as of September 30, 2024.

3. Metric based on annualized SLR as of September 30, 2024.

4. Refer to Investment Grade definition included in the footnotes on slide 9.

+

Number of

Properties

Square Feet

(millions)

SLR(1)

($ millions)

% Leased(2)

WALT(3)

% IG Rated

Tenants(3)(4)

+ +

Industrial &

Distribution

207

32.0

$225 (33%)

98%

6.8 Years

62%

Multi-Tenant

Retail

103

15.2

$183 (27%)

90%

5.3 Years

42%

Single-Tenant

Retail

832

7.7

$151 (22%)

97%

7.8 Years

61%

Single-Tenant

Office

81

6.9

$125 (18%)

97%

4.2 Years

76%

Total Portfolio

1,223

61.9

$684

96%

6.3 Years

61%

Rent

Escalations(3) 80% 92% 54% 85% 91%

GNL’s competitive advantage of having a global presence and diversified portfolio provides

flexibility to focus on attractive opportunities in multiple segments and markets that the Company

believes will contribute long-term value to GNL shareholders |

| 11

1. Metric based on annualized SLR as of September 30, 2024. Refer to SLR definition included in the footnotes on slide 10.

2. Based on Annualized Straight-Line Rent. Ratings information as of October 24, 2024. Refer to Investment Grade Rating definition included in the footnotes on slide 9.

Top ten tenants represent 22% of SLR with no single tenant accounting for more than 3.3%

Tenant Credit Rating Country Property Type % of SLR(1)

Actual: Baa2 U.S. / Canada Industrial & Distribution 3.3%

Implied: Baa1 U.S. Single-Tenant Retail 3.3%

Actual: CCC+ U.K. Industrial & Distribution 3.0%

Actual: Baa3 U.S. Single-Tenant Retail 2.2%

Actual: Baa2 U.S. / Italy Industrial & Distribution 2.1%

Actual: A2 U.S. Industrial & Distribution;

Multi-Tenant Retail 2.0%

Actual: Aaa U.S. Single-Tenant Office 1.7%

Actual: Aa3 Netherlands Single-Tenant Office 1.6%

Implied: Baa1 U.S. Industrial / Distribution 1.5%

Actual: Baa2 U.S. Single-Tenant Retail 1.4%

Top 10 Tenants 86.4% IG Rated(2) 22.1%

Top Ten Tenants

HIGH-QUALITY INVESTMENT-GRADE TENANTS |

| 12

MIDWEST

NC

FL

GA AL MS

LA

TX

NM AZ

CA

NV

UT

OR

WA

ID

MT

WY

CO

ND

SD

NE

KS

OK

AR

MO

IA

MN WI

MI

IL IN

OH

KY

TN

SC

NC

WV VA

PA

NY

VT NH

ME

MA

NJ CT

MD

DE

DC

RI

NB

PACIFIC

SOUTHWEST

SOUTHWEST

MID-ATLANTIC

NEW

PACIFIC BRUNSWICK

NORTHWEST

SOUTH

EAST

AK

NORTHEAST

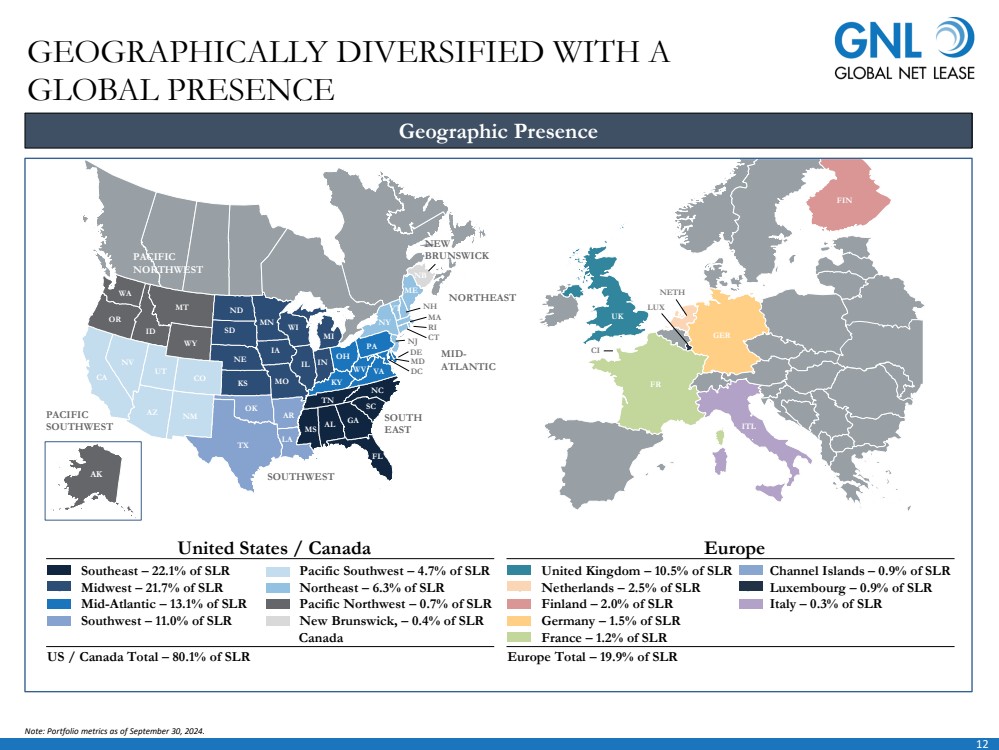

GEOGRAPHICALLY DIVERSIFIED WITH A

GLOBAL PRESENCE

Geographic Presence

Note: Portfolio metrics as of September 30, 2024.

FR

UK

ITL

GER

LUX

NETH

FIN

CI

United States / Canada

US / Canada Total – 80.1% of SLR

⚫ Southeast – 22.1% of SLR

⚫ Midwest – 21.7% of SLR

⚫ Mid-Atlantic – 13.1% of SLR

⚫ Southwest – 11.0% of SLR

⚫ Pacific Southwest – 4.7% of SLR

⚫ Northeast – 6.3% of SLR

⚫ Pacific Northwest – 0.7% of SLR

⚫ New Brunswick, – 0.4% of SLR

Canada

Europe

Europe Total – 19.9% of SLR

⚫ United Kingdom – 10.5% of SLR

⚫ Netherlands – 2.5% of SLR

⚫ Finland – 2.0% of SLR

⚫ Germany – 1.5% of SLR

⚫ France – 1.2% of SLR

⚫ Channel Islands – 0.9% of SLR

⚫ Luxembourg – 0.9% of SLR

⚫ Italy – 0.3% of SLR

|

| 13

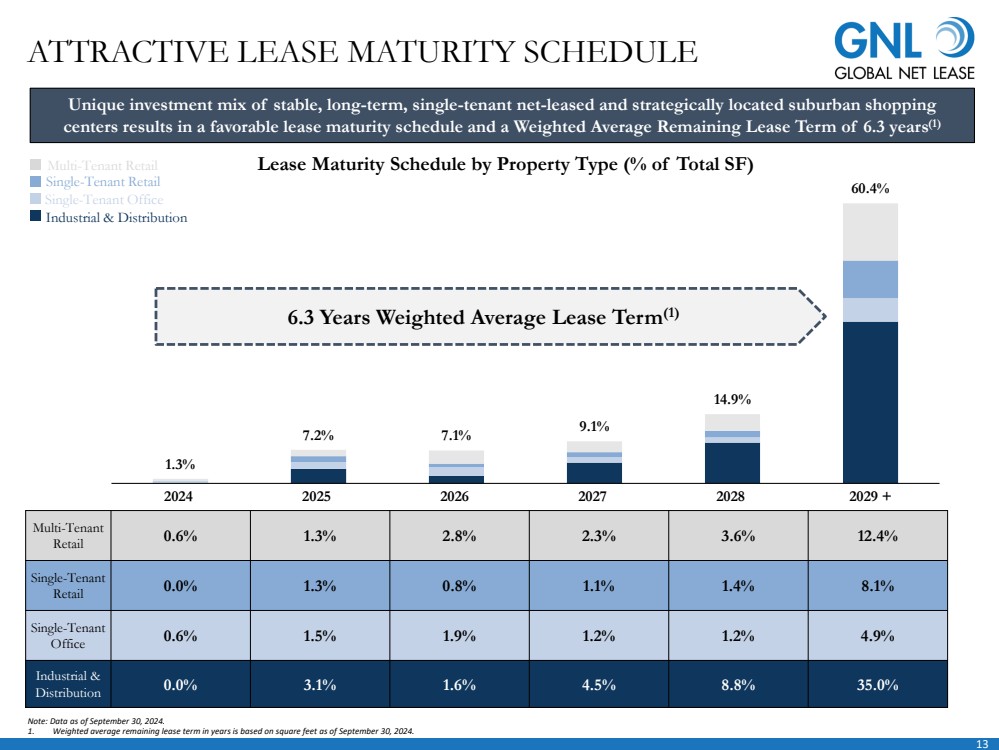

1.3%

7.2% 7.1% 9.1%

14.9%

60.4%

2024 2025 2026 2027 2028 2029 +

Lease Maturity Schedule by Property Type (% of Total SF)

ATTRACTIVE LEASE MATURITY SCHEDULE

Unique investment mix of stable, long-term, single-tenant net-leased and strategically located suburban shopping

centers results in a favorable lease maturity schedule and a Weighted Average Remaining Lease Term of 6.3 years(1)

Note: Data as of September 30, 2024.

1. Weighted average remaining lease term in years is based on square feet as of September 30, 2024.

Multi-Tenant

Retail 0.6% 1.3% 2.8% 2.3% 3.6% 12.4%

Single-Tenant

Retail 0.0% 1.3% 0.8% 1.1% 1.4% 8.1%

Single-Tenant

Office 0.6% 1.5% 1.9% 1.2% 1.2% 4.9%

Industrial &

Distribution 0.0% 3.1% 1.6% 4.5% 8.8% 35.0%

6.3 Years Weighted Average Lease Term(1)

Multi-Tenant Retail

Single-Tenant Retail

Single-Tenant Office

Industrial & Distribution |

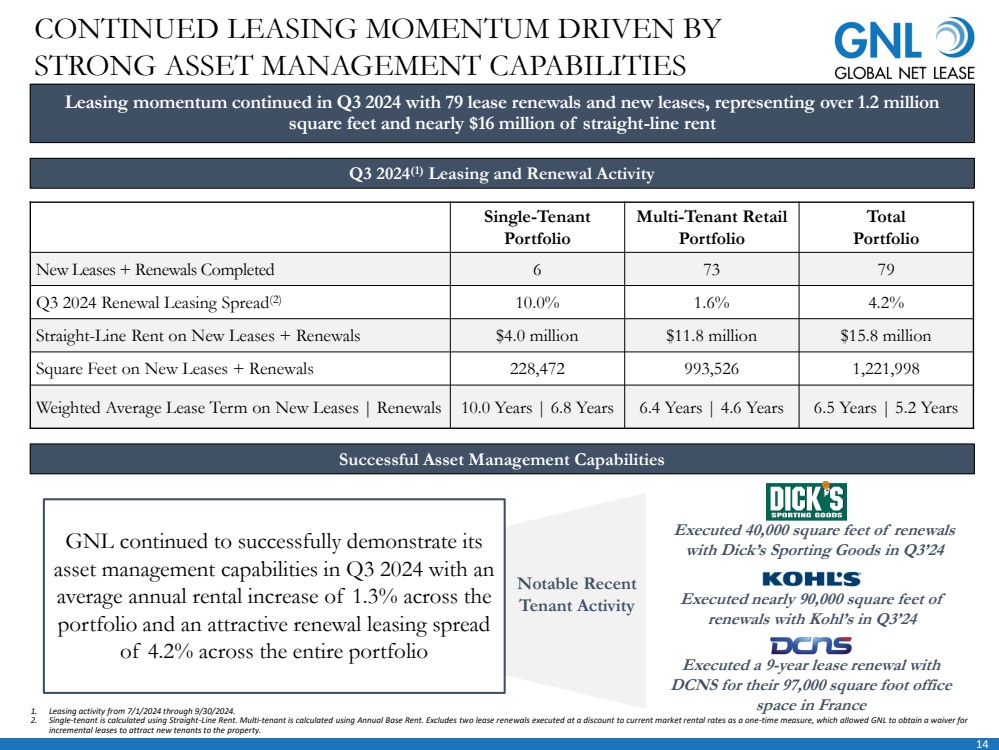

| 14

Leasing momentum continued in Q3 2024 with 79 lease renewals and new leases, representing over 1.2 million

square feet and nearly $16 million of straight-line rent

Q3 2024(1) Leasing and Renewal Activity

Single-Tenant

Portfolio

Multi-Tenant Retail

Portfolio

Total

Portfolio

New Leases + Renewals Completed 6 73 79

Q3 2024 Renewal Leasing Spread(2) 10.0% 1.6% 4.2%

Straight-Line Rent on New Leases + Renewals $4.0 million $11.8 million $15.8 million

Square Feet on New Leases + Renewals 228,472 993,526 1,221,998

Weighted Average Lease Term on New Leases | Renewals 10.0 Years | 6.8 Years 6.4 Years | 4.6 Years 6.5 Years | 5.2 Years

1. Leasing activity from 7/1/2024 through 9/30/2024.

2. Single-tenant is calculated using Straight-Line Rent. Multi-tenant is calculated using Annual Base Rent. Excludes two lease renewals executed at a discount to current market rental rates as a one-time measure, which allowed GNL to obtain a waiver for

incremental leases to attract new tenants to the property.

CONTINUED LEASING MOMENTUM DRIVEN BY

STRONG ASSET MANAGEMENT CAPABILITIES

Successful Asset Management Capabilities

GNL continued to successfully demonstrate its

asset management capabilities in Q3 2024 with an

average annual rental increase of 1.3% across the

portfolio and an attractive renewal leasing spread

of 4.2% across the entire portfolio

Notable Recent

Tenant Activity Executed nearly 90,000 square feet of

renewals with Kohl’s in Q3’24

Executed a 9-year lease renewal with

DCNS for their 97,000 square foot office

space in France

Executed 40,000 square feet of renewals

with Dick’s Sporting Goods in Q3’24 |

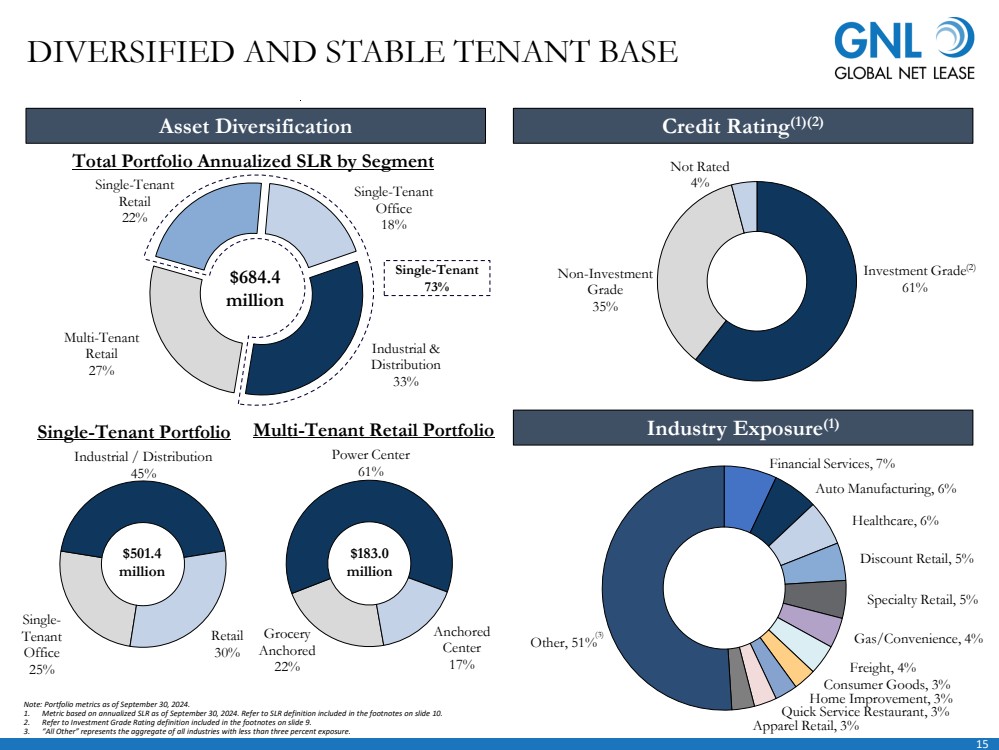

| 15

Industrial &

Distribution

33%

Multi-Tenant

Retail

27%

Single-Tenant

Retail

22%

Single-Tenant

Office

18%

Grocery

Anchored

22%

Power Center

61%

Anchored

Center

17%

Single-Tenant

Office

25%

Industrial / Distribution

45%

Retail

30%

$183.0

million

$684.4

million

Total Portfolio Annualized SLR by Segment

Industry Exposure(1)

Credit Rating Asset Diversification (1)(2)

Note: Portfolio metrics as of September 30, 2024.

1. Metric based on annualized SLR as of September 30, 2024. Refer to SLR definition included in the footnotes on slide 10.

2. Refer to Investment Grade Rating definition included in the footnotes on slide 9.

3. “All Other” represents the aggregate of all industries with less than three percent exposure.

DIVERSIFIED AND STABLE TENANT BASE

Single-Tenant Portfolio Multi-Tenant Retail Portfolio

$501.4

million

Single-Tenant

73%

(2)

(3)

Investment Grade

61%

Non-Investment

Grade

35%

Not Rated

4%

Financial Services, 7%

Auto Manufacturing, 6%

Healthcare, 6%

Discount Retail, 5%

Specialty Retail, 5%

Gas/Convenience, 4%

Freight, 4%

Consumer Goods, 3%

Home Improvement, 3%

Quick Service Restaurant, 3%

Apparel Retail, 3%

Other, 51% |

| 16

0.0%

3.1% 1.6%

4.5%

8.8%

35.0%

2024 2025 2026 2027 2028 2029 +

United States

72%

Europe

10%

United Kingdom

16%

Canada

1%

Tenant Credit Rating Country % of SLR

Actual: Baa2 U.S. / Canada 3.3%

Actual: CCC+ U.K. 3.0%

Actual: Baa2 U.S. / Italy 2.1%

Implied: Baa1 U.S. 1.5%

Actual: Baa2 U.S. 1.4%

Top 5 Tenants 73.5% IG Rated(2)(3) 11.3%

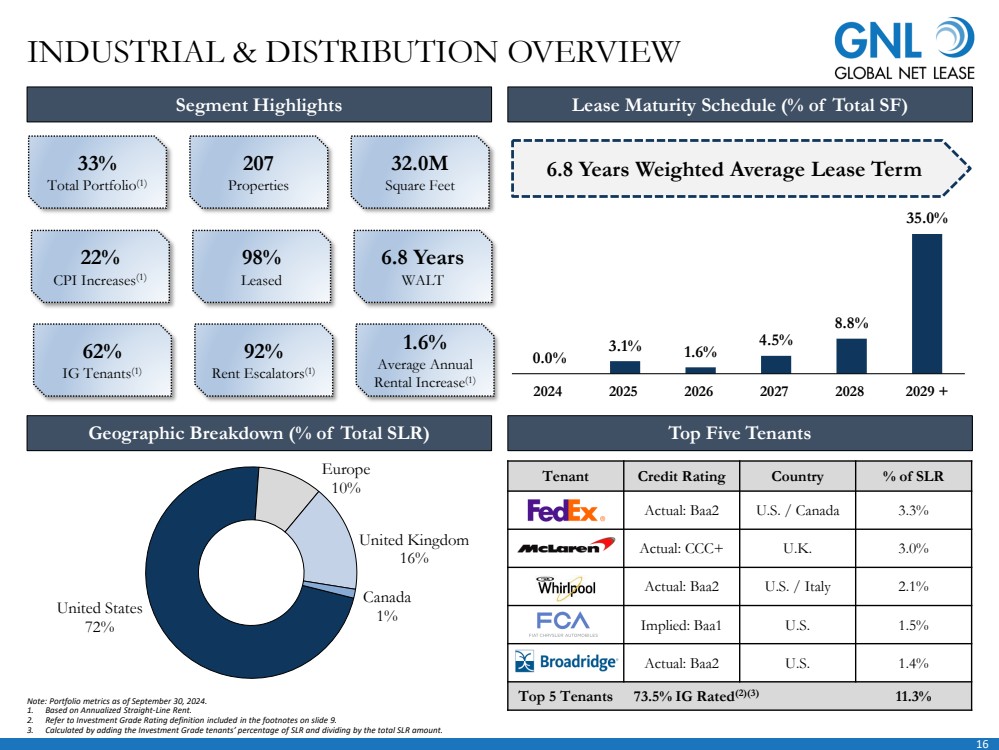

Segment Highlights Lease Maturity Schedule (% of Total SF)

Geographic Breakdown (% of Total SLR) Top Five Tenants

33%

Total Portfolio(1)

207

Properties

32.0M

Square Feet

22%

CPI Increases(1)

98%

Leased

6.8 Years

WALT

62%

IG Tenants(1)

92%

Rent Escalators(1)

1.6%

Average Annual

Rental Increase(1)

Note: Portfolio metrics as of September 30, 2024.

1. Based on Annualized Straight-Line Rent.

2. Refer to Investment Grade Rating definition included in the footnotes on slide 9.

3. Calculated by adding the Investment Grade tenants’ percentage of SLR and dividing by the total SLR amount.

INDUSTRIAL & DISTRIBUTION OVERVIEW

6.8 Years Weighted Average Lease Term |

| 17

88.8%

90.3%

Q2'24 Occupancy Q3'24 Occupancy

0.6% 1.3%

2.8% 2.3%

3.6%

12.4%

2024 2025 2026 2027 2028 2029 +

Multi-Tenant Leasing Is Expected To Increase Occupancy to 92.9%

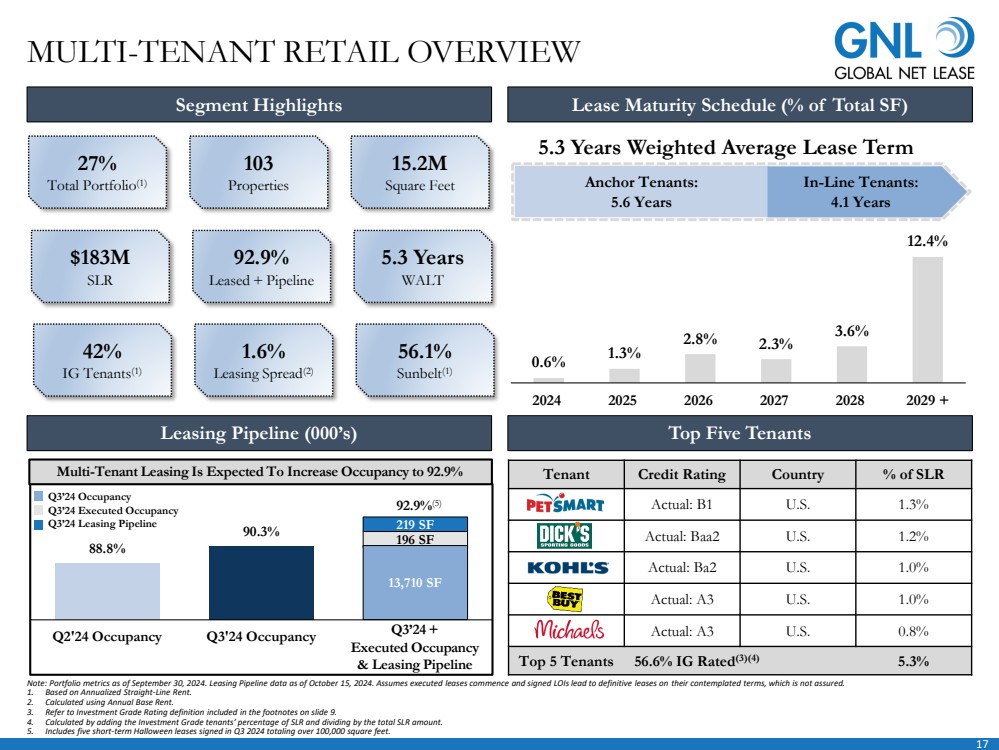

MULTI-TENANT RETAIL OVERVIEW

Tenant Credit Rating Country % of SLR

Actual: B1 U.S. 1.3%

Actual: Baa2 U.S. 1.2%

Actual: Ba2 U.S. 1.0%

Actual: A3 U.S. 1.0%

Actual: A3 U.S. 0.8%

Top 5 Tenants 56.6% IG Rated(3)(4) 5.3%

Segment Highlights Lease Maturity Schedule (% of Total SF)

Leasing Pipeline (000’s) Top Five Tenants

27%

Total Portfolio(1)

103

Properties

15.2M

Square Feet

$183M

SLR

92.9%

Leased + Pipeline

5.3 Years

WALT

42%

IG Tenants(1)

1.6%

Leasing Spread(2)

56.1%

Sunbelt(1)

Q3’24 Occupancy

Q3’24 Executed Occupancy

Q3’24 Leasing Pipeline

Note: Portfolio metrics as of September 30, 2024. Leasing Pipeline data as of October 15, 2024. Assumes executed leases commence and signed LOIs lead to definitive leases on their contemplated terms, which is not assured.

1. Based on Annualized Straight-Line Rent.

2. Calculated using Annual Base Rent.

3. Refer to Investment Grade Rating definition included in the footnotes on slide 9.

4. Calculated by adding the Investment Grade tenants’ percentage of SLR and dividing by the total SLR amount.

5. Includes five short-term Halloween leases signed in Q3 2024 totaling over 100,000 square feet.

5.3 Years Weighted Average Lease Term

Anchor Tenants:

5.6 Years

In-Line Tenants:

4.1 Years

196 SF

219 SF

Q3’24 +

Executed Occupancy

& Leasing Pipeline

92.9%(5)

13,710 SF |

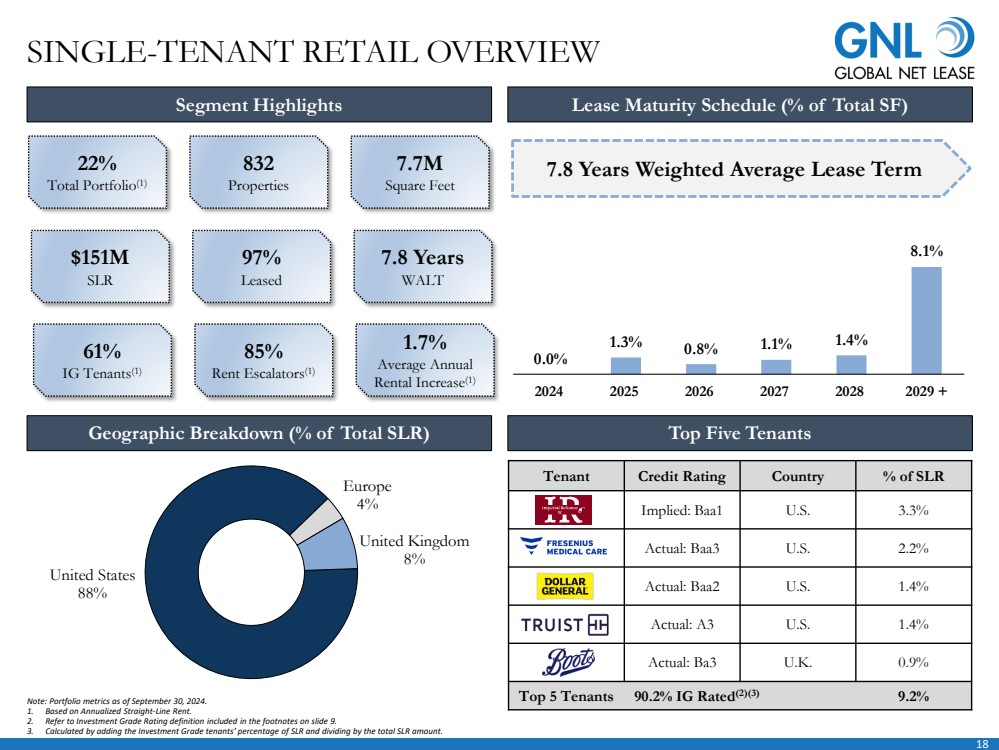

| 18

0.0%

1.3% 0.8% 1.1% 1.4%

8.1%

2024 2025 2026 2027 2028 2029 +

United States

88%

Europe

4%

United Kingdom

8%

SINGLE-TENANT RETAIL OVERVIEW

Tenant Credit Rating Country % of SLR

Implied: Baa1 U.S. 3.3%

Actual: Baa3 U.S. 2.2%

Actual: Baa2 U.S. 1.4%

Actual: A3 U.S. 1.4%

Actual: Ba3 U.K. 0.9%

Top 5 Tenants 90.2% IG Rated(2)(3) 9.2%

Segment Highlights Lease Maturity Schedule (% of Total SF)

Geographic Breakdown (% of Total SLR) Top Five Tenants

22%

Total Portfolio(1)

832

Properties

7.7M

Square Feet

$151M

SLR

97%

Leased

7.8 Years

WALT

61%

IG Tenants(1)

85%

Rent Escalators(1)

1.7%

Average Annual

Rental Increase(1)

Note: Portfolio metrics as of September 30, 2024.

1. Based on Annualized Straight-Line Rent.

2. Refer to Investment Grade Rating definition included in the footnotes on slide 9.

3. Calculated by adding the Investment Grade tenants’ percentage of SLR and dividing by the total SLR amount.

7.8 Years Weighted Average Lease Term |

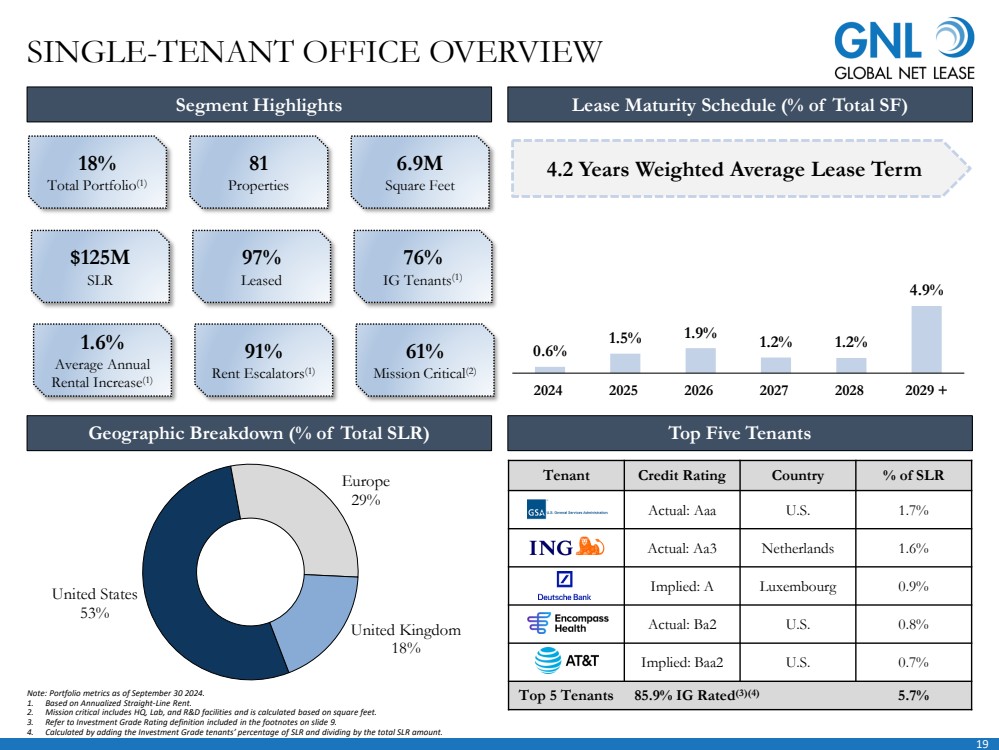

| 19

0.6%

1.5% 1.9% 1.2% 1.2%

4.9%

2024 2025 2026 2027 2028 2029 +

SINGLE-TENANT OFFICE OVERVIEW

Tenant Credit Rating Country % of SLR

Actual: Aaa U.S. 1.7%

Actual: Aa3 Netherlands 1.6%

Implied: A Luxembourg 0.9%

Actual: Ba2 U.S. 0.8%

Implied: Baa2 U.S. 0.7%

Top 5 Tenants 85.9% IG Rated(3)(4) 5.7%

Segment Highlights Lease Maturity Schedule (% of Total SF)

18%

Total Portfolio(1)

81

Properties

6.9M

Square Feet

$125M

SLR

97%

Leased

76%

IG Tenants(1)

1.6%

Average Annual

Rental Increase(1)

91%

Rent Escalators(1)

61%

Mission Critical(2)

Geographic Breakdown (% of Total SLR) Top Five Tenants

Note: Portfolio metrics as of September 30 2024.

1. Based on Annualized Straight-Line Rent.

2. Mission critical includes HQ, Lab, and R&D facilities and is calculated based on square feet.

3. Refer to Investment Grade Rating definition included in the footnotes on slide 9.

4. Calculated by adding the Investment Grade tenants’ percentage of SLR and dividing by the total SLR amount.

4.2 Years Weighted Average Lease Term

United States

53%

Europe

29%

United Kingdom

18% |

| 20

LEADERSHIP OVERVIEW

Management Board of Directors

Michael Weil, Director

Refer to “Management” section for Michael Weil’s biography

Michael Weil, Chief Executive Officer & President

Previously served as CEO of The Necessity Retail

REIT

Member of the Board of Directors of Global Net

Lease, Inc. since 2012

Served as President of the Board of Directors of the

Real Estate Investment Securities Association

Chris Masterson, Chief Financial Officer

Previously served as Chief Accounting Officer of

GNL

Past experience includes accounting positions with

Goldman Sachs and KPMG

Sue Perrotty, Non-Executive Chairperson of the Board of Directors

Currently serves as President and Chief Executive Officer of AFM Financial

Services and Tower Health

Edward Rendell, Independent Director

Previously served as the 45th Governor of the Commonwealth of Pennsylvania and

as the Mayor of Philadelphia, and previously served as a member of the board of

directors of The Necessity Retail REIT

Lisa Kabnick, Independent Director

Retired Partner at Troutman Pepper Hamilton Sanders LLP, and previously served

as a member of the board of directors of The Necessity Retail REIT

Therese Antone, Independent Director

Currently serves as the Chancellor of Salve Regina University since her appointment

in 2009

Leslie Michelson, Independent Director

Currently serves as lead independent director of Franklin BSP Franklin Lending

Corporation, and previously served as a member of the board of directors of The

Necessity Retail REIT

Stanley Perla, Independent Director

Previously served as a member of the board of directors and the chair of the audit

committee of Madison Harbor Balanced Strategies, Inc, and previously served as a

member of the board of directors of The Necessity Retail REIT

Independent Directors

Inside Directors

Jesse Galloway, Executive Vice President & General Counsel

Joined GNL in September 2023

25 years of legal experience representing large real

estate companies and financial institutions, including

10 years as General Counsel and 15 years in private

practice

Jason Slear, Executive Vice President

Responsible for sourcing, negotiating, and closing

GNL’s real estate acquisitions and dispositions

Oversaw the acquisition of over $3.5 billion of real

estate assets and the lease-up of over 10 million

square feet during professional career

Ori Kravel, Senior Vice President

Responsible for corporate development and

business strategy

Executed over $12 billion of capital market

transactions and over $25 billion of M&A

transactions

Rob Kauffman, Independent Director

Co-founder of Fortress Investment Group and previously worked as a Managing

Director at UBS, a Principal at BlackRock Financial and at Lehman Brothers

Michael J.U. Monahan, Independent Director

Currently serves as a CBRE Vice Chair and previously served as a Senior Director at

Jones Lang Wootton and a Vice President at Cushman & Wakefield |

| 21

APPENDIX: FINANCIAL DEFINITIONS

Non-GAAP Financial Measures

This section discusses non-GAAP financial measures we use to evaluate our performance, including Funds from Operations (“FFO”), Core Funds from Operations (“Core FFO”),

Adjusted Funds from Operations (“AFFO”), Adjusted Earnings before Interest, Taxes, Depreciation and Amortization (“Adjusted EBITDA”), Net Operating Income (“NOI”), Cash

Net Operating Income (“Cash NOI”) and Cash Paid for Interest. While NOI is a property-level measure, AFFO is based on total Company performance and therefore reflects the

impact of other items not specifically associated with NOI such as, interest expense, general and administrative expenses and operating fees to related parties. Additionally, NOI as

defined herein, does not reflect an adjustment for straight-line rent but AFFO does include this adjustment. A description of these non-GAAP measures and reconciliations to the most

directly comparable GAAP measure, which is net income, is provided below.

Caution on Use of Non-GAAP Measures

FFO, Core FFO, AFFO, Adjusted EBITDA, NOI, Cash NOI and Cash Paid for Interest should not be construed to be more relevant or accurate than the current GAAP methodology

in calculating net income or in its applicability in evaluating our operating performance. The method utilized to evaluate the value and performance of real estate under GAAP should be

construed as a more relevant measure of operational performance and considered more prominently than the non-GAAP measures.

Other REITs may not define FFO in accordance with the current National Association of Real Estate Investment Trusts (“NAREIT”) definition (as we do), or may interpret the

current NAREIT definition differently than we do, or may calculate Core FFO or AFFO differently than we do. Consequently, our presentation of FFO, Core FFO and AFFO may not

be comparable to other similarly-titled measures presented by other REITs.

We consider FFO, Core FFO and AFFO useful indicators of our performance. Because FFO, Core FFO and AFFO calculations exclude such factors as depreciation and amortization

of real estate assets and gain or loss from sales of operating real estate assets (which can vary among owners of identical assets in similar conditions based on historical cost accounting

and useful-life estimates), FFO, Core FFO and AFFO presentations facilitate comparisons of operating performance between periods and between other REITs in our peer group.

Funds from Operations, Core Funds from Operations and Adjusted Funds from Operations

Funds From Operations

Due to certain unique operating characteristics of real estate companies, as discussed below, NAREIT, an industry trade group, has promulgated a measure known as FFO, which we

believe to be an appropriate supplemental measure to reflect the operating performance of a REIT. FFO is not equivalent to net income or loss as determined under GAAP.

We calculate FFO, a non-GAAP measure, consistent with the standards established over time by the Board of Governors of NAREIT, as restated in a White Paper approved by the

Board of Governors of NAREIT effective in December 2018 (the “White Paper”). The White Paper defines FFO as net income or loss computed in accordance with GAAP, excluding

depreciation and amortization related to real estate, gain and loss from the sale of certain real estate assets, gain and loss from change in control and impairment write-downs of certain

real estate assets and investments in entities when the impairment is directly attributable to decreases in the value of depreciable real estate held by the entity. Adjustments for

unconsolidated partnerships and joint ventures are calculated to exclude the proportionate share of the non-controlling interest to arrive at FFO, Core FFO, AFFO and NOI

attributable to stockholders, as applicable. Our FFO calculation complies with NAREIT’s definition. |

| 22

The historical accounting convention used for real estate assets requires straight-line depreciation of buildings and improvements, and straight-line amortization of intangibles, which

implies that the value of a real estate asset diminishes predictably over time. We believe that, because real estate values historically rise and fall with market conditions, including

inflation, interest rates, unemployment and consumer spending, presentations of operating results for a REIT using historical accounting for depreciation and certain other items may be

less informative. Historical accounting for real estate involves the use of GAAP. Any other method of accounting for real estate such as the fair value method cannot be construed to be

any more accurate or relevant than the comparable methodologies of real estate valuation found in GAAP. Nevertheless, we believe that the use of FFO, which excludes the impact of

real estate related depreciation and amortization, among other things, provides a more complete understanding of our performance to investors and to management, and, when

compared year over year, reflects the impact on our operations from trends in occupancy rates, rental rates, operating costs, general and administrative expenses, and interest costs,

which may not be immediately apparent from net income.

Funds from Operations, Core Funds from Operations and Adjusted Funds from Operations (Cont’d)

Core Funds From Operations

In calculating Core FFO, we start with FFO, then we exclude certain non-core items such as merger, transaction and other costs, as well as certain other costs that are considered to be

non-core, such as debt extinguishment costs. The purchase of properties, and the corresponding expenses associated with that process, is a key operational feature of our core business

plan to generate operational income and cash flows in order to make dividend payments to stockholders. In evaluating investments in real estate, we differentiate the costs to acquire the

investment from the subsequent operations of the investment. We also add back non-cash write-offs of deferred financing costs and prepayment penalties incurred with the early

extinguishment of debt which are included in net income but are considered financing cash flows when paid in the statement of cash flows. We consider these write-offs and

prepayment penalties to be capital transactions and not indicative of operations. By excluding expensed acquisition, transaction and other costs as well as non-core costs, we believe

Core FFO provides useful supplemental information that is comparable for each type of real estate investment and is consistent with management’s analysis of the investing and

operating performance of our properties.

Adjusted Funds From Operations

In calculating AFFO, we start with Core FFO, then we exclude certain income or expense items from AFFO that we consider more reflective of investing activities, other non-cash

income and expense items and the income and expense effects of other activities or items, including items that were paid in cash that are not a fundamental attribute of our business

plan or were one time or non-recurring items. These items include early extinguishment of debt and other items excluded in Core FFO as well as unrealized gain and loss, which may

not ultimately be realized, such as gain or loss on derivative instruments, gain or loss on foreign currency transactions, and gain or loss on investments. In addition, by excluding non-cash income and expense items such as amortization of above-market and below-market leases intangibles, amortization of deferred financing costs, straight-line rent and equity-based

compensation from AFFO, we believe we provide useful information regarding income and expense items which have a direct impact on our ongoing operating performance. We also

exclude revenue attributable to the reimbursement by third parties of financing costs that we originally incurred because these revenues are not, in our view, related to operating

performance. We also include the realized gain or loss on foreign currency exchange contracts for AFFO as such items are part of our ongoing operations and affect our current

operating performance.

APPENDIX: FINANCIAL DEFINITIONS |

| 23

Funds from Operations, Core Funds from Operations and Adjusted Funds from Operations (Cont’d)

Adjusted Funds From Operations (cont’d)

In calculating AFFO, we also exclude certain expenses which under GAAP are characterized as operating expenses in determining operating net income. All paid and accrued

acquisition, transaction and other costs (including prepayment penalties for debt extinguishments and merger related expenses) and certain other expenses, including expenses incurred

for the 2023 proxy contest and related Blackwells/Related Parties litigation, expenses related to our European tax restructuring and transition costs related to the Mergers, negatively

impact our operating performance during the period in which expenses are incurred or properties are acquired and will also have negative effects on returns to investors, but are

excluded by us as we believe they are not reflective of our on-going performance. Further, under GAAP, certain contemplated non-cash fair value and other non-cash adjustments are

considered operating non-cash adjustments to net income. In addition, as discussed above, we view gain and loss from fair value adjustments as items which are unrealized and may not

ultimately be realized and not reflective of ongoing operations and are therefore typically adjusted for when assessing operating performance. Excluding income and expense items

detailed above from our calculation of AFFO provides information consistent with management’s analysis of our operating performance. Additionally, fair value adjustments, which are

based on the impact of current market fluctuations and underlying assessments of general market conditions, but can also result from operational factors such as rental and occupancy

rates, may not be directly related or attributable to our current operating performance. By excluding such changes that may reflect anticipated and unrealized gain or loss, we believe

AFFO provides useful supplemental information. By providing AFFO, we believe we are presenting useful information that can be used to, among other things, assess our performance

without the impact of transactions or other items that are not related to our portfolio of properties. AFFO presented by us may not be comparable to AFFO reported by other REITs

that define AFFO differently. Furthermore, we believe that in order to facilitate a clear understanding of our operating results, AFFO should be examined in conjunction with net

income (loss) calculated in accordance with GAAP and presented in our consolidated financial statements. AFFO should not be considered as an alternative to net income (loss) as an

indication of our performance or to cash flows as a measure of our liquidity or ability to make distributions.

Adjusted Earnings before Interest, Taxes, Depreciation and Amortization, Net Operating Income, Cash Net Operating Income and Cash Paid for Interest.

We believe that Adjusted EBITDA, which is defined as earnings before interest, taxes, depreciation and amortization adjusted for acquisition, transaction and other costs, other non-cash items and including our pro-rata share from unconsolidated joint ventures, is an appropriate measure of our ability to incur and service debt. We also exclude revenue attributable

to the reimbursement by third parties of financing costs that we originally incurred because these revenues are not, in our view, related to operating performance. All paid and accrued

acquisition, transaction and other costs (including prepayment penalties for debt extinguishments) and certain other expenses, expenses related to our European tax restructuring and

transition costs related to the Merger and Internalization, negatively impact our operating performance during the period in which expenses are incurred or properties are acquired and

will also have negative effects on returns to investors, but are not reflective of on-going performance. Adjusted EBITDA should not be considered as an alternative to cash flows from

operating activities, as a measure of our liquidity or as an alternative to net income (loss) as calculated in accordance with GAAP as an indicator of our operating activities. Other REITs

may calculate Adjusted EBITDA differently and our calculation should not be compared to that of other REITs.

APPENDIX: FINANCIAL DEFINITIONS |

| 24

NOI is a non-GAAP financial measure equal to net income (loss), the most directly comparable GAAP financial measure, less discontinued operations, interest, other income and

income from preferred equity investments and investment securities, plus corporate general and administrative expense, acquisition, transaction and other costs, depreciation and

amortization, other noncash expenses and interest expense. We use NOI internally as a performance measure and believe NOI provides useful information to investors regarding our

financial condition and results of operations because it reflects only those income and expense items that are incurred at the property level. Therefore, we believe NOI is a useful

measure for evaluating the operating performance of our real estate assets and to make decisions about resource allocations. Further, we believe NOI is useful to investors as a

performance measure because, when compared across periods, NOI reflects the impact on operations from trends in occupancy rates, rental rates, operating costs and acquisition

activity on an unlevered basis, providing perspective not immediately apparent from net income. NOI excludes certain components from net income in order to provide results that are

more closely related to a property’s results of operations. For example, interest expense is not necessarily linked to the operating performance of a real estate asset and is often incurred

at the corporate level as opposed to the property level. In addition, depreciation and amortization, because of historical cost accounting and useful life estimates, may distort operating

performance at the property level. NOI presented by us may not be comparable to NOI reported by other REITs that define NOI differently. We believe that in order to facilitate a

clear understanding of our operating results, NOI should be examined in conjunction with net income (loss) as presented in our consolidated financial statements. NOI should not be

considered as an alternative to net income (loss) as calculated in accordance with GAAP as an indication of our performance or to cash flows as a measure of our liquidity.

Adjusted Earnings before Interest, Taxes, Depreciation and Amortization, Net Operating Income, Cash Net Operating Income and Cash Paid for Interest (Cont’d)

Cash NOI is a non-GAAP financial measure that is intended to reflect the performance of our properties. We define Cash NOI as net operating income (which is separately defined

herein) excluding amortization of above/below market lease intangibles and straight-line adjustments that are included in GAAP lease revenues. We believe that Cash NOI is a helpful

measure that both investors and management can use to evaluate the current financial performance of our properties and it allows for comparison of our operating performance

between periods and to other REITs. Cash NOI should not be considered as an alternative to net income (loss) as calculated in accordance with GAAP as an indication of our financial

performance, or to cash flows as a measure of liquidity or our ability to fund all needs. The method by which we calculate and present Cash NOI may not be directly comparable to the

way other REITs calculate and present Cash NOI.

Cash Paid for Interest is calculated based on the interest expense less non-cash portion of interest expense and amortization of mortgage (discount) premium, net. Management believes

that Cash Paid for Interest provides useful information to investors to assess our overall solvency and financial flexibility. Cash Paid for Interest should not be considered as an

alternative to interest expense as determined in accordance with GAAP or any other GAAP financial measures and should only be considered together with and as a supplement to our

financial information prepared in accordance with GAAP.

APPENDIX: FINANCIAL DEFINITIONS |

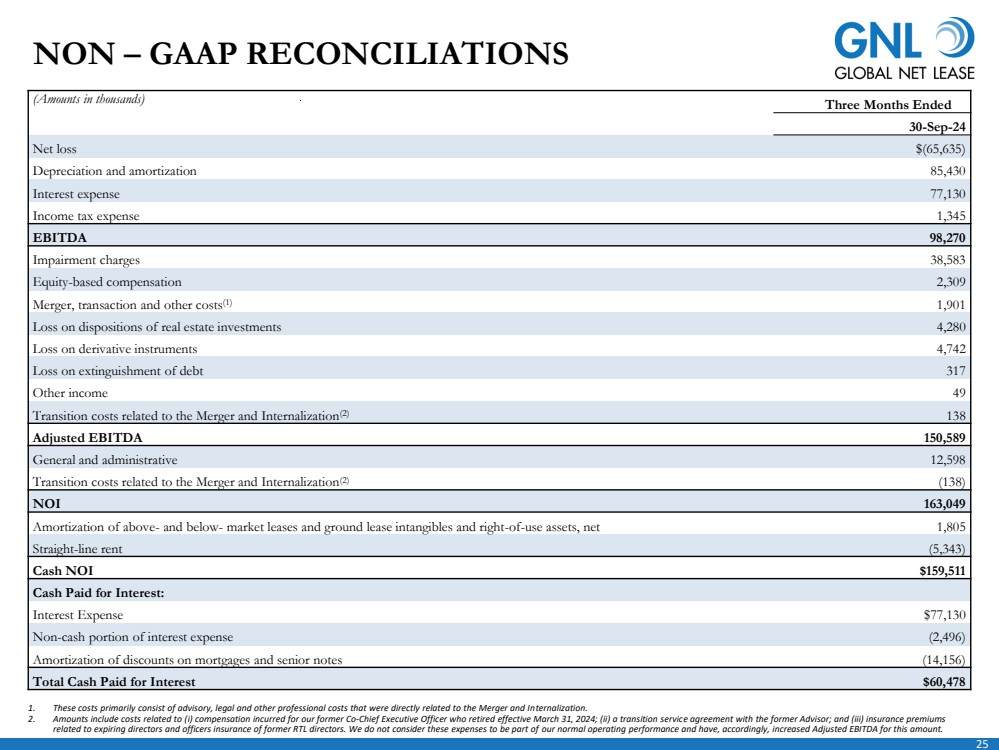

| 25

NON – GAAP RECONCILIATIONS

1. These costs primarily consist of advisory, legal and other professional costs that were directly related to the Merger and Internalization.

2. Amounts include costs related to (i) compensation incurred for our former Co-Chief Executive Officer who retired effective March 31, 2024; (ii) a transition service agreement with the former Advisor; and (iii) insurance premiums

related to expiring directors and officers insurance of former RTL directors. We do not consider these expenses to be part of our normal operating performance and have, accordingly, increased Adjusted EBITDA for this amount.

(Amounts in thousands) Three Months Ended

30-Sep-24

Net loss $(65,635)

Depreciation and amortization 85,430

Interest expense 77,130

Income tax expense 1,345

EBITDA 98,270

Impairment charges 38,583

Equity-based compensation 2,309

Merger, transaction and other costs(1) 1,901

Loss on dispositions of real estate investments 4,280

Loss on derivative instruments 4,742

Loss on extinguishment of debt 317

Other income 49

Transition costs related to the Merger and Internalization(2) 138

Adjusted EBITDA 150,589

General and administrative 12,598

Transition costs related to the Merger and Internalization(2) (138)

NOI 163,049

Amortization of above- and below- market leases and ground lease intangibles and right-of-use assets, net 1,805

Straight-line rent (5,343)

Cash NOI $159,511

Cash Paid for Interest:

Interest Expense $77,130

Non-cash portion of interest expense (2,496)

Amortization of discounts on mortgages and senior notes (14,156)

Total Cash Paid for Interest $60,478 |

| 26

(Amounts in thousands) Three Months Ended

30-Sep-24

Net loss attributable to common stockholders (in accordance with GAAP) $(76,571)

Impairment charges 38,583

Depreciation and amortization 85,430

Gain on dispositions of real estate investments 4,280

FFO (as defined by NAREIT) attributable to stockholders 51,722

Merger, transaction and other costs(1) 1,901

Loss on extinguishment of debt 317

Core FFO attributable to stockholders 53,940

Non-cash equity-based compensation 2,309

Non-cash portion of interest expense 2,496

Amortization related to above- and below- market lease intangibles and right-of-use assets, net 1,805

Straight-line rent (5,343)

Eliminate unrealized losses on foreign currency transactions(2) 4,360

Amortization of mortgage discounts 14,156

Transition costs related to the Merger and Internalization(3) 138

Forfeited disposition deposit(4) (5)

Adjusted funds from operations (AFFO) attributable to stockholders $73,856

Weighted-average shares outstanding – Basic and Diluted 230,463

Net loss per share attributable to common stockholders $(0.33)

FFO per share $0.22

Core FFO per share $0.23

AFFO per share $0.32

Dividends declared $63,722

NON – GAAP RECONCILIATIONS

1. These costs primarily consist of advisory, legal and other professional costs that were directly related to the Merger and Internalization.

2. For AFFO purposes, we add back unrealized (gain) loss. For the three months ended September 30, 2024, the gain on derivative instruments was $4.7 million which consisted of unrealized gains of $4.4 million and realized gains of

$0.3 million

3. Amounts include costs related to (i) compensation incurred for our former Co-Chief Executive Officer who retired effective March 31, 2024; (ii) a transition service agreement with the former Advisor; and (iii) insurance premiums

related to expiring directors and officers insurance of former RTL directors. We do not consider these expenses to be part of our normal operating performance and have, accordingly, increased AFFO for this amount.

4. Represents a forfeited deposit from a potential buyer of one of our properties, which is recorded in other income in our consolidated statement of operations. We do not consider this income part of our normal operating performance,

and have, accordingly, decreased AFFO for this amount. |

Cover

|

Nov. 06, 2024 |

| Document Information [Line Items] |

|

| Document Type |

8-K

|

| Amendment Flag |

false

|

| Document Period End Date |

Nov. 06, 2024

|

| Entity File Number |

001-37390

|

| Entity Registrant Name |

Global Net Lease, Inc.

|

| Entity Central Index Key |

0001526113

|

| Entity Tax Identification Number |

45-2771978

|

| Entity Incorporation, State or Country Code |

MD

|

| Entity Address, Address Line One |

650 Fifth Avenue

|

| Entity Address, Address Line Two |

30th Floor

|

| Entity Address, City or Town |

New York

|

| Entity Address, State or Province |

NY

|

| Entity Address, Postal Zip Code |

10019

|

| City Area Code |

332

|

| Local Phone Number |

265-2020

|

| Written Communications |

false

|

| Soliciting Material |

false

|

| Pre-commencement Tender Offer |

false

|

| Pre-commencement Issuer Tender Offer |

false

|

| Entity Emerging Growth Company |

false

|

| Common Stock [Member] |

|

| Document Information [Line Items] |

|

| Title of 12(b) Security |

Common

Stock, $0.01 par value per share

|

| Trading Symbol |

GNL

|

| Security Exchange Name |

NYSE

|

| Series A Preferred Stock [Member] |

|

| Document Information [Line Items] |

|

| Title of 12(b) Security |

7.25%

Series A Cumulative Redeemable Preferred Stock, $0.01 par value per share

|

| Trading Symbol |

GNL PR A

|

| Security Exchange Name |

NYSE

|

| Series B Preferred Stock [Member] |

|

| Document Information [Line Items] |

|

| Title of 12(b) Security |

6.875%

Series B Cumulative Redeemable Perpetual Preferred Stock, $0.01 par value per share

|

| Trading Symbol |

GNL PR B

|

| Security Exchange Name |

NYSE

|

| Series D Preferred Stock [Member] |

|

| Document Information [Line Items] |

|

| Title of 12(b) Security |

7.50% Series D Cumulative Redeemable Perpetual Preferred Stock, $0.01 par

value per share

|

| Trading Symbol |

GNL PR D

|

| Security Exchange Name |

NYSE

|

| Series E Preferred Stock [Member] |

|

| Document Information [Line Items] |

|

| Title of 12(b) Security |

7.375%

Series E Cumulative Redeemable Perpetual Preferred Stock, $0.01 par value per share

|

| Trading Symbol |

GNL PR E

|

| Security Exchange Name |

NYSE

|

| X |

- DefinitionBoolean flag that is true when the XBRL content amends previously-filed or accepted submission.

| Name: |

dei_AmendmentFlag |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionFor the EDGAR submission types of Form 8-K: the date of the report, the date of the earliest event reported; for the EDGAR submission types of Form N-1A: the filing date; for all other submission types: the end of the reporting or transition period. The format of the date is YYYY-MM-DD.

| Name: |

dei_DocumentPeriodEndDate |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:dateItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe type of document being provided (such as 10-K, 10-Q, 485BPOS, etc). The document type is limited to the same value as the supporting SEC submission type, or the word 'Other'.

| Name: |

dei_DocumentType |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:submissionTypeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 1 such as Attn, Building Name, Street Name

| Name: |

dei_EntityAddressAddressLine1 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionAddress Line 2 such as Street or Suite number

| Name: |

dei_EntityAddressAddressLine2 |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- Definition

+ References

+ Details

| Name: |

dei_EntityAddressCityOrTown |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCode for the postal or zip code

| Name: |

dei_EntityAddressPostalZipCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the state or province.

| Name: |

dei_EntityAddressStateOrProvince |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:stateOrProvinceItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionA unique 10-digit SEC-issued value to identify entities that have filed disclosures with the SEC. It is commonly abbreviated as CIK. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityCentralIndexKey |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:centralIndexKeyItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionIndicate if registrant meets the emerging growth company criteria. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityEmergingGrowthCompany |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionCommission file number. The field allows up to 17 characters. The prefix may contain 1-3 digits, the sequence number may contain 1-8 digits, the optional suffix may contain 1-4 characters, and the fields are separated with a hyphen.

| Name: |

dei_EntityFileNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:fileNumberItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTwo-character EDGAR code representing the state or country of incorporation.

| Name: |

dei_EntityIncorporationStateCountryCode |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarStateCountryItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe exact name of the entity filing the report as specified in its charter, which is required by forms filed with the SEC. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityRegistrantName |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionThe Tax Identification Number (TIN), also known as an Employer Identification Number (EIN), is a unique 9-digit value assigned by the IRS. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b-2

| Name: |

dei_EntityTaxIdentificationNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:employerIdItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionLocal phone number for entity.

| Name: |

dei_LocalPhoneNumber |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:normalizedStringItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 13e

-Subsection 4c

| Name: |

dei_PreCommencementIssuerTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 14d

-Subsection 2b

| Name: |

dei_PreCommencementTenderOffer |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTitle of a 12(b) registered security. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection b

| Name: |

dei_Security12bTitle |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:securityTitleItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionName of the Exchange on which a security is registered. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Number 240

-Section 12

-Subsection d1-1

| Name: |

dei_SecurityExchangeName |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:edgarExchangeCodeItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as soliciting material pursuant to Rule 14a-12 under the Exchange Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Exchange Act

-Section 14a

-Number 240

-Subsection 12

| Name: |

dei_SolicitingMaterial |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionTrading symbol of an instrument as listed on an exchange.

| Name: |

dei_TradingSymbol |

| Namespace Prefix: |

dei_ |

| Data Type: |

dei:tradingSymbolItemType |

| Balance Type: |

na |

| Period Type: |

duration |

|

| X |

- DefinitionBoolean flag that is true when the Form 8-K filing is intended to satisfy the filing obligation of the registrant as written communications pursuant to Rule 425 under the Securities Act. Reference 1: http://www.xbrl.org/2003/role/presentationRef

-Publisher SEC

-Name Securities Act

-Number 230

-Section 425

| Name: |

dei_WrittenCommunications |

| Namespace Prefix: |

dei_ |

| Data Type: |

xbrli:booleanItemType |