false

0001295401

0001295401

2024-01-25

2024-01-25

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 8-K

Current Report

Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934

Date of Report (Date of earliest event

reported): January 25, 2024

The Bancorp, Inc.

(Exact name of registrant as specified in its charter)

Commission File Number: 000-51018

| Delaware |

|

23-3016517 |

| (State or other jurisdiction of |

|

(IRS Employer |

| incorporation) |

|

Identification No.) |

409 Silverside Road

Wilmington, DE 19809

(Address of principal executive offices, including

zip code)

302-385-5000

(Registrant’s telephone number, including

area code)

(Former name or former address, if changed since

last report)

Check the appropriate box below if the Form 8-K filing is intended

to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

[_] Written communications pursuant to Rule 425 under the

Securities Act (17 CFR 230.425)

[_] Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

[_] Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

[_] Pre-commencement communications pursuant to Rule 13e-4(c)

under the Exchange Act (17 CFR 240.13e-4(c))

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

|

Trading

Symbol(s) |

|

Name of each exchange on which registered |

| Common Stock, par value $1.00 per share |

|

TBBK |

|

Nasdaq Global Select |

Indicate by check mark whether the registrant is an emerging growth

company as defined in Rule 405 of the Securities Act of 1933 (§230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2).

[_] Emerging growth company

If an emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant

to Section 13(a) of the Exchange Act. [ ]

| Item 2.02. |

Results of Operations and Financial Condition |

On January 25, 2024, The Bancorp, Inc. (the

"Company") issued a press release regarding its earnings for the three and twelve months ended December 31, 2023. A copy

of this press release is furnished with this report as Exhibit 99.1.

| Item 7.01. |

Regulation FD Disclosure. |

The Company hereby furnishes the information set

forth in the presentation attached hereto as Exhibit 99.2, which is incorporated herein by reference.

The information being furnished pursuant to Item

2.02 and Item 7.01 in this Current Report, including the exhibits hereto, is to be considered “furnished” pursuant to Form

8-K and shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or otherwise

subject to the liabilities of that section. The information in this Current Report shall not be incorporated by reference into any registration

statement or other document pursuant to the Securities Act of 1933, as amended.

| Item 9.01. |

Financial Statements and Exhibits |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the

registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date:

January 25, 2024 |

The Bancorp, Inc. |

| |

|

|

| |

By: |

/s/ Paul Frenkiel |

| |

Name: |

Paul Frenkiel |

| |

Title: |

Chief Financial Officer and |

| |

|

Secretary |

Exhibit 99.1

The

Bancorp, Inc. Reports Fourth Quarter and Full Year 2023 Financial

Results and Updates 2024 Guidance

Wilmington, DE – January 25, 2024 – The Bancorp, Inc. ("The

Bancorp" or “we”) (NASDAQ: TBBK), a financial holding company, today reported financial results for the fourth quarter

and full year of 2023.

Highlights

| · | The Bancorp reported net income of $44.0 million, or $0.81 per diluted share, for the quarter ended December 31, 2023, compared

to net income of $40.2 million, or $0.71 per diluted share, for the quarter ended December 31, 2022. Excluding the tax effected impact

of a $10.0 million provision for credit loss on its only trust preferred security, non-GAAP adjusted diluted earnings per share amounted

to $0.95.* |

| · | Return on assets and equity for the quarter ended December 31, 2023 amounted to 2.4% and 22%, respectively, compared to 2.1% and 24%,

respectively, for the quarter ended December 31, 2022 (all percentages “annualized”). |

| · | Net interest income increased 20% to $92.2 million for the quarter ended December 31, 2023, compared to $76.8 million for the quarter

ended December 31, 2022. Net interest income increases reflected the impact of Federal Reserve rate increases on The Bancorp’s variable

rate loans and securities. |

| · | Net interest margin amounted to 5.26% for the quarter ended December 31, 2023, compared to 4.21% for the quarter ended December 31,

2022, and 5.07% for the quarter ended September 30, 2023. |

| · | Loans, net of deferred fees and costs were $5.36 billion at December 31, 2023, compared to $5.20 billion at September 30, 2023

and $5.49 billion at December 31, 2022. Those changes reflected an increase of 3% quarter over linked quarter and a decrease of 2% year

over year. |

| · | Gross dollar volume (“GDV”), representing the total amounts spent on prepaid and debit cards, increased $3.84 billion,

or 13%, to $33.29 billion for the quarter ended December 31, 2023, compared to the quarter ended December 31, 2022. The increase reflects

continued organic growth with existing partners and the impact of clients added within the past year. Total prepaid, debit card, ACH and

other payment fees increased 15% to $25.1 million for the fourth quarter of 2023 compared to the fourth quarter of 2022. |

| · | Small business loans (“SBL”), including those held at fair value, amounted to $896.2 million at December 31,

2023, or 13% higher year over year, and 4% quarter over linked quarter, excluding $28.6 million of loans with related secured borrowings. |

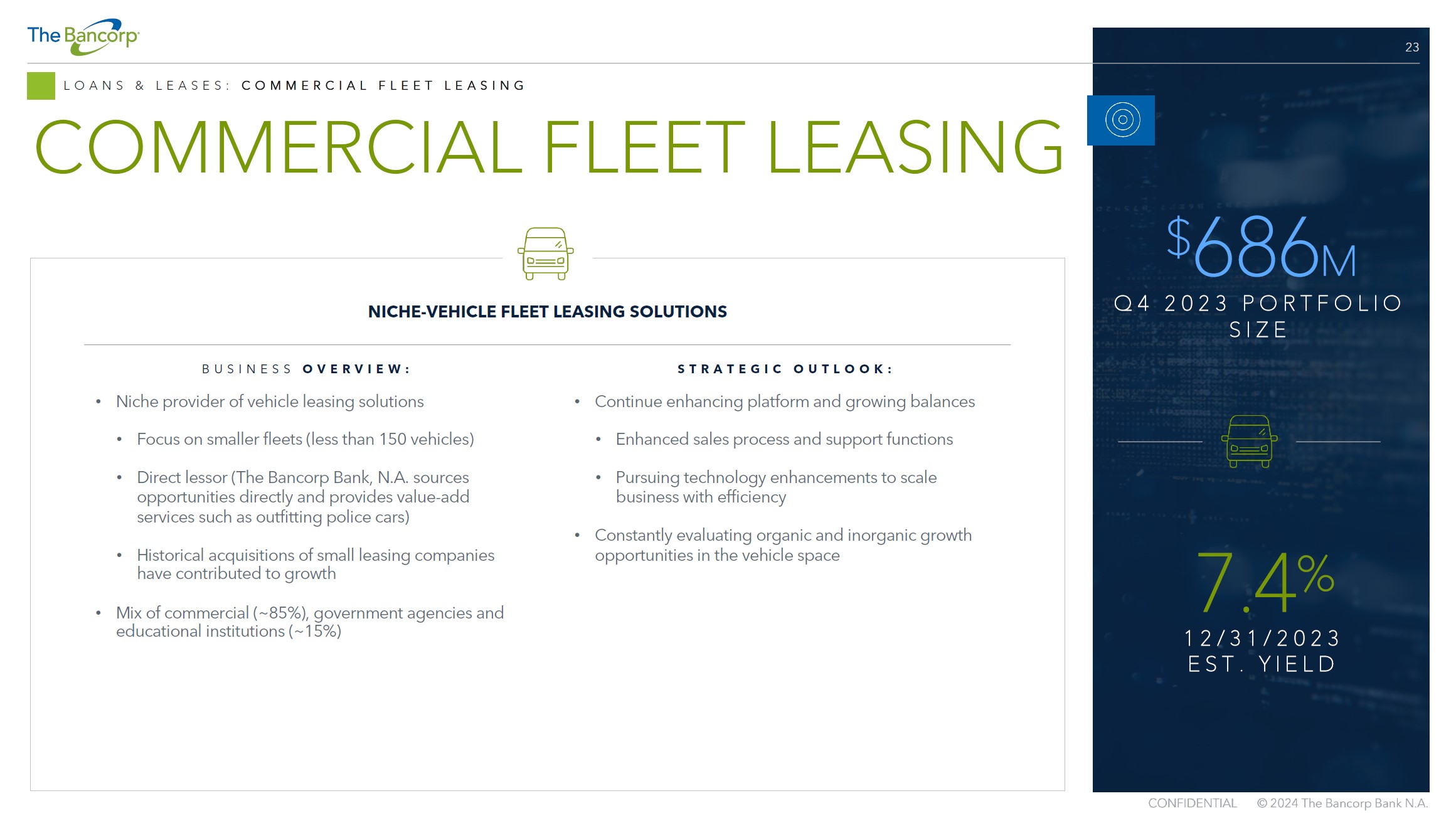

| · | Direct lease financing balances increased 8% year over year to $685.7 million at December 31, 2023, and 2% quarter over September

30, 2023. |

| · | At December 31, 2023, real estate bridge loans of $2.00 billion had grown 8% compared to the $1.85 billion balance at September 30,

2023, and 20% compared to the December 31, 2022 balance of $1.67 billion. These real estate bridge loans consist entirely of apartment

buildings. |

| · | Security backed lines of credit (“SBLOC”), insurance backed lines of credit (“IBLOC”) and investment advisor

financing loans collectively decreased 26% year over year and decreased 4% quarter over linked quarter to $1.85 billion at December

31, 2023. |

| · | The average interest rate on $6.37 billion of average deposits and interest-bearing liabilities during the fourth quarter of

2023 was 2.51%. Average deposits of $6.25 billion for the fourth quarter of 2023 reflected a decrease of 6% from the $6.62 billion

of average deposits for the quarter ended December 31, 2022, and a 1% decrease from $6.29 billion of average deposits for the quarter

ended September 30, 2023. The decreases reflected the planned exit of $200 million of higher cost funds on July 1, 2023. Not included

in deposit totals are deposits which are sold to other financial institutions totaling $300.7 million at December 31, 2023. |

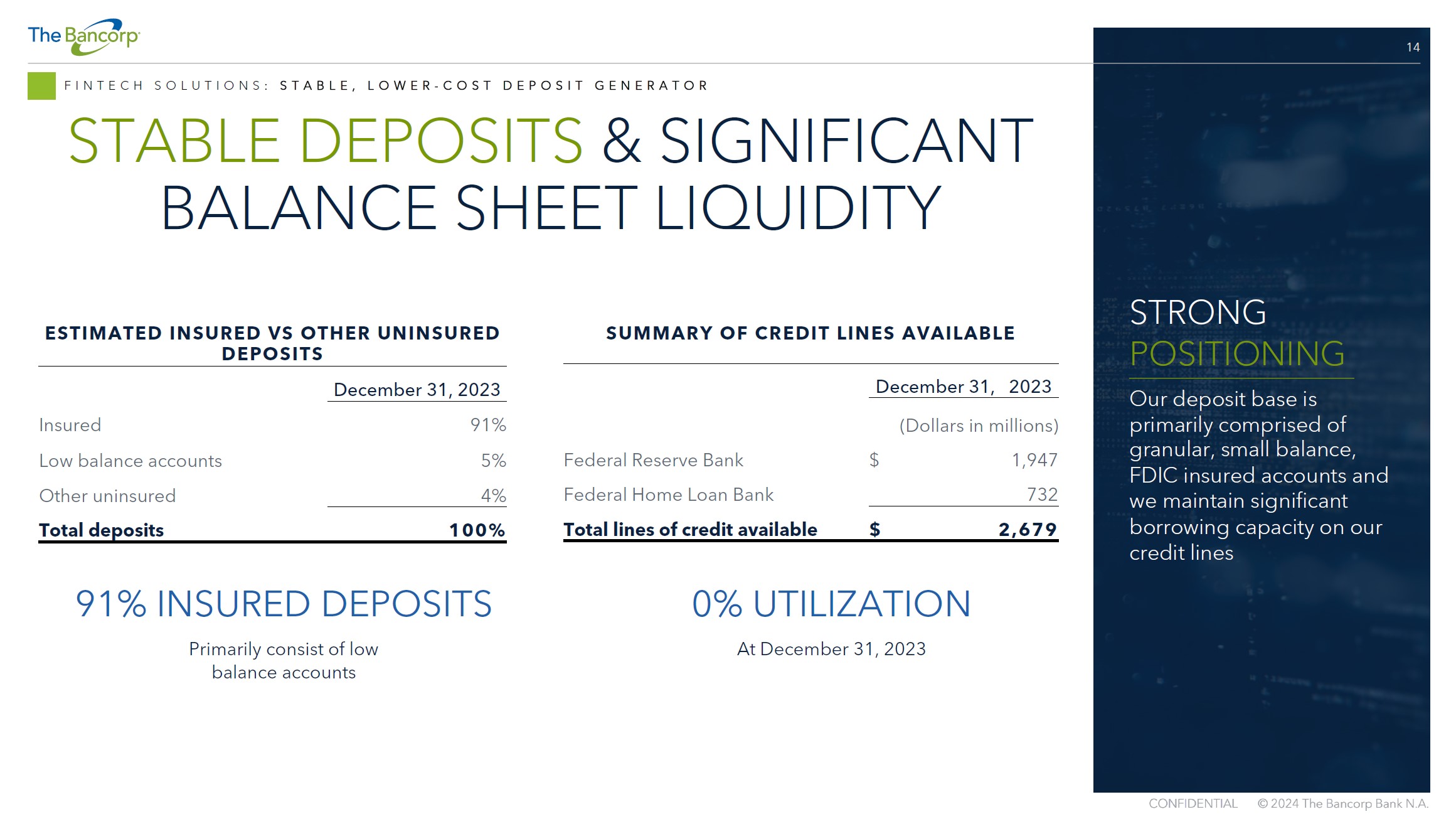

| · | The Bancorp emphasizes safety and soundness, and liquidity. The vast majority of its funding is comprised of insured and small balance

accounts. The Bancorp also has lines of credit with U.S. government agencies totaling approximately $2.7 billion as of December 31, 2023,

as well as access to other liquidity. |

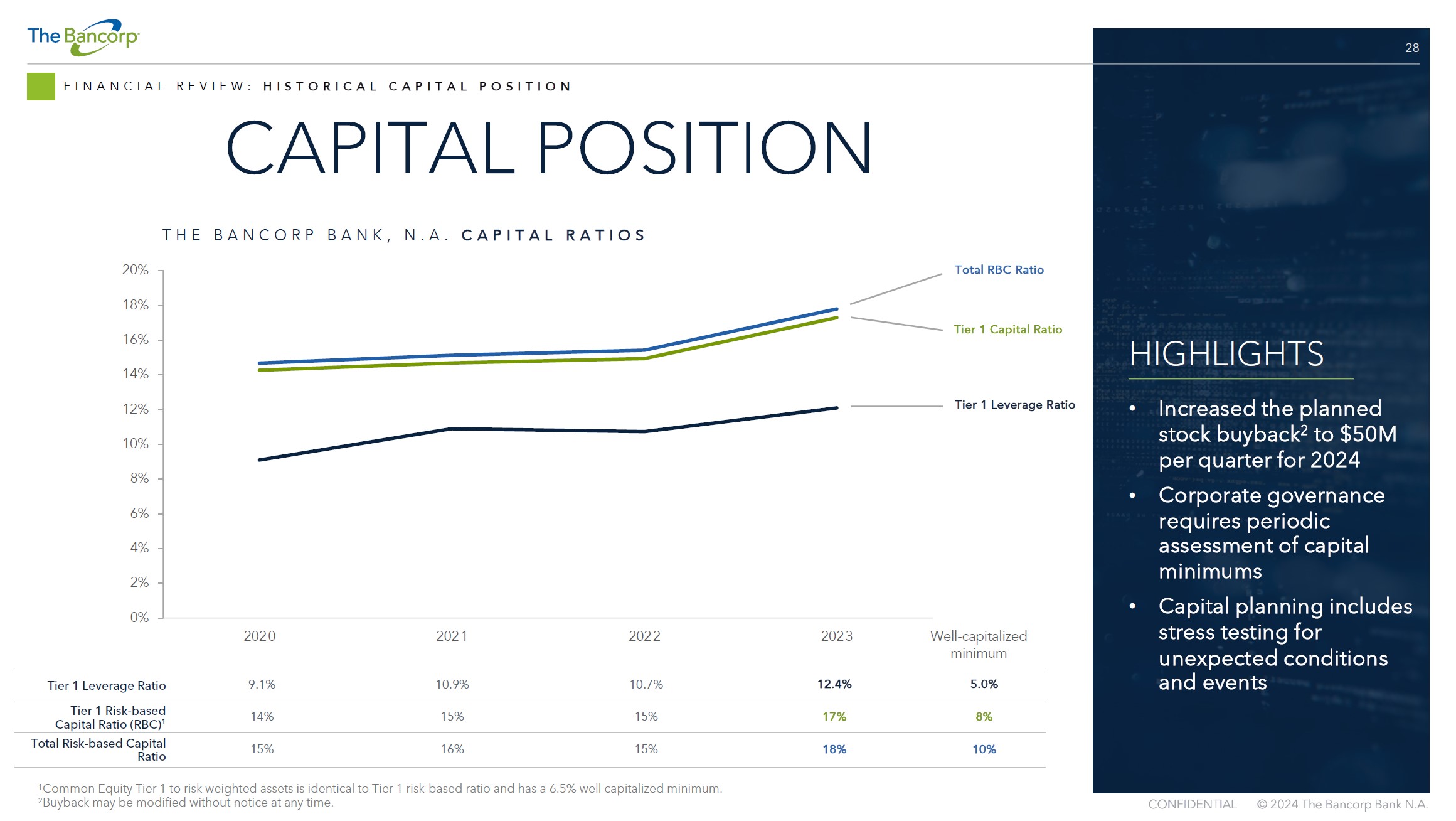

| · | As of December 31, 2023, tier one capital to assets (leverage), tier one capital to risk-weighted assets, total capital to risk-weighted

assets and common equity-tier 1 to risk-weighted assets ratios were 11.19%, 15.66%, 16.23% and 15.66%, respectively, compared to well-capitalized

minimums of 5%, 8%, 10% and 6.5%, respectively. The Bancorp and its wholly owned subsidiary, The Bancorp Bank, National Association, each

remain well capitalized under banking regulations. |

| · | Book value per common share at December 31, 2023 was $15.17 compared to $12.46 per common share at December

31, 2022, an increase of 22%. |

| · | The Bancorp repurchased 664,499 shares of its common stock at an average cost of $37.62

per share during the quarter ended December 31, 2023. |

*The Bank purchased a $10.0 million trust preferred security in 2006, which

is the only such security in its portfolios. In the fourth quarter of 2023, the Bank took a charge for the full amount of the security

through a provision for credit loss. The following reconciliation of GAAP to non-GAAP adjusted net income and diluted earnings per share

(“EPS”) for the fourth quarter of 2023, adjusts for the impact of that charge.

| | |

Net Income (000’s) | |

EPS |

| GAAP | |

$ | 44,028 | | |

$ | 0.81 | |

| Provision for credit loss on trust preferred security, net of tax effect | |

| 7,489 | | |

| 0.14 | |

| As adjusted, non-GAAP | |

$ | 51,517 | | |

$ | 0.95 | |

CEO and President Damian Kozlowski commented, “In 2023, we rode the

waves of market turmoil and interest rate hikes and demonstrated the superiority of our rigorous commitment to our business partners,

safety and soundness and shareholder advocacy. The strength of our business model and our comprehensive and integrated risk

management showed that sound fundamental banking can reduce event risk and create opportunities for exemplar performance even in times

of economic dislocations. We are confirming 2024 guidance of $4.25 a share without including the impact of share buybacks of $200 million

for the year, or $50 million a quarter.”

Conference Call Webcast

You may access the LIVE webcast of The Bancorp's Quarterly Earnings Conference

Call at 8:00 AM ET Friday, January 26, 2024 by clicking on the webcast link on The Bancorp's homepage at www.thebancorp.com. Or you may

dial 1.888.259.6580, conference code 18545154. You may listen to the replay of the webcast following the live call on The Bancorp's investor

relations website or telephonically until Friday, February 2, 2024 by dialing 1.877.674.7070, access code 545154#.

About The Bancorp

The Bancorp, Inc. (NASDAQ: TBBK), headquartered in Wilmington, Delaware,

through its subsidiary, The Bancorp Bank, National Association, (or “The Bancorp Bank, N.A.”) provides non-bank financial

companies with the people, processes, and technology to meet their unique banking needs. Through its Fintech Solutions, Institutional

Banking, Commercial Lending, and Real Estate Bridge Lending businesses, The Bancorp provides partner-focused solutions paired with cutting-edge

technology for companies that range from entrepreneurial startups to Fortune 500 companies. With over 20 years of experience, The Bancorp

has become a leader in the financial services industry, earning recognition as the #1 issuer of prepaid cards in the U.S., a nationwide

provider of bridge financing for real estate capital improvement plans, an SBA National Preferred Lender, a leading provider of securities-backed

lines of credit, with one of the few bank-owned commercial vehicle leasing groups. By its company-wide commitment to excellence, The Bancorp

has also been ranked as one of the 100 Fastest-Growing Companies by Fortune, a Top 50 Employer by Equal Opportunity Magazine and was selected

to be included in the S&P Small Cap 600. For more about The Bancorp, visit https://thebancorp.com/.

Forward-Looking Statements

Statements in this earnings release regarding The Bancorp’s business

which are not historical facts are "forward-looking statements." These statements may be identified by the use of forward-looking

terminology, including but not limited to the words “intend,” “may,” “believe,” “will,”

“expect,” “look,” “anticipate,” “plan,” “estimate,” “continue,”

or similar words, and are based on current expectations about important economic, political, and technological factors, among others,

and are subject to risks and uncertainties, which could cause the actual results, events or achievements to differ materially from those

set forth in or implied by the forward-looking statements and related assumptions. For further discussion of the risks and uncertainties

to which these forward-looking statements may be subject, see The Bancorp’s filings with the Securities and Exchange Commission,

including the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”

sections of those filings. The forward-looking statements speak only as of the date of this press release. The Bancorp does not undertake

to publicly revise or update forward-looking statements in this press release to reflect events or circumstances that arise after the

date of this press release, except as may be required under applicable law.

The Bancorp, Inc. Contact

Andres Viroslav

Director, Investor Relations

215-861-7990

andres.viroslav@thebancorp.com

Source: The Bancorp, Inc.

The Bancorp, Inc.

Financial highlights

(unaudited)

| | |

Three months ended | |

Year ended |

| | |

December 31, | |

December 31, |

| Consolidated condensed income statements | |

2023 | |

2022 | |

2023 | |

2022 |

| | |

(Dollars in thousands, except per share and share data) |

| | |

| |

| |

| |

|

| Net interest income | |

$ | 92,159 | | |

$ | 76,760 | | |

$ | 354,052 | | |

$ | 248,841 | |

| Provision for credit losses on loans | |

| 4,314 | | |

| 2,777 | | |

| 8,330 | | |

| 7,108 | |

| Provision for credit loss on security | |

| 10,000 | | |

| — | | |

| 10,000 | | |

| — | |

| Non-interest income | |

| | | |

| | | |

| | | |

| | |

| ACH, card and other payment processing fees | |

| 2,669 | | |

| 2,383 | | |

| 9,822 | | |

| 8,935 | |

| Prepaid, debit card and related fees | |

| 22,404 | | |

| 19,371 | | |

| 89,417 | | |

| 77,236 | |

| Net realized and unrealized (losses) gains on commercial loans, at fair value | |

| (426 | ) | |

| 2,269 | | |

| 3,745 | | |

| 13,531 | |

| Leasing related income | |

| 1,556 | | |

| 1,256 | | |

| 6,324 | | |

| 4,822 | |

| Other non-interest income | |

| 786 | | |

| 461 | | |

| 2,786 | | |

| 1,159 | |

| Total non-interest income | |

| 26,989 | | |

| 25,740 | | |

| 112,094 | | |

| 105,683 | |

| Non-interest expense | |

| | | |

| | | |

| | | |

| | |

| Salaries and employee benefits | |

| 27,628 | | |

| 27,520 | | |

| 121,055 | | |

| 105,368 | |

| Data processing expense | |

| 1,324 | | |

| 1,245 | | |

| 5,447 | | |

| 4,972 | |

| Legal expense | |

| 740 | | |

| 703 | | |

| 3,850 | | |

| 3,878 | |

| Legal settlement | |

| — | | |

| — | | |

| — | | |

| 1,152 | |

| Civil money penalty | |

| — | | |

| — | | |

| — | | |

| 1,750 | |

| FDIC insurance | |

| 724 | | |

| 944 | | |

| 2,957 | | |

| 3,270 | |

| Software | |

| 4,368 | | |

| 4,181 | | |

| 17,349 | | |

| 16,211 | |

| Other non-interest expense | |

| 10,826 | | |

| 8,882 | | |

| 40,384 | | |

| 32,901 | |

| Total non-interest expense | |

| 45,610 | | |

| 43,475 | | |

| 191,042 | | |

| 169,502 | |

| Income before income taxes | |

| 59,224 | | |

| 56,248 | | |

| 256,774 | | |

| 177,914 | |

| Income tax expense | |

| 15,196 | | |

| 16,007 | | |

| 64,478 | | |

| 47,701 | |

| Net income | |

| 44,028 | | |

| 40,241 | | |

| 192,296 | | |

| 130,213 | |

| | |

| | | |

| | | |

| | | |

| | |

| Net income per share - basic | |

$ | 0.82 | | |

$ | 0.72 | | |

$ | 3.52 | | |

$ | 2.30 | |

| | |

| | | |

| | | |

| | | |

| | |

| Net income per share - diluted | |

$ | 0.81 | | |

$ | 0.71 | | |

$ | 3.49 | | |

$ | 2.27 | |

| Weighted average shares - basic | |

| 53,549,138 | | |

| 55,885,015 | | |

| 54,506,065 | | |

| 56,556,303 | |

| Weighted average shares - diluted | |

| 54,201,312 | | |

| 56,588,011 | | |

| 55,053,497 | | |

| 57,268,946 | |

| Condensed consolidated balance sheets | |

December 31, | |

September 30, | |

June 30, | |

December 31, |

| | |

2023 (unaudited) | |

2023 (unaudited) | |

2023 (unaudited) | |

2022 |

| | |

(Dollars in thousands, except share data) |

| Assets: | |

| |

| |

| |

|

| Cash and cash equivalents | |

| | | |

| | | |

| | | |

| | |

| Cash and due from banks | |

$ | 4,820 | | |

$ | 4,881 | | |

$ | 6,496 | | |

$ | 24,063 | |

| Interest earning deposits at Federal Reserve Bank | |

| 1,033,270 | | |

| 898,533 | | |

| 874,050 | | |

| 864,126 | |

| Total cash and cash equivalents | |

| 1,038,090 | | |

| 903,414 | | |

| 880,546 | | |

| 888,189 | |

| | |

| | | |

| | | |

| | | |

| | |

| Investment securities, available-for-sale, at fair value, net of $10.0 million allowance for credit loss | |

| 747,534 | | |

| 756,636 | | |

| 776,410 | | |

| 766,016 | |

| Commercial loans, at fair value | |

| 332,766 | | |

| 379,603 | | |

| 396,581 | | |

| 589,143 | |

| Loans, net of deferred fees and costs | |

| 5,361,139 | | |

| 5,198,972 | | |

| 5,267,574 | | |

| 5,486,853 | |

| Allowance for credit losses | |

| (27,378 | ) | |

| (24,145 | ) | |

| (23,284 | ) | |

| (22,374 | ) |

| Loans, net | |

| 5,333,761 | | |

| 5,174,827 | | |

| 5,244,290 | | |

| 5,464,479 | |

| Federal Home Loan Bank, Atlantic Central Bankers Bank, and Federal Reserve Bank stock | |

| 15,591 | | |

| 20,157 | | |

| 20,157 | | |

| 12,629 | |

| Premises and equipment, net | |

| 27,474 | | |

| 28,978 | | |

| 26,408 | | |

| 18,401 | |

| Accrued interest receivable | |

| 37,534 | | |

| 34,159 | | |

| 34,062 | | |

| 32,005 | |

| Intangible assets, net | |

| 1,651 | | |

| 1,751 | | |

| 1,850 | | |

| 2,049 | |

| Other real estate owned | |

| 16,949 | | |

| 18,756 | | |

| 20,952 | | |

| 21,210 | |

| Deferred tax asset, net | |

| 21,219 | | |

| 20,379 | | |

| 19,215 | | |

| 19,703 | |

| Other assets | |

| 133,126 | | |

| 127,107 | | |

| 122,435 | | |

| 89,176 | |

| Total assets | |

$ | 7,705,695 | | |

$ | 7,465,767 | | |

$ | 7,542,906 | | |

$ | 7,903,000 | |

| | |

| | | |

| | | |

| | | |

| | |

| Liabilities: | |

| | | |

| | | |

| | | |

| | |

| Deposits | |

| | | |

| | | |

| | | |

| | |

| Demand and interest checking | |

$ | 6,630,251 | | |

$ | 6,455,043 | | |

$ | 6,554,967 | | |

$ | 6,559,617 | |

| Savings and money market | |

| 50,659 | | |

| 49,428 | | |

| 68,084 | | |

| 140,496 | |

| Time deposits, $100,000 and over | |

| — | | |

| — | | |

| — | | |

| 330,000 | |

| Total deposits | |

| 6,680,910 | | |

| 6,504,471 | | |

| 6,623,051 | | |

| 7,030,113 | |

| | |

| | | |

| | | |

| | | |

| | |

| Securities sold under agreements to repurchase | |

| 42 | | |

| 42 | | |

| 42 | | |

| 42 | |

| Senior debt | |

| 95,859 | | |

| 95,771 | | |

| 95,682 | | |

| 99,050 | |

| Subordinated debenture | |

| 13,401 | | |

| 13,401 | | |

| 13,401 | | |

| 13,401 | |

| Other long-term borrowings | |

| 38,561 | | |

| 9,861 | | |

| 9,917 | | |

| 10,028 | |

| Other liabilities | |

| 69,641 | | |

| 68,533 | | |

| 51,646 | | |

| 56,335 | |

| Total liabilities | |

$ | 6,898,414 | | |

$ | 6,692,079 | | |

$ | 6,793,739 | | |

$ | 7,208,969 | |

| | |

| | | |

| | | |

| | | |

| | |

| Shareholders' equity: | |

| | | |

| | | |

| | | |

| | |

| Common stock - authorized, 75,000,000 shares of $1.00 par value; 53,202,630 and 55,689,627 shares issued and outstanding at December 31, 2023 and 2022, respectively | |

| 53,203 | | |

| 53,867 | | |

| 54,542 | | |

| 55,690 | |

| Additional paid-in capital | |

| 212,431 | | |

| 234,320 | | |

| 256,115 | | |

| 299,279 | |

| Retained earnings | |

| 561,615 | | |

| 517,587 | | |

| 467,450 | | |

| 369,319 | |

| Accumulated other comprehensive loss | |

| (19,968 | ) | |

| (32,086 | ) | |

| (28,940 | ) | |

| (30,257 | ) |

| Total shareholders' equity | |

| 807,281 | | |

| 773,688 | | |

| 749,167 | | |

| 694,031 | |

| | |

| | | |

| | | |

| | | |

| | |

| Total liabilities and shareholders' equity | |

$ | 7,705,695 | | |

$ | 7,465,767 | | |

$ | 7,542,906 | | |

$ | 7,903,000 | |

| Average balance sheet and net interest income | |

Three months ended December 31, 2023 | |

Three months ended December 31, 2022 |

| | |

(Dollars in thousands; unaudited) |

| Assets: | |

Average

Balance | |

Interest(1) | |

Average

Rate | |

Average

Balance | |

Interest(1) | |

Average

Rate |

| | |

| |

| |

| |

| |

| |

|

| Interest earning assets: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loans, net of deferred fees and costs(2) | |

$ | 5,583,467 | | |

$ | 112,334 | | |

| 8.05 | % | |

$ | 6,083,587 | | |

$ | 94,477 | | |

| 6.21 | % |

| Leases-bank qualified(3) | |

| 4,658 | | |

| 109 | | |

| 9.36 | % | |

| 2,952 | | |

| 50 | | |

| 6.78 | % |

| Investment securities-taxable | |

| 747,384 | | |

| 10,258 | | |

| 5.49 | % | |

| 782,046 | | |

| 8,483 | | |

| 4.34 | % |

| Investment securities-nontaxable(3) | |

| 2,895 | | |

| 49 | | |

| 6.77 | % | |

| 3,559 | | |

| 32 | | |

| 3.60 | % |

| Interest earning deposits at Federal Reserve Bank | |

| 677,524 | | |

| 9,356 | | |

| 5.52 | % | |

| 424,255 | | |

| 3,886 | | |

| 3.66 | % |

| Net interest earning assets | |

| 7,015,928 | | |

| 132,106 | | |

| 7.53 | % | |

| 7,296,399 | | |

| 106,928 | | |

| 5.86 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Allowance for credit losses | |

| (24,070 | ) | |

| | | |

| | | |

| (20,227 | ) | |

| | | |

| | |

| Other assets | |

| 356,785 | | |

| | | |

| | | |

| 223,692 | | |

| | | |

| | |

| | |

$ | 7,348,643 | | |

| | | |

| | | |

$ | 7,499,864 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Liabilities and Shareholders' Equity: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Deposits: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Demand and interest checking | |

$ | 6,204,048 | | |

$ | 37,830 | | |

| 2.44 | % | |

$ | 5,891,947 | | |

$ | 21,350 | | |

| 1.45 | % |

| Savings and money market | |

| 46,428 | | |

| 392 | | |

| 3.38 | % | |

| 474,302 | | |

| 4,332 | | |

| 3.65 | % |

| Time deposits | |

| — | | |

| — | | |

| — | | |

| 257,231 | | |

| 2,193 | | |

| 3.41 | % |

| Total deposits | |

| 6,250,476 | | |

| 38,222 | | |

| 2.45 | % | |

| 6,623,480 | | |

| 27,875 | | |

| 1.68 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Short-term borrowings | |

| 2,717 | | |

| 37 | | |

| 5.45 | % | |

| 26,847 | | |

| 271 | | |

| 4.04 | % |

| Repurchase agreements | |

| 41 | | |

| — | | |

| — | | |

| 42 | | |

| — | | |

| — | |

| Long-term borrowings | |

| 10,144 | | |

| 125 | | |

| 4.94 | % | |

| 38,951 | | |

| 498 | | |

| 5.11 | % |

| Subordinated debentures | |

| 13,401 | | |

| 296 | | |

| 8.84 | % | |

| 13,401 | | |

| 226 | | |

| 6.75 | % |

| Senior debt | |

| 95,808 | | |

| 1,234 | | |

| 5.15 | % | |

| 99,005 | | |

| 1,280 | | |

| 5.17 | % |

| Total deposits and liabilities | |

| 6,372,587 | | |

| 39,914 | | |

| 2.51 | % | |

| 6,801,726 | | |

| 30,150 | | |

| 1.77 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Other liabilities | |

| 185,572 | | |

| | | |

| | | |

| 19,254 | | |

| | | |

| | |

| Total liabilities | |

| 6,558,159 | | |

| | | |

| | | |

| 6,820,980 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shareholders' equity | |

| 790,484 | | |

| | | |

| | | |

| 678,884 | | |

| | | |

| | |

| | |

$ | 7,348,643 | | |

| | | |

| | | |

$ | 7,499,864 | | |

| | | |

| | |

| Net interest income on tax equivalent basis(3) | |

| | | |

$ | 92,192 | | |

| | | |

| | | |

$ | 76,778 | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Tax equivalent adjustment | |

| | | |

| 33 | | |

| | | |

| | | |

| 18 | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net interest income | |

| | | |

$ | 92,159 | | |

| | | |

| | | |

$ | 76,760 | | |

| | |

| Net interest margin(3) | |

| | | |

| | | |

| 5.26 | % | |

| | | |

| | | |

| 4.21 | % |

| (1)Interest on loans for 2023 and 2022 includes $5,000 and $12,000, respectively, of interest and fees on PPP loans. |

| (2)Includes commercial loans, at fair value. All periods include non-accrual loans. |

| (3)Full taxable equivalent basis, using 21% respective statutory federal tax rates in 2023 and 2022. |

| Average balance sheet and net interest income | |

Year ended December 31, 2023 | |

Year ended December 31, 2022 |

| | |

(Dollars in thousands; unaudited) |

| Assets: | |

Average

Balance | |

Interest(1) | |

Average

Rate | |

Average

Balance | |

Interest(1) | |

Average

Rate |

| | |

| |

| |

| |

| |

| |

|

| Interest earning assets: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loans, net of deferred fees and costs(2) | |

$ | 5,724,679 | | |

$ | 436,343 | | |

| 7.62 | % | |

$ | 5,670,957 | | |

$ | 275,651 | | |

| 4.86 | % |

| Leases-bank qualified(3) | |

| 4,106 | | |

| 388 | | |

| 9.45 | % | |

| 3,479 | | |

| 235 | | |

| 6.75 | % |

| Investment securities-taxable | |

| 766,906 | | |

| 39,078 | | |

| 5.10 | % | |

| 855,629 | | |

| 25,598 | | |

| 2.99 | % |

| Investment securities-nontaxable(3) | |

| 3,118 | | |

| 193 | | |

| 6.19 | % | |

| 3,559 | | |

| 125 | | |

| 3.51 | % |

| Interest earning deposits at Federal Reserve Bank | |

| 649,873 | | |

| 33,627 | | |

| 5.17 | % | |

| 479,791 | | |

| 6,762 | | |

| 1.41 | % |

| Net interest earning assets | |

| 7,148,682 | | |

| 509,629 | | |

| 7.13 | % | |

| 7,013,415 | | |

| 308,371 | | |

| 4.40 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Allowance for credit losses | |

| (23,412 | ) | |

| | | |

| | | |

| (19,374 | ) | |

| | | |

| | |

| Other assets | |

| 292,491 | | |

| | | |

| | | |

| 213,491 | | |

| | | |

| | |

| | |

$ | 7,417,761 | | |

| | | |

| | | |

$ | 7,207,532 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Liabilities and Shareholders' Equity: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Deposits: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Demand and interest checking | |

$ | 6,308,509 | | |

$ | 144,814 | | |

| 2.30 | % | |

$ | 5,670,818 | | |

$ | 39,872 | | |

| 0.70 | % |

| Savings and money market | |

| 78,074 | | |

| 2,857 | | |

| 3.66 | % | |

| 510,370 | | |

| 8,524 | | |

| 1.67 | % |

| Time deposits | |

| 20,794 | | |

| 858 | | |

| 4.13 | % | |

| 86,907 | | |

| 2,740 | | |

| 3.15 | % |

| Total deposits | |

| 6,407,377 | | |

| 148,529 | | |

| 2.32 | % | |

| 6,268,095 | | |

| 51,136 | | |

| 0.82 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Short-term borrowings | |

| 5,739 | | |

| 271 | | |

| 4.72 | % | |

| 60,312 | | |

| 1,538 | | |

| 2.55 | % |

| Repurchase agreements | |

| 41 | | |

| — | | |

| — | | |

| 41 | | |

| — | | |

| — | |

| Long-term borrowings | |

| 9,995 | | |

| 507 | | |

| 5.07 | % | |

| 39,202 | | |

| 1,004 | | |

| 2.56 | % |

| Subordinated debentures | |

| 13,401 | | |

| 1,121 | | |

| 8.37 | % | |

| 13,401 | | |

| 658 | | |

| 4.91 | % |

| Senior debt | |

| 96,864 | | |

| 5,027 | | |

| 5.19 | % | |

| 98,865 | | |

| 5,118 | | |

| 5.18 | % |

| Total deposits and liabilities | |

| 6,533,417 | | |

| 155,455 | | |

| 2.38 | % | |

| 6,479,916 | | |

| 59,454 | | |

| 0.92 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Other liabilities | |

| 133,688 | | |

| | | |

| | | |

| 54,374 | | |

| | | |

| | |

| Total liabilities | |

| 6,667,105 | | |

| | | |

| | | |

| 6,534,290 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shareholders' equity | |

| 750,656 | | |

| | | |

| | | |

| 673,242 | | |

| | | |

| | |

| | |

$ | 7,417,761 | | |

| | | |

| | | |

$ | 7,207,532 | | |

| | | |

| | |

| Net interest income on tax equivalent basis(3) | |

| | | |

$ | 354,174 | | |

| | | |

| | | |

$ | 248,917 | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Tax equivalent adjustment | |

| | | |

| 122 | | |

| | | |

| | | |

| 76 | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net interest income | |

| | | |

$ | 354,052 | | |

| | | |

| | | |

$ | 248,841 | | |

| | |

| Net interest margin(3) | |

| | | |

| | | |

| 4.95 | % | |

| | | |

| | | |

| 3.55 | % |

| |

| (1)Interest on loans for 2023 and 2022 includes $32,000 and $514,000, respectively, of interest and fees on PPP loans. |

| (2)Includes commercial loans, at fair value. All periods include non-accrual loans. |

| (3)Full taxable equivalent basis, using 21% respective statutory federal tax rates in 2023 and 2022. |

| Allowance for credit losses |

Year ended |

| |

December 31, |

|

December 31, |

| |

2023 (unaudited) |

|

2022 |

| |

(Dollars in thousands) |

| |

|

|

|

|

|

| Balance in the allowance for credit losses at beginning of period |

$ |

22,374 |

|

$ |

17,806 |

| |

|

|

|

|

|

| Loans charged-off: |

|

|

|

|

|

| SBA non-real estate |

|

871 |

|

|

885 |

| SBA commercial mortgage |

|

76 |

|

|

— |

| Direct lease financing |

|

3,666 |

|

|

576 |

| IBLOC |

|

24 |

|

|

— |

| Consumer - other |

|

3 |

|

|

— |

| Total |

|

4,640 |

|

|

1,461 |

| |

|

|

|

|

|

| Recoveries: |

|

|

|

|

|

| SBA non-real estate |

|

475 |

|

|

140 |

| SBA commercial mortgage |

|

75 |

|

|

— |

| Direct lease financing |

|

330 |

|

|

124 |

| Consumer - home equity |

|

299 |

|

|

— |

| Other loans |

|

— |

|

|

24 |

| Total |

|

1,179 |

|

|

288 |

| Net charge-offs |

|

3,461 |

|

|

1,173 |

| Provision for credit losses, excluding commitment provision |

|

8,465 |

|

|

5,741 |

| |

|

|

|

|

|

| Balance in allowance for credit losses at end of period |

$ |

27,378 |

|

$ |

22,374 |

| Net charge-offs/average loans |

|

0.07% |

|

|

0.03% |

| Net charge-offs/average assets |

|

0.05% |

|

|

0.02% |

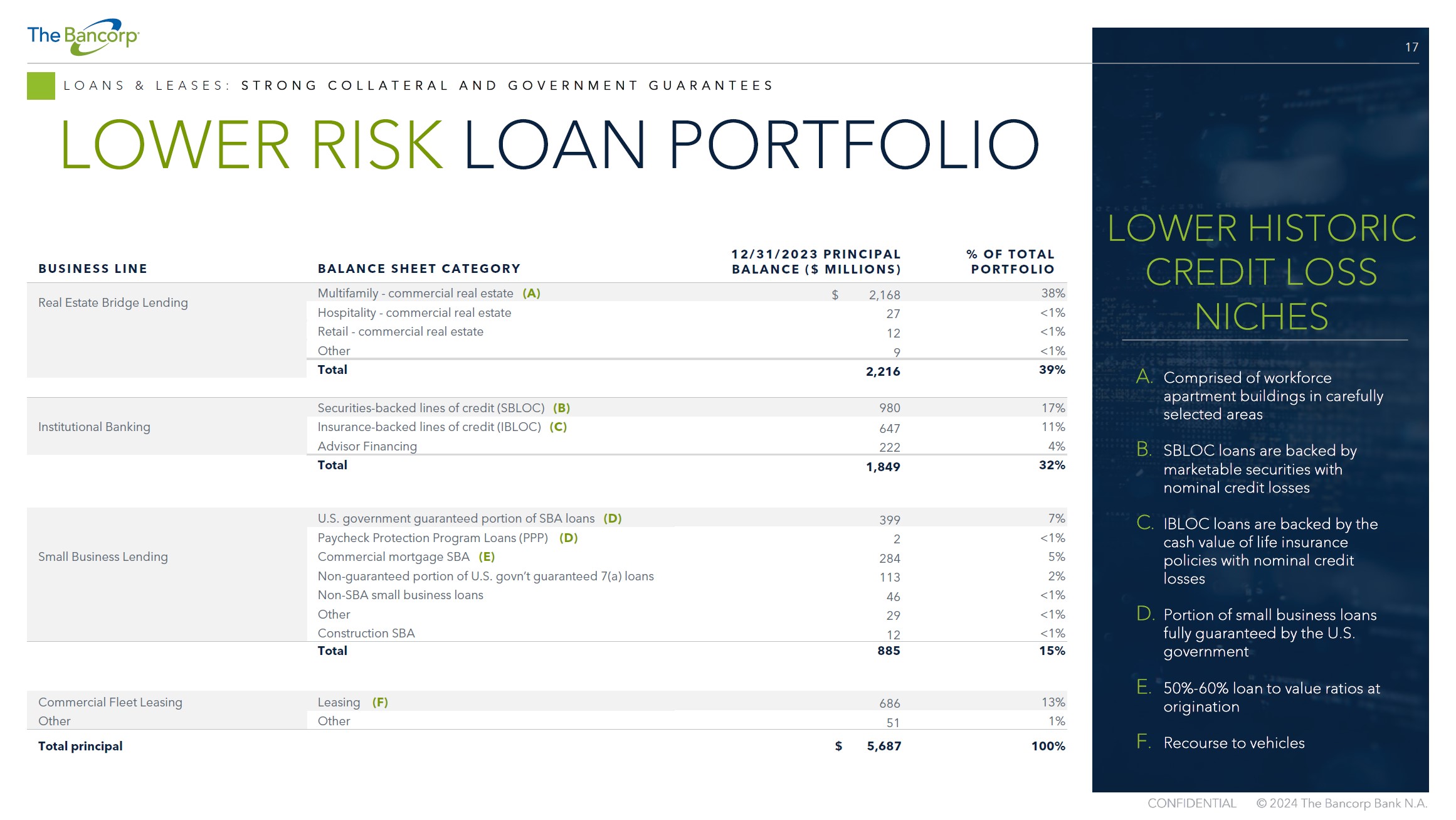

| Loan portfolio |

December 31, |

|

September 30, |

|

June 30, |

|

December 31, |

| |

2023 (unaudited) |

|

2023 (unaudited) |

|

2023 (unaudited) |

|

2022 |

| |

(Dollars in thousands) |

| |

|

|

|

|

|

|

|

|

|

|

|

| SBL non-real estate |

$ |

137,752 |

|

$ |

130,579 |

|

$ |

117,621 |

|

$ |

108,954 |

| SBL commercial mortgage |

|

606,986 |

|

|

547,107 |

|

|

515,008 |

|

|

474,496 |

| SBL construction |

|

22,627 |

|

|

19,204 |

|

|

32,471 |

|

|

30,864 |

| Small business loans |

|

767,365 |

|

|

696,890 |

|

|

665,100 |

|

|

614,314 |

| Direct lease financing |

|

685,657 |

|

|

670,208 |

|

|

657,316 |

|

|

632,160 |

| SBLOC / IBLOC(1) |

|

1,627,285 |

|

|

1,720,513 |

|

|

1,883,607 |

|

|

2,332,469 |

| Advisor financing(2) |

|

221,612 |

|

|

199,442 |

|

|

173,376 |

|

|

172,468 |

| Real estate bridge loans |

|

1,999,782 |

|

|

1,848,224 |

|

|

1,826,227 |

|

|

1,669,031 |

| Other loans(3) |

|

50,638 |

|

|

55,800 |

|

|

55,644 |

|

|

61,679 |

| |

|

5,352,339 |

|

|

5,191,077 |

|

|

5,261,270 |

|

|

5,482,121 |

| Unamortized loan fees and costs |

|

8,800 |

|

|

7,895 |

|

|

6,304 |

|

|

4,732 |

| Total loans, including unamortized fees and costs |

$ |

5,361,139 |

|

$ |

5,198,972 |

|

$ |

5,267,574 |

|

$ |

5,486,853 |

| Small business portfolio |

December 31, |

|

September 30, |

|

June 30, |

|

December 31, |

| |

2023 (unaudited) |

|

2023 (unaudited) |

|

2023 (unaudited) |

|

2022 |

| |

|

(Dollars in thousands) |

| |

|

|

|

|

|

|

|

|

|

|

|

| SBL, including unamortized fees and costs |

$ |

776,867 |

|

$ |

705,790 |

|

$ |

673,667 |

|

$ |

621,641 |

| SBL, included in loans, at fair value |

|

119,287 |

|

|

126,543 |

|

|

134,131 |

|

|

146,717 |

| Total small business loans(4) |

$ |

896,154 |

|

$ |

832,333 |

|

$ |

807,798 |

|

$ |

768,358 |

(1) SBLOC

are collateralized by marketable securities, while IBLOC are collateralized by the cash surrender value of insurance policies. At December

31, 2023 and December 31, 2022, IBLOC loans amounted to $646.9 million and $1.12 billion, respectively.

(2) In

2020 The Bancorp began originating loans to investment advisors for purposes of debt refinancing, acquisition of another firm or internal

succession. Maximum loan amounts are subject to loan-to-value (“LTV”) ratios of 70% of the business enterprise value based

on a third-party valuation, but may be increased depending upon the debt service coverage ratio. Personal guarantees and blanket

business liens are obtained as appropriate.

(3) Includes

demand deposit overdrafts reclassified as loan balances totaling $1.7 million and $2.6 million at December 31, 2023 and December 31, 2022,

respectively. Estimated overdraft charge-offs and recoveries are reflected in the allowance for credit losses and are immaterial.

(4) The

SBLs held at fair value are comprised of the government guaranteed portion of 7(a) Program loans at the dates indicated.

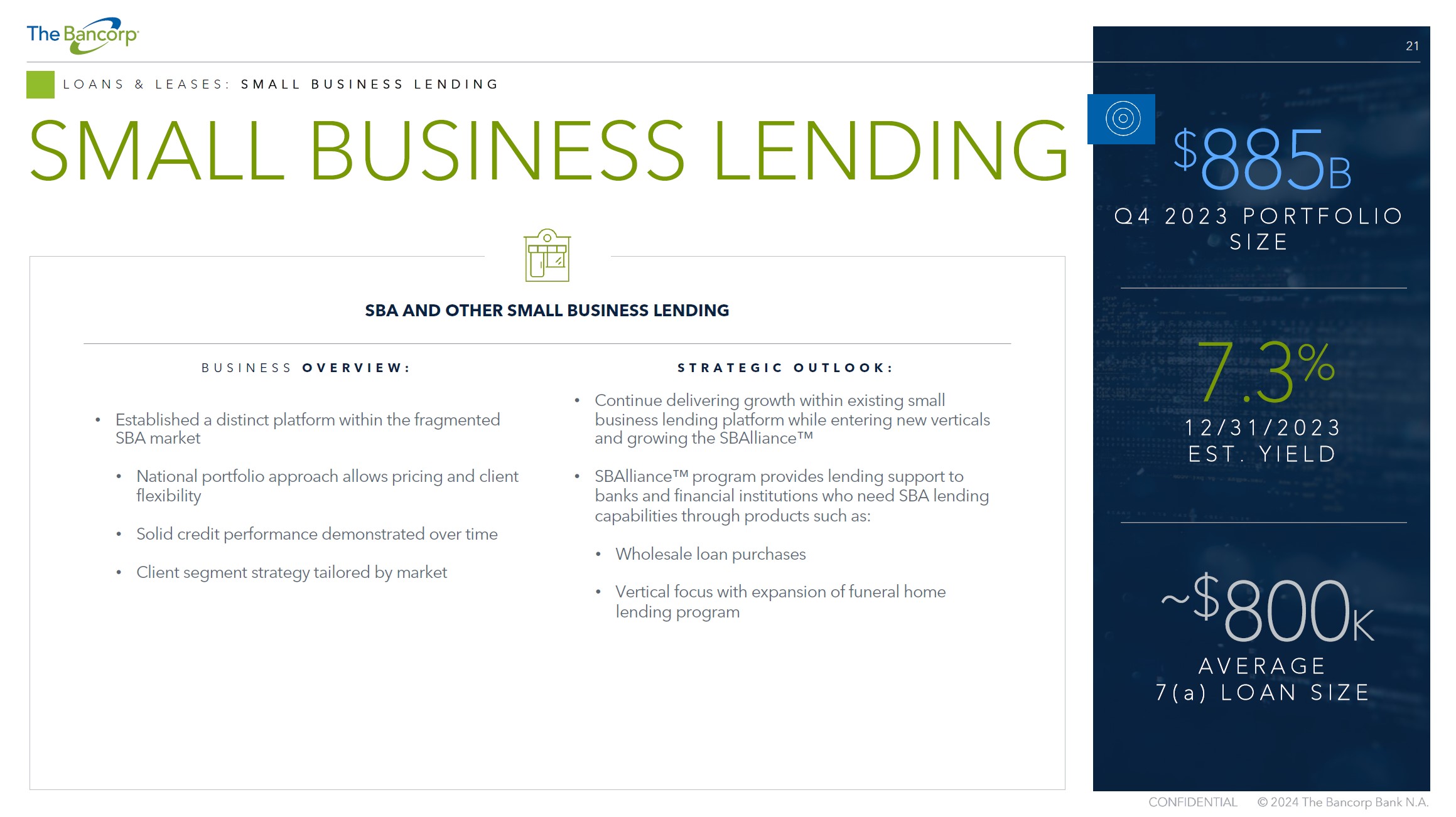

Small business loans as of December 31, 2023

| |

|

Loan principal |

| |

|

(Dollars in millions) |

| U.S. government guaranteed portion of SBA loans(1) |

|

$ |

399 |

| PPP loans(1) |

|

|

2 |

| Commercial mortgage SBA(2) |

|

|

284 |

| Construction SBA(3) |

|

|

12 |

| Non-guaranteed portion of U.S. government guaranteed 7(a) Program loans(4) |

|

|

113 |

| Non-SBA SBLs |

|

|

46 |

| Other(5) |

|

|

29 |

| Total principal |

|

$ |

885 |

| Unamortized fees and costs |

|

|

11 |

| Total SBLs |

|

$ |

896 |

(1) Includes

the portion of SBA 7(a) Program loans and PPP loans which have been guaranteed by the U.S. government, and therefore are assumed to have

no credit risk.

(2) Substantially

all these loans are made under the 504 Program, which dictates origination date LTV percentages, generally 50-60%, to which The Bancorp

adheres.

(3) Includes

$4.0 million in 504 Program first mortgages with an origination date LTV of 50-60%, and $8.0 million in SBA interim loans with an approved

SBA post-construction full takeout/payoff.

(4) Includes

the unguaranteed portion of 7(a) Program loans which are 70% or more guaranteed by the U.S. government. SBA 7(a) Program loans are not

made on the basis of real estate LTV; however, they are subject to SBA's "All Available Collateral" rule which mandates that

to the extent a borrower or its 20% or greater principals have available collateral (including personal residences), the collateral must

be pledged to fully collateralize the loan, after applying SBA-determined liquidation rates. In addition, all 7(a) Program loans and 504

Program loans require the personal guaranty of all 20% or greater owners.

(5) Comprised of $29.0 million of loans sold that do not qualify

for true sale accounting.

Small business loans by type as of December 31, 2023

(Excludes government guaranteed portion of SBA 7(a) Program and PPP loans)

| |

|

SBL commercial mortgage(1) |

|

SBL construction(1) |

|

SBL non-real estate |

|

Total |

|

|

% Total |

| |

|

|

(Dollars in millions) |

| Hotels and motels |

|

$ |

77 |

|

$ |

— |

|

$ |

— |

|

$ |

77 |

|

|

17% |

| Funeral homes and funeral services |

|

|

41 |

|

|

— |

|

|

— |

|

|

41 |

|

|

9% |

| Full-service restaurants |

|

|

24 |

|

|

6 |

|

|

2 |

|

|

32 |

|

|

7% |

| Car washes |

|

|

19 |

|

|

— |

|

|

— |

|

|

19 |

|

|

4% |

| Child day care services |

|

|

16 |

|

|

2 |

|

|

2 |

|

|

20 |

|

|

4% |

| Outpatient mental health and substance abuse centers |

|

|

15 |

|

|

— |

|

|

— |

|

|

15 |

|

|

3% |

| Homes for the elderly |

|

|

13 |

|

|

— |

|

|

— |

|

|

13 |

|

|

3% |

| Gasoline stations with convenience stores |

|

|

12 |

|

|

— |

|

|

— |

|

|

12 |

|

|

3% |

| Fitness and recreational sports centers |

|

|

8 |

|

|

— |

|

|

2 |

|

|

10 |

|

|

2% |

| Lessors of other real estate property |

|

|

9 |

|

|

— |

|

|

1 |

|

|

10 |

|

|

2% |

| Offices of lawyers |

|

|

9 |

|

|

— |

|

|

— |

|

|

9 |

|

|

2% |

| Limited-service restaurants |

|

|

3 |

|

|

1 |

|

|

3 |

|

|

7 |

|

|

2% |

| Caterers |

|

|

7 |

|

|

— |

|

|

— |

|

|

7 |

|

|

2% |

| General warehousing and storage |

|

|

7 |

|

|

— |

|

|

— |

|

|

7 |

|

|

2% |

| Lessors of nonresidential buildings |

|

|

6 |

|

|

— |

|

|

— |

|

|

6 |

|

|

1% |

| Plumbing, heating, and air-conditioning |

|

|

6 |

|

|

— |

|

|

1 |

|

|

7 |

|

|

2% |

| All other specialty trade contractors |

|

|

5 |

|

|

— |

|

|

— |

|

|

5 |

|

|

1% |

| Lessors of residential buildings |

|

|

5 |

|

|

— |

|

|

— |

|

|

5 |

|

|

1% |

| Miscellaneous durable goods merchants |

|

|

5 |

|

|

— |

|

|

— |

|

|

5 |

|

|

1% |

| Packaged frozen food merchant wholesalers |

|

|

5 |

|

|

— |

|

|

— |

|

|

5 |

|

|

1% |

| Technical and trade schools |

|

|

5 |

|

|

— |

|

|

— |

|

|

5 |

|

|

1% |

| Amusement and recreation |

|

|

4 |

|

|

— |

|

|

— |

|

|

4 |

|

|

1% |

| Offices of dentists |

|

|

3 |

|

|

— |

|

|

— |

|

|

3 |

|

|

1% |

| Vocational rehabilitation services |

|

|

— |

|

|

3 |

|

|

— |

|

|

3 |

|

|

1% |

| Other(2) |

|

|

99 |

|

|

2 |

|

|

27 |

|

|

128 |

|

|

27% |

| Total |

|

$ |

403 |

|

$ |

14 |

|

$ |

38 |

|

$ |

455 |

|

|

100% |

(1) Of

the SBL commercial mortgage and SBL construction loans, $121.0 million represents the total of the non-guaranteed portion of SBA 7(a)

Program loans and non-SBA loans. The balance of those categories represents SBA 504 Program loans with 50%-60% origination date LTVs.

SBL Commercial excludes $29.0 million of loans sold that do not qualify for true sale accounting.

(2) Loan

types of less than $3.0 million are spread over approximately one hundred different business types.

State diversification as of December 31, 2023

(Excludes government guaranteed portion of SBA 7(a) Program loans and PPP

loans)

| |

|

SBL commercial mortgage(1) |

|

SBL construction(1) |

|

SBL non-real estate |

|

Total |

|

|

% Total |

| |

|

|

(Dollars in millions) |

| California |

|

$ |

82 |

|

$ |

5 |

|

$ |

3 |

|

$ |

90 |

|

|

20% |

| Florida |

|

|

68 |

|

|

1 |

|

|

3 |

|

|

72 |

|

|

16% |

| North Carolina |

|

|

38 |

|

|

1 |

|

|

2 |

|

|

41 |

|

|

9% |

| Pennsylvania |

|

|

34 |

|

|

— |

|

|

1 |

|

|

35 |

|

|

8% |

| New York |

|

|

25 |

|

|

2 |

|

|

2 |

|

|

29 |

|

|

6% |

| New Jersey |

|

|

17 |

|

|

3 |

|

|

4 |

|

|

24 |

|

|

5% |

| Texas |

|

|

18 |

|

|

— |

|

|

6 |

|

|

24 |

|

|

5% |

| Georgia |

|

|

20 |

|

|

1 |

|

|

2 |

|

|

23 |

|

|

5% |

| Other States |

|

|

101 |

|

|

1 |

|

|

15 |

|

|

117 |

|

|

26% |

| Total |

|

$ |

403 |

|

$ |

14 |

|

$ |

38 |

|

$ |

455 |

|

|

100% |

(1) Of the SBL commercial

mortgage and SBL construction loans, $121.0 million represents the total of the non-guaranteed

portion of SBA 7(a) Program loans and non-SBA loans. The balance of those categories represents SBA 504 Program loans with 50%-60% origination

date LTVs. SBL Commercial excludes $29.0 million of loans that do not qualify for true sale accounting.

Top 10 loans as of December 31, 2023

| Type(1) |

|

State |

|

SBL commercial mortgage |

|

| |

|

(Dollars in millions) |

| Funeral homes and funeral services |

|

|

PA |

|

$ |

13 |

|

| Mental health and substance abuse center |

|

|

FL |

|

|

10 |

|

| Funeral homes and funeral services |

|

|

ME |

|

|

9 |

|

| Hotel |

|

|

FL |

|

|

8 |

|

| Lawyers office |

|

|

CA |

|

|

8 |

|

| Hotel |

|

|

NC |

|

|

7 |

|

| General warehousing and storage |

|

|

PA |

|

|

7 |

|

| Hotel |

|

|

FL |

|

|

6 |

|

| Hotel |

|

|

NY |

|

|

6 |

|

| Hotel |

|

|

NC |

|

|

5 |

|

| Total |

|

|

|

|

$ |

79 |

|

(1) The table above does

not include loans to the extent that they are U.S. government guaranteed.

Commercial real estate loans, excluding SBA loans, are as follows including

LTV at origination:

Type as of December 31, 2023

| Type |

|

|

# Loans |

|

Balance |

|

Weighted average origination date LTV |

|

Weighted average interest rate |

| |

|

|

(Dollars in millions) |

| Real estate bridge loans (multi-family apartment loans recorded at amortized cost)(1) |

|

|

148 |

|

$ |

2,000 |

|

71% |

|

9.30% |

| |

|

|

|

|

|

|

|

|

|

|

| Non-SBA commercial real estate loans, at fair value: |

|

|

|

|

|

|

|

|

|

|

| Multi-family (apartment bridge loans)(1) |

|

|

9 |

|

$ |

168 |

|

77% |

|

8.82% |

| Hospitality (hotels and lodging) |

|

|

2 |

|

|

27 |

|

65% |

|

9.82% |

| Retail |

|

|

2 |

|

|

12 |

|

72% |

|

8.19% |

| Other |

|

|

2 |

|

|

9 |

|

73% |

|

4.97% |

| |

|

|

15 |

|

|

216 |

|

75% |

|

8.74% |

| Fair value adjustment |

|

|

|

|

|

(3) |

|

|

|

|

| Total non-SBA commercial real estate loans, at fair value |

|

|

|

|

|

213 |

|

|

|

|

| Total commercial real estate loans |

|

|

|

|

$ |

2,213 |

|

72% |

|

9.26% |

(1) In the third quarter

of 2021, we resumed the origination of multi-family apartment loans. These are similar to the multi-family apartment loans carried at

fair value, but at origination are intended to be held on the balance sheet, so they are not accounted for at fair value.

| State diversification as of December 31, 2023 |

|

|

15 largest loans as of December 31, 2023 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| State |

|

|

Balance |

|

|

Origination date LTV |

|

|

State |

|

|

|

Balance |

|

Origination date LTV |

| (Dollars in millions) |

|

|

(Dollars in millions) |

| Texas |

|

$ |

814 |

|

|

72% |

|

|

Texas |

|

|

$ |

46 |

|

75% |

| Georgia |

|

|

247 |

|

|

69% |

|

|

Texas |

|

|

|

44 |

|

72% |

| Florida |

|

|

221 |

|

|

70% |

|

|

Tennessee |

|

|

|

40 |

|

72% |

| Michigan |

|

|

112 |

|

|

69% |

|

|

Texas |

|

|

|

39 |

|

75% |

| Indiana |

|

|

92 |

|

|

73% |

|

|

Texas |

|

|

|

39 |

|

79% |

| New Jersey |

|

|

78 |

|

|

69% |

|

|

Texas |

|

|

|

37 |

|

80% |

| Ohio |

|

|

73 |

|

|

67% |

|

|

Michigan |

|

|

|

37 |

|

62% |

| Other States each <$63 million |

|

|

576 |

|

|

73% |

|

|

Texas |

|

|

|

36 |

|

67% |

| Total |

|

$ |

2,213 |

|

|

72% |

|

|

Florida |

|

|

|

35 |

|

72% |

| |

|

|

|

|

|

|

|

|

Indiana |

|

|

|

34 |

|

76% |

| |

|

|

|

|

|

|

|

|

Texas |

|

|

|

34 |

|

62% |

| |

|

|

|

|

|

|

|

|

Michigan |

|

|

|

32 |

|

79% |

| |

|

|

|

|

|

|

|

|

Oklahoma |

|

|

|

31 |

|

78% |

| |

|

|

|

|

|

|

|

|

New Jersey |

|

|

|

30 |

|

62% |

| |

|

|

|

|

|

|

|

|

Georgia |

|

|

|

29 |

|

69% |

| |

|

|

|

|

|

|

|

|

15 largest commercial real estate loans |

|

|

$ |

543 |

|

72% |

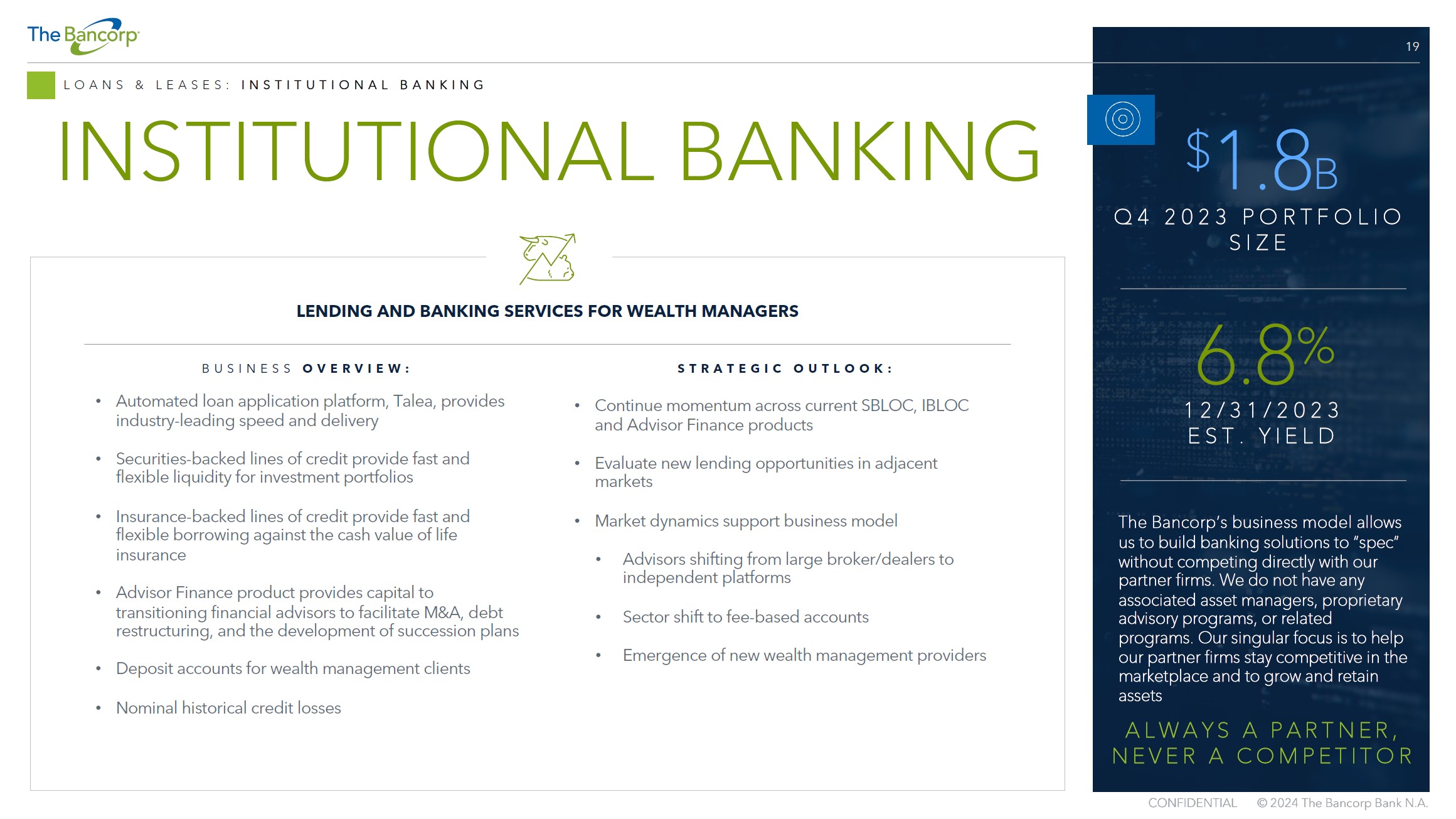

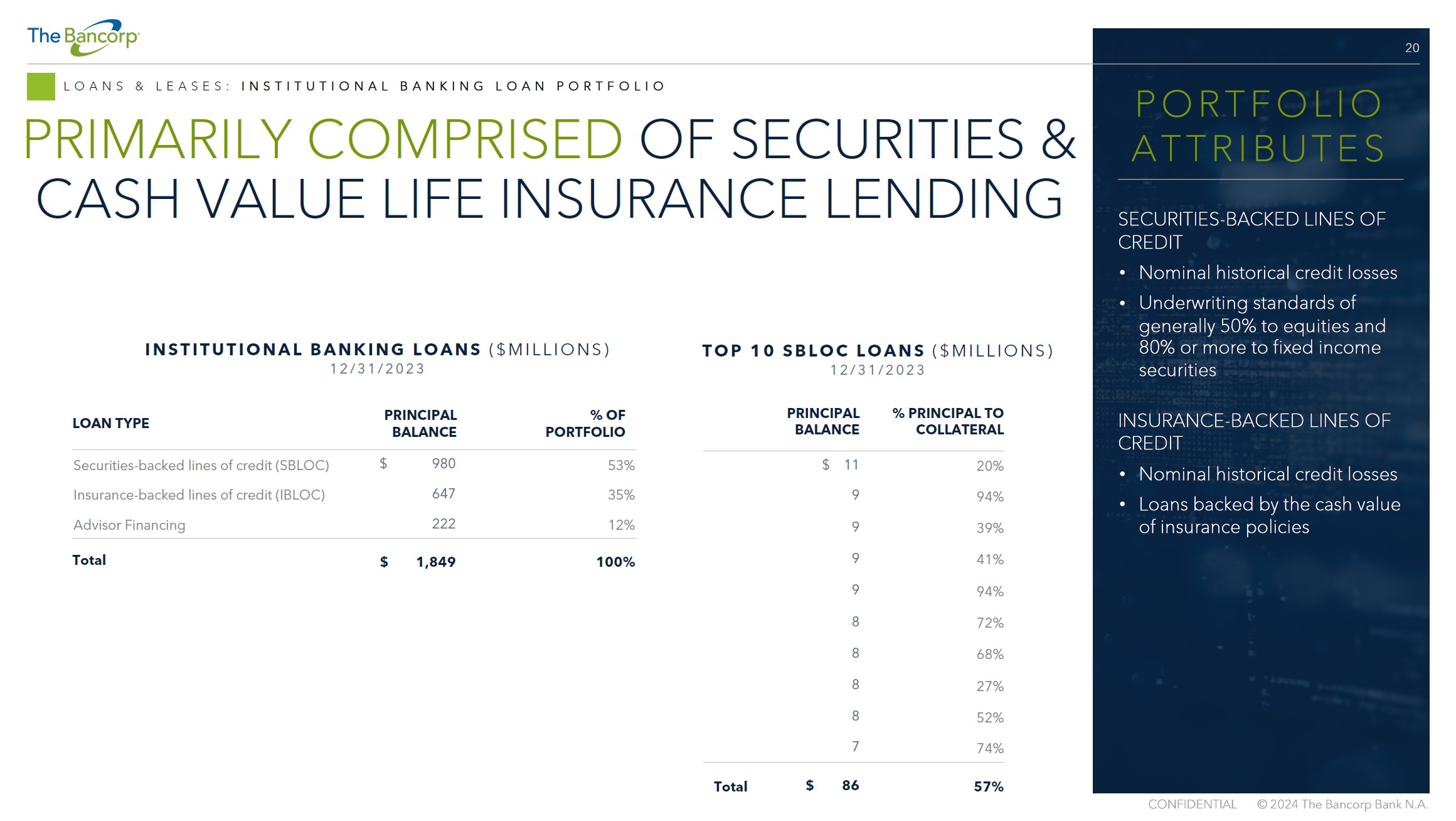

Institutional banking loans outstanding at December 31, 2023

| Type |

Principal |

|

% of total |

| |

|

(Dollars in millions) |

|

|

| SBLOC |

$ |

980 |

|

53% |

| IBLOC |

|

647 |

|

35% |

| Advisor financing |

|

222 |

|

12% |

| Total |

$ |

1,849 |

|

100% |

For SBLOC, we generally lend up to 50% of the value of equities and 80%

for investment grade securities. While the value of equities has fallen in excess of 30% in recent years, the reduction in collateral

value of brokerage accounts collateralizing SBLOCs generally has been less, for two reasons. First, many collateral accounts are “balanced”

and accordingly have a component of debt securities, which have either not decreased in value as much as equities, or in some cases may

have increased in value. Second, many of these accounts have the benefit of professional investment advisors who provided some protection

against market downturns, through diversification and other means. Additionally, borrowers often utilize only a portion of collateral

value, which lowers the percentage of principal to collateral.

Top 10 SBLOC loans at December 31, 2023

| |

Principal amount |

|

% Principal to collateral |

| |

(Dollars in millions) |

| |

$ |

11 |

|

20% |

| |

|

9 |

|

94% |

| |

|

9 |

|

39% |

| |

|

9 |

|

41% |

| |

|

9 |

|

94% |

| |

|

8 |

|

72% |

| |

|

8 |

|

68% |

| |

|

8 |

|

27% |

| |

|

8 |

|

52% |

| |

|

7 |

|

74% |

| Total and weighted average |

$ |

86 |

|

57% |

Insurance backed lines of credit (IBLOC)

IBLOC loans are backed by the cash value of eligible life insurance policies

which have been assigned to us. We generally lend up to 95% of such cash value. Our underwriting standards require approval of the

insurance companies which carry the policies backing these loans. Currently, fifteen insurance companies have been approved and, as of

December 31, 2023, all were rated A- (Excellent) or better by AM BEST.

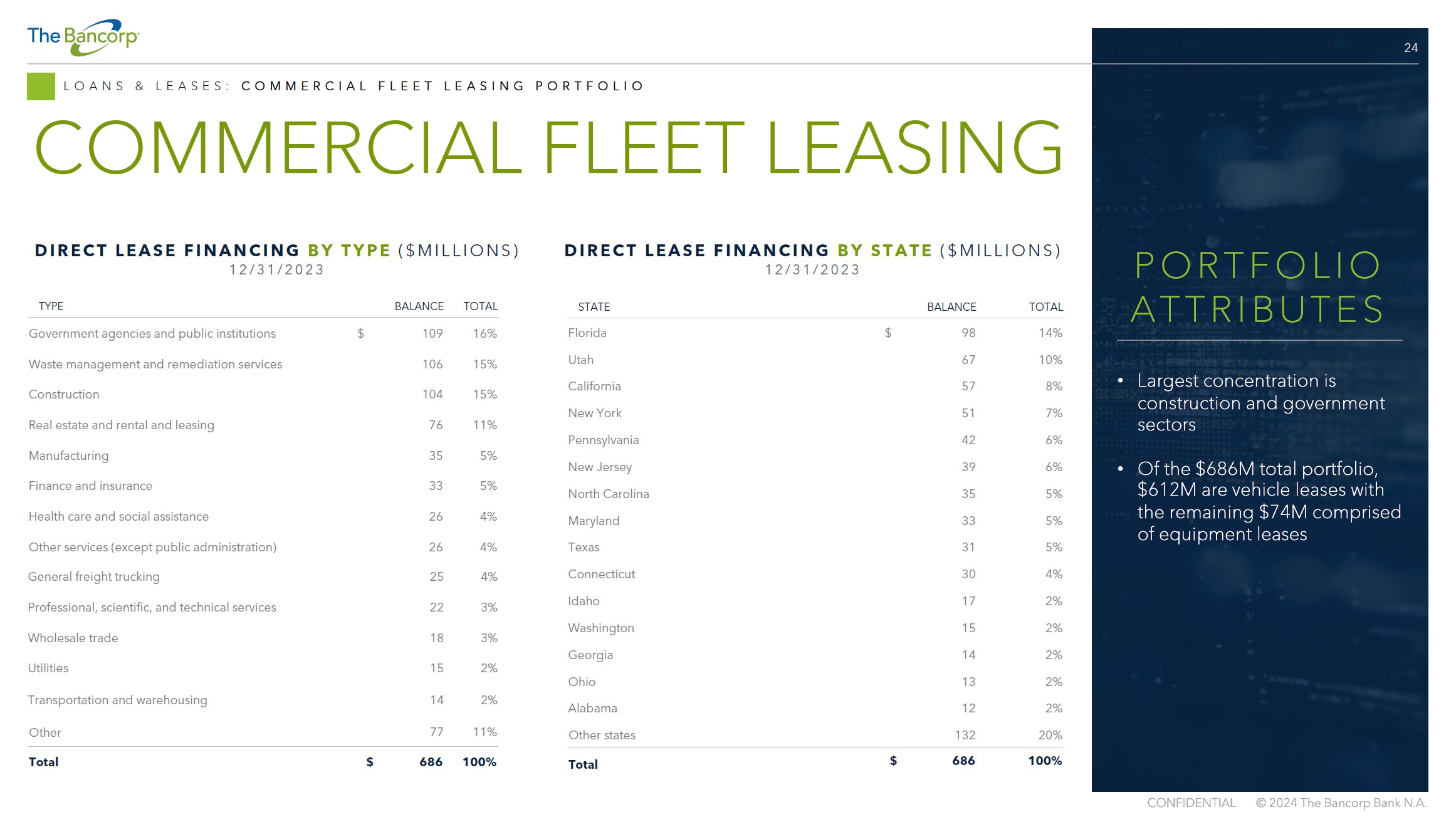

Direct lease financing by type as of December 31, 2023

| |

Principal balance(1) |

|

% Total |

| |

(Dollars in millions) |

|

|

| Government agencies and public institutions(2) |

$ |

109 |

|

16% |

| Waste management and remediation services |

|

106 |

|

15% |

| Construction |

|

104 |

|

15% |

| Real estate and rental and leasing |

|

76 |

|

11% |

| Manufacturing |

|

35 |

|

5% |

| Finance and insurance |

|

33 |

|

5% |

| Health care and social assistance |

|

26 |

|

4% |

| Other services (except public administration) |

|

26 |

|

4% |

| General freight trucking |

|

25 |

|

4% |

| Professional, scientific, and technical services |

|

22 |

|

3% |

| Wholesale trade |

|

18 |

|

3% |

| Utilities |

|

15 |

|

2% |

| Transportation and warehousing |

|

14 |

|

2% |

| Other |

|

77 |

|

11% |

| Total |

$ |

686 |

|

100% |

(1) Of

the total $686.0 million of direct lease financing, $611.0 million consisted of vehicle leases with the remaining balance consisting of

equipment leases.

(2) Includes

public universities and school districts.

Direct lease financing by state as of December 31, 2023

| State |

Principal balance |

|

% Total |

| |

(Dollars in millions) |

|

|

| Florida |

$ |

98 |

|

14% |

| Utah |

|

67 |

|

10% |

| California |

|

57 |

|

8% |

| New York |

|

51 |

|

7% |

| Pennsylvania |

|

42 |

|

6% |

| New Jersey |

|

39 |

|

6% |

| North Carolina |

|

35 |

|

5% |

| Maryland |

|

33 |

|

5% |

| Texas |

|

31 |

|

5% |

| Connecticut |

|

30 |

|

4% |

| Idaho |

|

17 |

|

2% |

| Washington |

|

15 |

|

2% |

| Georgia |

|

14 |

|

2% |

| Ohio |

|

13 |

|

2% |

| Alabama |

|

12 |

|

2% |

| Other States |

|

132 |

|

20% |

| Total |

$ |

686 |

|

100% |

| Capital ratios | |

Tier 1 capital to average | |

Tier 1 capital to risk-weighted | |

Total capital to risk-weighted | |

Common equity tier 1 to risk |

| | |

assets

ratio | |

assets

ratio | |

assets

ratio | |

weighted

assets |

| As of December 31, 2023 | |

| | | |

| | | |

| | | |

| | |

| The Bancorp, Inc. | |

| 11.19% | | |

| 15.66% | | |

| 16.23% | | |

| 15.66% | |

| The Bancorp Bank, National Association | |

| 12.37% | | |

| 17.35% | | |

| 17.92% | | |

| 17.35% | |

| "Well capitalized" institution (under federal regulations-Basel III) | |

| 5.00% | | |

| 8.00% | | |

| 10.00% | | |

| 6.50% | |

| | |

| | | |

| | | |

| | | |

| | |

| As of December 31, 2022 | |

| | | |

| | | |

| | | |

| | |

| The Bancorp, Inc. | |

| 9.63% | | |

| 13.40% | | |

| 13.87% | | |

| 13.40% | |

| The Bancorp Bank, National Association | |

| 10.73% | | |

| 14.95% | | |

| 15.42% | | |

| 14.95% | |

| "Well capitalized" institution (under federal regulations-Basel III) | |

| 5.00% | | |

| 8.00% | | |

| 10.00% | | |

| 6.50% | |

| | |

| |

|

| | |

Three months ended | |

Year ended |

| | |

December 31, | |

December 31, |

| | |

2023 | |

2022 | |

2023 | |

2022 |

| Selected operating ratios | |

| | | |

| | | |

| | | |

| | |

| Return on average assets(1) | |

| 2.38% | | |

| 2.13% | | |

| 2.59% | | |

| 1.81% | |

| Return on average equity(1) | |

| 22.10% | | |

| 23.52% | | |

| 25.62% | | |

| 19.34% | |

| Net interest margin | |

| 5.26% | | |

| 4.21% | | |

| 4.95% | | |

| 3.55% | |

(1)Annualized

| Book value per share table |

December 31, |

|

September 30, |

|

June 30, |

|

December 31, |

| |

2023 |

|

2023 |

|

2023 |

|

2022 |

| Book value per share |

$ |

15.17 |

|

$ |

14.36 |

|

$ |

13.74 |

|

$ |

12.46 |

| |

|

|

|

|

|

|

|

|

|

|

|

| Loan quality table | |

December 31, | |

September 30, | |

June 30, | |

December 31, |

| | |

2023 | |

2023 | |

2023 | |

2022 |

| | |

(Dollars in thousands) |

| Nonperforming loans to total loans | |

| 0.25% | | |

| 0.30% | | |

| 0.28% | | |

| 0.33% | |

| Nonperforming assets to total assets | |

| 0.39% | | |

| 0.46% | | |

| 0.47% | | |

| 0.50% | |

| Allowance for credit losses to total loans | |

| 0.51% | | |

| 0.46% | | |

| 0.44% | | |

| 0.41% | |

| | |

| | | |

| | | |

| | | |

| | |

| Nonaccrual loans | |

$ | 11,525 | | |

$ | 15,100 | | |

$ | 14,027 | | |

$ | 10,356 | |

| Loans 90 days past due still accruing interest | |

| 1,744 | | |

| 677 | | |

| 563 | | |

| 7,775 | |

| Other real estate owned | |

| 16,949 | | |

| 18,756 | | |

| 20,952 | | |

| 21,210 | |

| Total nonperforming assets | |

$ | 30,218 | | |

$ | 34,533 | | |

$ | 35,542 | | |

$ | 39,341 | |

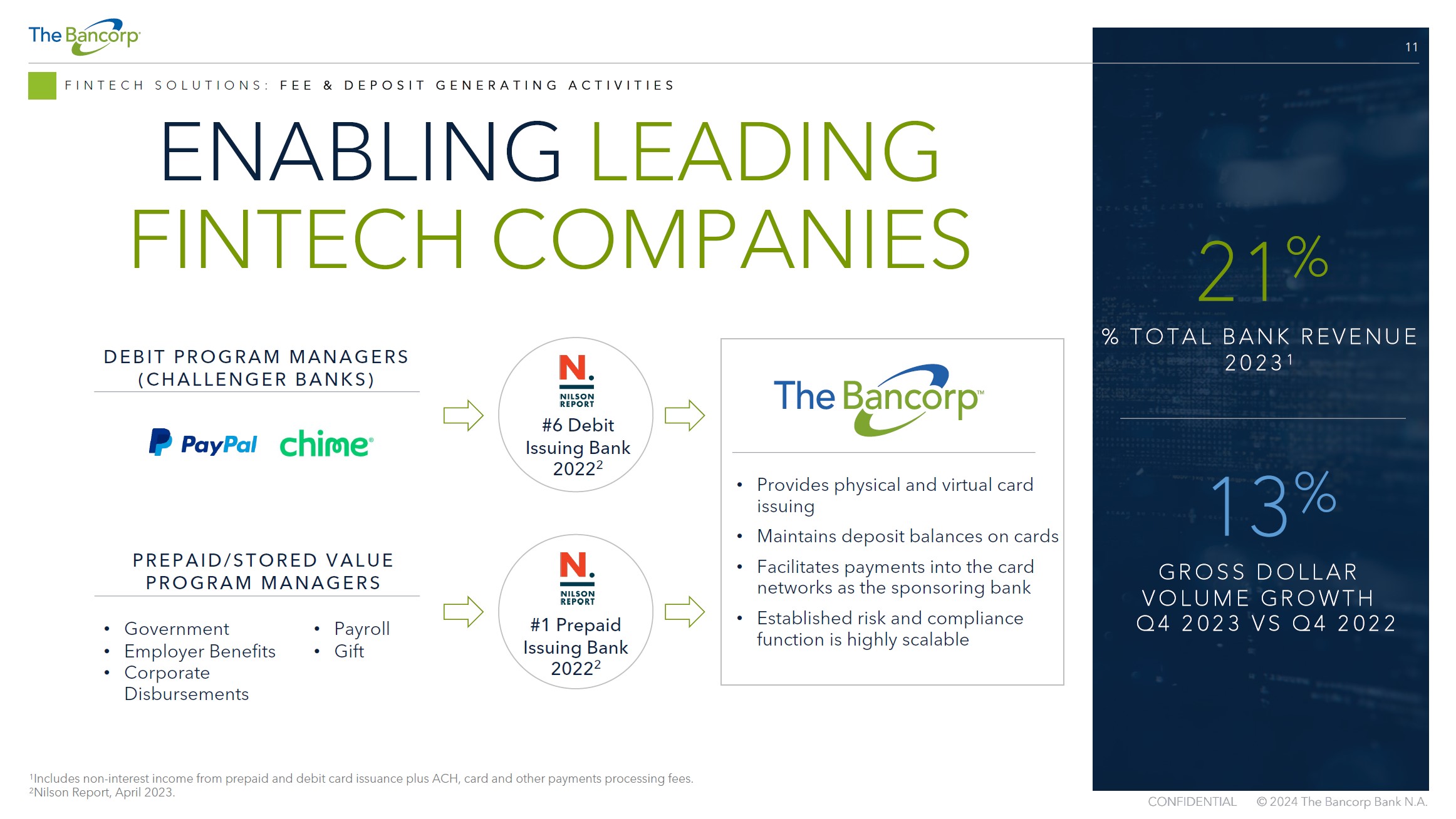

| Gross dollar volume (GDV) (1) | |

Three months ended |

| | |

December 31, | |

September 30, | |

June 30, | |

December 31, |

| | |

2023 | |

2023 | |

2023 | |

2022 |

| | |

(Dollars in thousands) |

| Prepaid and debit card GDV | |

$ | 33,292,350 | | |

$ | 32,972,249 | | |

$ | 32,776,154 | | |

$ | 29,454,074 | |

| | |

| | | |

| | | |

| | | |

| | |

(1) Gross dollar volume represents the total dollar amount

spent on prepaid and debit cards issued by The Bancorp Bank, N.A.

| Business line quarterly summary |

|

| Quarter ended December 31, 2023 |

|

| (Dollars in millions) |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Balances |

|

|

|

|

|

| |

|

|

|

|

|

% Growth |

|

|

|

|

|

| Major business lines |

|

Average approximate rates(1) |

|

Balances(2) |

|

Year over year |

|

Linked quarter annualized |

|

|

|

|

|

| Loans |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Institutional banking(3) |

|

6.8% |

|

$ 1,849 |

|

(26%) |

|

(15%) |

|

|

|

|

|

| Small business lending(4) |

|

7.3% |

|

896 |

|

13% |

|

17% |

|

|

|

|

|

| Leasing |

|

7.4% |

|

686 |

|

8% |

|

9% |

|

|

|

|

|

| Commercial real estate (non-SBA loans, at fair value) |

|

8.7% |

|

216 |

|

nm |

|

nm |

|

|

|

|

|

| Real estate bridge loans (recorded at book value) |

|

9.3% |

|

2,000 |

|

20% |

|

33% |

|

|

|

|

|

| Weighted average yield |

|

7.9% |

|

$ 5,647 |

|

|

|

|

|

Non-interest income |

| |

|

|

|

|

|

|

|

|

|

|

|

% Growth |

| Deposits: Fintech solutions group |

|

|

|

|

|

|

|

|

|

Current quarter |

|

Year over year |

|

| Prepaid and debit card issuance, and other payments |

2.5% |

|

$ 5,998 |

|

6% |

|

nm |

|

$ 25.1 |

|

15% |

|

(1) Average rates are for the three months ended December 31,

2023.

(2) Loan and deposit categories are based on period-end and

average quarterly balances, respectively.

(3) Institutional Banking loans are comprised of security backed

lines of credit (SBLOC), collateralized by marketable securities, insurance backed lines of credit (IBLOC), collateralized by the cash

surrender value of eligible life insurance policies, and investment advisor financing.

(4) Small Business Lending is substantially comprised of SBA

loans. Growth rates exclude $29.0 million of loans that do not qualify for true sale accounting.

Summary of credit lines available

Notwithstanding that the vast majority of The Bancorp’s funding is

comprised of insured and small balance accounts, The Bancorp maintains lines of credit exceeding potential liquidity requirements as follows.

The Bancorp also has access to other substantial sources of liquidity.

| |

December 31, 2023 |

| |

|

(Dollars in thousands) |

| Federal Reserve Bank |

$ |

1,947,513 |

| Federal Home Loan Bank |

|

731,500 |

| Total lines of credit available |

$ |

2,679,013 |

Estimated insured vs uninsured deposits

The vast majority of The Bancorp’s deposits are insured and low balance

and accordingly do not constitute the liquidity risk experienced by certain institutions. Accordingly the deposit base is comprised as

follows.

| |

December 31, 2023 |

| Insured |

|

91% |

| Low balance accounts |

|

5% |

| Other uninsured |

|

4% |

| Total deposits |

|

100% |

Calculation of efficiency ratio(1)

| |

Three months ended |

|

Year ended |

| |

December 31, |

|

December 31, |

|

December 31, |

|

December 31, |

| |

2023 |

|

2022 |

|

2023 |

|

2022 |

| |

(Dollars in thousands) |

| Net interest income |

$ |

92,159 |

|

$ |

76,760 |

|

$ |

354,052 |

|

$ |

248,841 |

| Non-interest income |

|

26,989 |

|

|

25,740 |

|

|

112,094 |

|

|

105,683 |

| Total revenue |

$ |

119,148 |

|

$ |

102,500 |

|

$ |

466,146 |

|

$ |

354,524 |

| Non-interest expense |

$ |

45,610 |

|

$ |

43,475 |

|

$ |

191,042 |

|

$ |

169,502 |

| |

|

|

|

|

|

|

|

|

|

|

|

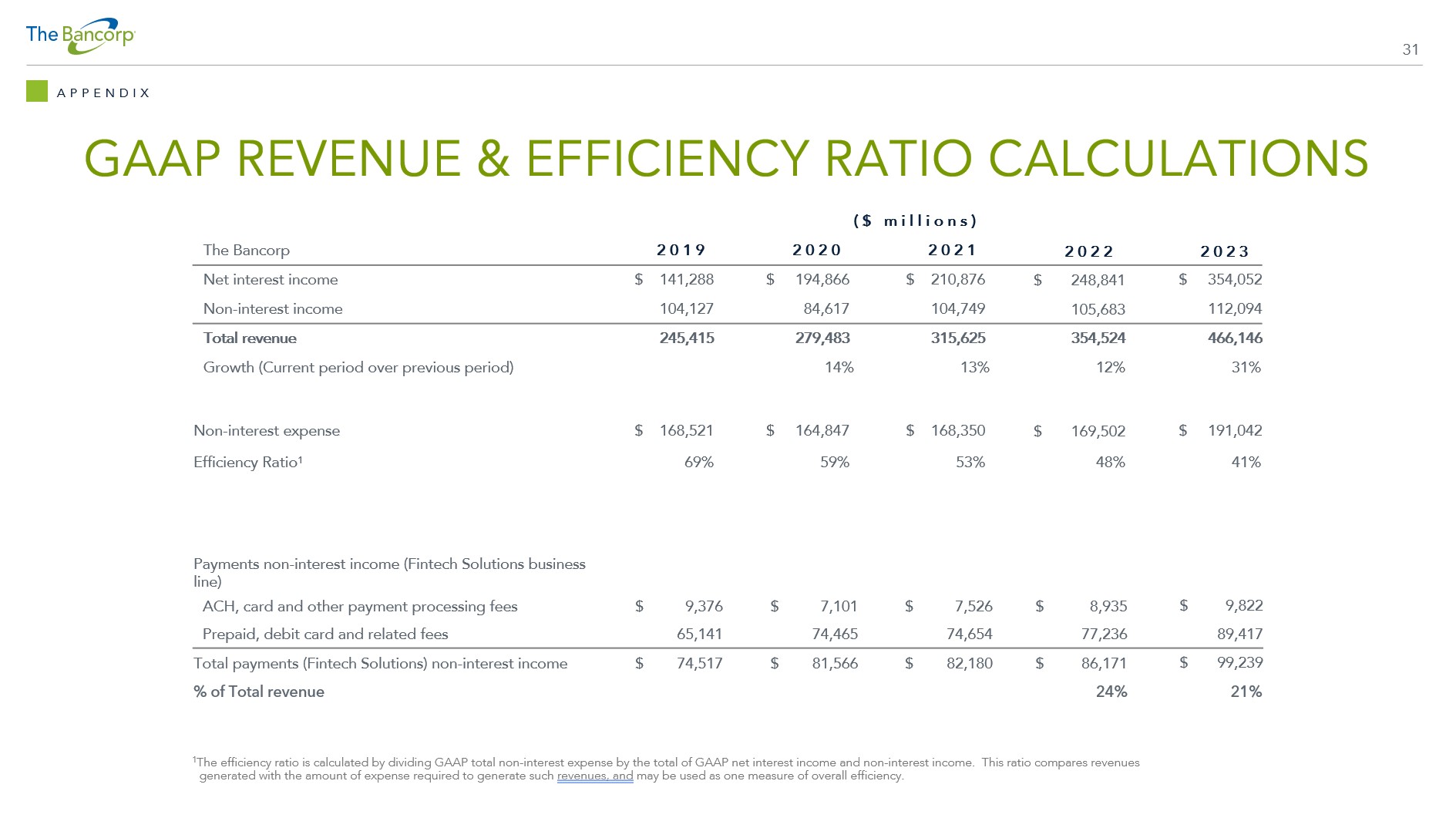

| Efficiency ratio |

|

38% |

|

|

42% |

|

|

41% |

|

|

48% |

(1) The efficiency ratio is calculated by dividing GAAP total

non-interest expense by the total of GAAP net interest income and non-interest income. This ratio compares revenues generated with

the amount of expense required to generate such revenues, and may be used as one measure of overall efficiency.

Exhibit 99.2

THE BANCORP INVESTOR PRESENTATION JANUARY 2024

2 DISCLOSURES Statements in this presentation regarding The Bancorp, Inc.’s (“The Bancorp”) business that are not historical facts or concern earnings guidance or the 2030 plan are “forward - looking statements”. These statements may be identified by the use of forward - looking terminology, including the words “may,” “believe,” “will,” “expect,” “anticipate,” “estimate,” “intend,” “plan," or similar words, and are based on current expectations about important business, economic, political, and technological factors, among others, and are subject to risks and uncertainties, which could cause the actual results, events or achievements to differ materially from those set forth in or implied by the forward - looking statements and related assumptions. 2024 guidance and long - term financial targets in this presentation assume achievement of management’s credit roadmap growth goals as described herein and other growth goals. If such assumptions are not met, guidance and long - term financial targets might not be reached. For further discussion of these risks and uncertainties, see the “risk factors” sections contained, in The Bancorp’s Annual Report on Form 10 - K for the year ended December 31, 2022 and in its other public filings with the SEC. In addition, these forward - looking statements are based upon assumptions with respect to future strategies and decisions that are subject to change. Annualized, pro forma, projected and estimated numbers are used for illustrative purposes only, are not forecasts and may not reflect actual results. The forward - looking statements speak only as of the date of this presentation. The Bancorp does not undertake to publicly revise or update forward - looking statements in this presentation to reflect events or circumstances that arise after the date of this presentation, except as may be required under applicable law. This presentation contains information regarding financial results that is calculated and presented on the basis of methodologies other than in accordance with accounting principles generally accepted in the United States (“GAAP”), such as those identified in the Appendix. As a result, such information may not conform to SEC Regulation S - X and may be adjusted and presented differently in filings with the SEC. Any non - GAAP financial measures used in this presentation are in addition to, and should not be considered superior to, or a substitute for, financial statements prepared in accordance with GAAP. Non - GAAP financial measures are subject to significant inherent limitations. The non - GAAP measures presented herein may not be comparable to similar non - GAAP measures presented by other companies. This information may be presented differently in future filings by The Bancorp with the SEC. This presentation may contain statistics and other data that in some cases has been obtained from or compiled from information made available by third - party service providers. The Bancorp makes no representation or warranty, express or implied, with respect to the accuracy, reasonableness or completeness of such information. Past performance is not indicative nor a guarantee of future results. Copies of the documents filed by The Bancorp with the SEC are available free of charge from the website of the SEC at www.sec.gov as well as on The Bancorp’s website at www.thebancorp.com . This presentation is for information purposes only and shall not constitute an offer to sell or the solicitation of an offer to buy any securities. Neither the SEC nor any other regulatory body has approved or disapproved of the securities of The Bancorp or passed upon the accuracy or adequacy of this presentation. Any representation to the contrary is a criminal offense. FORWARD LOOKING STATEMENTS & OTHER DISCLOSURES

3 FINANCIAL PERFORMANCE DELIVERING STRONG FINANCIAL PERFORMANCE 2023 2022 2021 2020 31% 12% 13% 14% REVENUE GROWTH 1 GROWTH 26% 19% 18% 15% ROE PROFITABILITY 2.6% 1.8% 1.7% 1.3% ROA 41% 48% 53% 59% EFFICIENCY RATIO 1 SCALABLE PLATFORM KEY FINANCIAL METRICS 1 Please see Appendix slide 31 for reconciliation of revenue growth over comparable prior year period and efficiency ratio Increasing levels of profitability Platform delivering operating leverage Capitalized on interest rate environment SUSTAINED PERFORMANCE The Bancorp is continuing to deliver high quality financial performance