SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 13E-3

RULE 13E-3 TRANSACTION STATEMENT UNDER SECTION

13(E)

OF THE SECURITIES ACT OF 1934

PowerSchool

Holdings, Inc.

(Name of the Issuer)

PowerSchool

Holdings, Inc.

Vista Equity Partners Fund VI, L.P.

Vista Equity Partners Fund VI-A, L.P.

VEPF VI FAF, L.P.

Severin Topco, LLC

VEP

Group, LLC

Robert F. Smith

Pinnacle Holdings I L.P.

Onex Partners IV Select LP

Onex US Principals LP

Onex Partners IV LP

Onex

Partners IV GP LP

Onex Partners IV PV LP

Onex Powerschool LP

OPH

B LP

Onex Partners Canadian GP Inc.

Onex American Holdings GP LLC

Onex Private Equity Holdings LLC

Onex Partners IV GP Ltd.

Onex Partners IV GP LLC

Onex Corporation

Gerald

W. Schwartz

(Names of Persons Filing Statement)

Class A Common Stock, par value $0.0001 per share

(Title of Class of Securities)

73939C106

(CUSIP Number

of Class of Securities)

|

|

|

|

|

| PowerSchool Holdings, Inc.

Hardeep Gulati Chief

Executive Officer 150 Parkshore Drive

Folsom, CA 95630 (877) 873-1550 |

|

Vista Equity Partners Fund VI, L.P.

Vista Equity Partners Fund VI-A, L.P.

VEPF VI FAF, L.P. Severin

Topco, LLC VEP Group, LLC

c/o Vista Equity Partners

4 Embarcadero Center, 20th Floor

San Francisco, CA 94111

(415) 765-6500

Robert F. Smith c/o Vista

Equity Partners 401 Congress Drive, Suite 3100

Austin, TX 78701 (512)

730-2400 |

|

Pinnacle Holdings I L.P.

Onex Partners IV Select LP

Onex US Principals LP

Onex Partners IV LP Onex

Partners IV GP LP Onex Partners IV PV LP

Onex Powerschool LP OPH B

LP Onex American Holdings GP LLC

Onex Private Equity Holdings LLC

Onex Partners IV GP LLC

712 Fifth Avenue, 40th Floor

New York, NY 10019 (212) 582-2211 Onex

Partners IV GP Ltd. Onex Partners Canadian GP Inc.

Onex Corporation Gerald

W. Schwartz 161 Bay Street, 49th Floor

Toronto, Ontario, Canada M5J 2S1

(416) 362-7711 |

(Name, Address, and Telephone Numbers of Person Authorized to Receive Notices and Communications on Behalf of

the Persons Filing Statement)

With copies to

|

|

|

| Damien R. Zoubek

Sanjay Murti Freshfields

Bruckhaus Deringer US LLP 175 Greenwich Street

New York, NY 10007 (212) 277-4000 |

|

Daniel Wolf, P.C.

David M. Klein, P.C.

Kirkland & Ellis LLP

601 Lexington Avenue New

York, NY 10022 (212) 446-4800 |

This statement is filed in connection with (check the appropriate box):

|

|

|

|

|

| a. |

|

☒ |

|

The filing of solicitation materials or an information statement subject to Regulation 14A, Regulation 14C or Rule 13e-3(c) under the Securities Exchange Act of 1934. |

|

|

|

| b. |

|

☐ |

|

The filing of a registration statement under the Securities Act of 1933. |

|

|

|

| c. |

|

☐ |

|

A tender offer. |

|

|

|

| d. |

|

☐ |

|

None of the above. |

Check the following box if the soliciting materials or information statement referred to in checking box

(a) are preliminary copies: ☒

Check the following box if the filing is a final amendment reporting the results of the

transaction: ☐

Neither the Securities and Exchange Commission nor any state securities commission has approved or

disapproved of this transaction, passed upon the merits or fairness of this transaction, or passed upon the adequacy or accuracy of the disclosure in this transaction statement on Schedule 13E-3. Any

representation to the contrary is a criminal offense.

INTRODUCTION

This Transaction Statement on Schedule 13E-3 (the “Transaction Statement”) is being

filed with the U.S. Securities and Exchange Commission (the “SEC”) pursuant to Section 13(e) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), jointly by the following persons (each, a “Filing

Person,” and collectively, the “Filing Persons”): (1) PowerSchool Holdings, Inc., a Delaware corporation (“PowerSchool” or the “Company”) and the issuer of the Class A common stock, par value $0.0001 per

share (the “Class A Common Stock”) that is the subject of the Rule 13e-3 transaction; (2) Vista Equity Partners Fund VI, L.P., a Cayman Islands exempted limited partnership (“VEPF

VI”); (3) Vista Equity Partners Fund VI-A, L.P., a Cayman Islands exempted limited partnership (“VEPF VI-A”); (4) VEPF VI FAF, L.P., a Cayman

Islands exempted limited partnership (“VEPF FAF”); (5) Severin Topco, LLC, a Delaware limited liability company (“Severin Topco”); (6) VEP Group, LLC, a Delaware limited liability company; (7) Robert F. Smith;

(8) Pinnacle Holdings I L.P., a Delaware limited partnership (“Pinnacle Holdings”); (9) Onex Partners IV Select LP, a Cayman Islands exempted limited partnership (“Onex Partners IV Select”); (10) Onex US Principals LP,

a Delaware limited partnership (“Onex US Principals”); (11) Onex Partners IV LP, a Cayman Islands exempted limited partnership (“Onex Partners IV”); (12) Onex Partners IV GP LP, a Cayman Islands exempted limited partnership

(“Onex Partners IV GP”); (13) Onex Partners IV PV LP, a Delaware limited partnership (“Onex Partners IV PV”); (14) Onex Powerschool LP, a Delaware limited partnership (“Onex Powerschool”); (15) OPH B LP; (16) Onex

Partners Canadian GP Inc., a corporation organized under the laws of the Province of Ontario; (17) Onex American Holdings GP LLC, a Delaware limited liability company; (18) Onex Private Equity Holdings LLC, a Delaware limited liability

company; (19) Onex Partners IV GP Ltd., a Cayman Islands exempted limited partnership; (20) Onex Partners IV GP LLC, a Delaware limited liability company; (21) Onex Corporation, a corporation organized under the laws of the Province

of Ontario; and (22) Gerald W. Schwartz.

This Transaction Statement relates to the Agreement and Plan of Merger, dated June 6,

2024 (including all exhibits and documents attached thereto, and as it may be amended from time to time, the “Merger Agreement”), by and among BCPE Polymath Buyer, Inc., a Delaware corporation (“Parent”), BCPE Polymath Merger

Sub, Inc., a Delaware corporation and a wholly owned subsidiary of Parent (“Merger Sub”), and PowerSchool. The Merger Agreement provides that, subject to the terms and conditions set forth in the Merger Agreement and the applicable

provisions of the General Corporation Law of the State of Delaware (the “DGCL”), Merger Sub will be merged with and into PowerSchool (the “Merger”), the separate corporate existence of Merger Sub will thereupon cease, and

PowerSchool will continue as the surviving corporation of the Merger and as a wholly owned subsidiary of Parent (the transactions contemplated by the Merger Agreement, including the Merger, collectively, the “Transactions”).

At the effective time of the Merger (the “Effective Time”), upon the terms and subject to the conditions set forth in the Merger

Agreement, by virtue of the Merger and without any action on the part of Parent, each issued and outstanding share of Class A Common Stock, other than (i) each share of common stock, par value $0.001 per share of Merger Sub that is issued

and outstanding as of immediately prior to the Effective Time will automatically be converted into one validly issued, fully paid and nonassessable share of common stock of the surviving corporation of the Merger; (ii) each share of

Class A Common Stock that is issued and outstanding as of immediately prior to the Effective Time (other than Owned Company Shares (including Rollover Shares) or Dissenting Company Shares) will be automatically cancelled, extinguished and

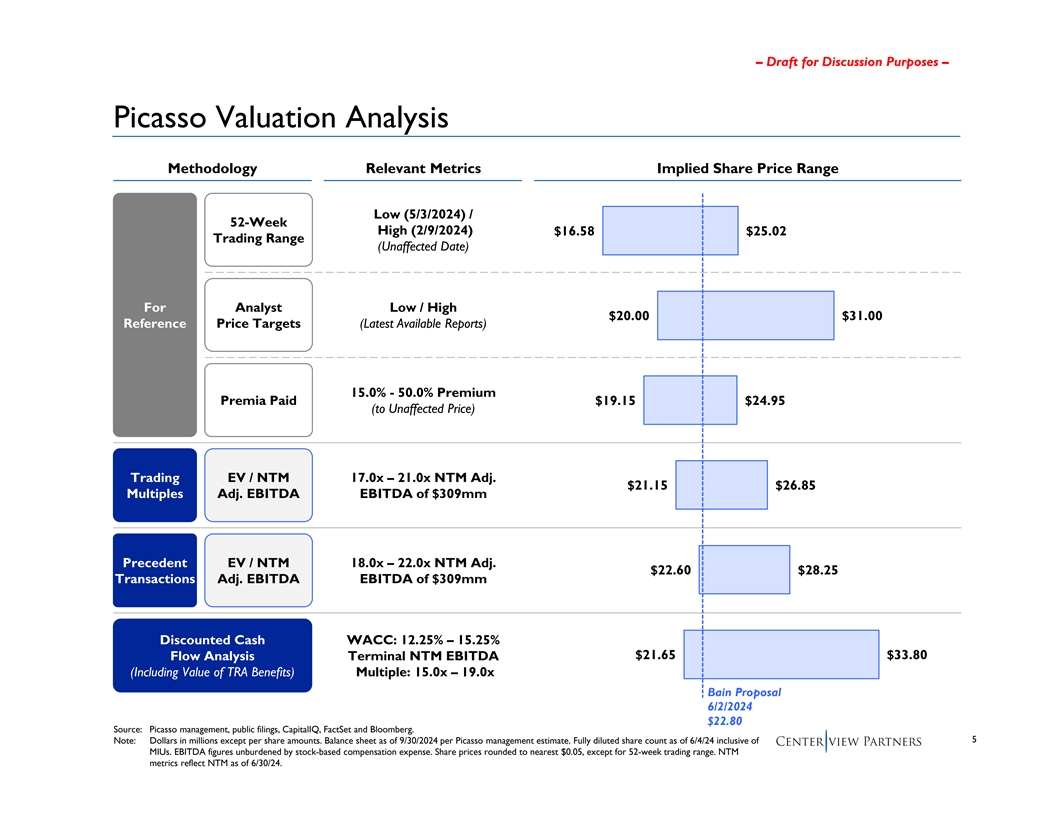

converted into the right to receive cash in an amount equal to $22.80, without interest thereon (the “Per Share Price”); (iii) any shares of Class A Common Stock held by PowerSchool as treasury stock or owned by Parent or any of its

affiliates or subsidiaries (including Merger Sub), in each case as of immediately prior to the Effective Time, which will automatically be cancelled and extinguished without conversion thereof or consideration paid in exchange (“Owned Company

Shares”); (iv) certain shares of Class A Common Stock (the “Rollover Shares”), which will be transferred together with certain limited liability company units of PowerSchool Holdings LLC (the “Rollover Units”) held by

the Principal Stockholders (as defined below) to BCPE Polymath Topco, LP, a Delaware limited partnership and affiliate of investment funds advised by Bain Capital Private Equity, LP (“BCPE Topco”), immediately prior to the Effective Time,

pursuant to support and rollover agreements entered into in connection with the Merger Agreement; and (v) shares of Class A Common Stock that are issued and outstanding immediately prior to the Effective Time (other than Owned Company

Shares) held by holders who have not consented to the adoption of the Merger Agreement in writing and who have properly exercised appraisal rights with respect to their shares in accordance with, and who have complied with, Section 262 of the

DGCL, will not be converted into the right to receive the Per Share Price (“Dissenting Company Shares”), and holders of such Dissenting Company Shares will be entitled to receive payment of the fair value of such Dissenting Company Shares

in accordance with the provisions of Section 262 of the DGCL unless and until any such holder fails to perfect or effectively withdraws or loses their rights to appraisal and payment under the DGCL. At the Effective time, each Owned Company

2

Share will automatically be cancelled and extinguished without any conversion thereof or consideration paid in exchange and any shares of Class B common stock, par value $0.0001 per share

(the “Class B Common Stock” and, together with the Class A Common Stock, the “Company Common Stock”), of PowerSchool issued and outstanding immediately prior to the Effective Time will automatically be cancelled and

shall cease to exist and no payment shall be made with respect thereto, and the holders thereof shall cease to have any rights with respect thereto. Upon consummation of the Merger, the Class A Common Stock will no longer be publicly traded,

and PowerSchool’s stockholders (other than holders of the Rollover Shares, indirectly) will cease to have any ownership interest in PowerSchool. The Rollover Shares will be exchanged by the Principal Stockholders immediately prior to the

Effective Time for common units of BCPE Topco, in accordance with the terms of the Support and Rollover Agreements, each dated as of June 6, 2024 (as may be amended, restated or otherwise modified from time to time), by and among investment

funds affiliated with Vista Equity Partners and Onex Partners Manager LP, PowerSchool and Parent. Vista and Onex have committed to a rollover so they will hold, in the aggregate, approximately 49% of the pro forma post-Closing capitalization table

of BCPE Topco.

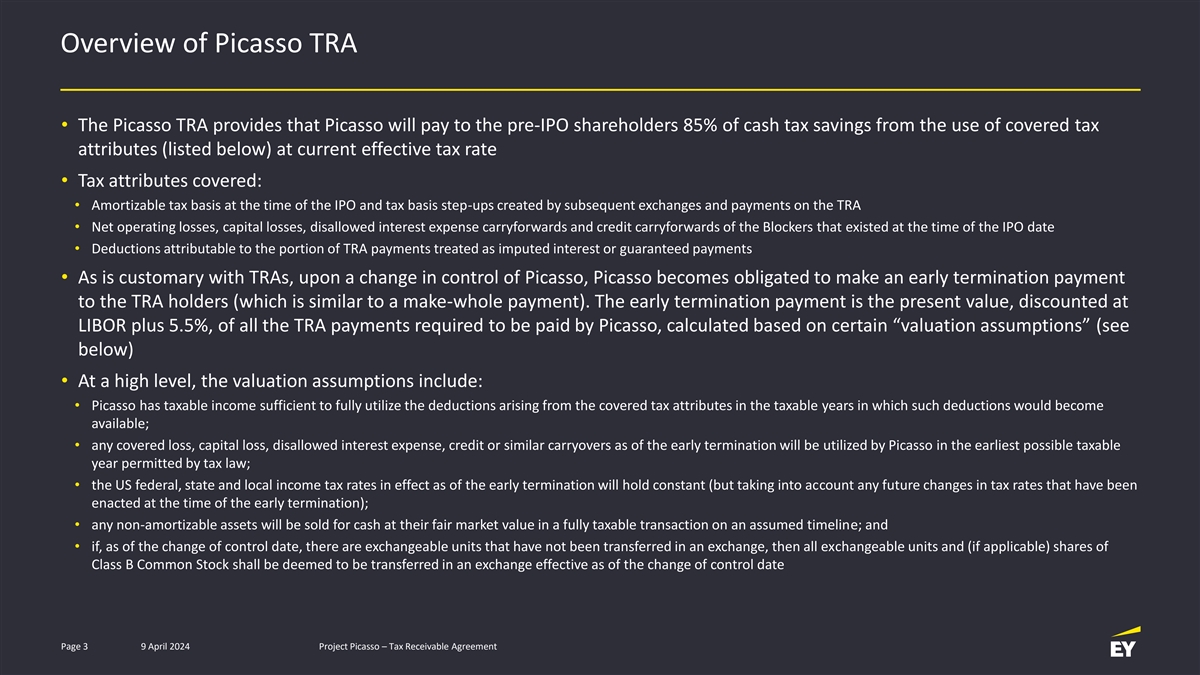

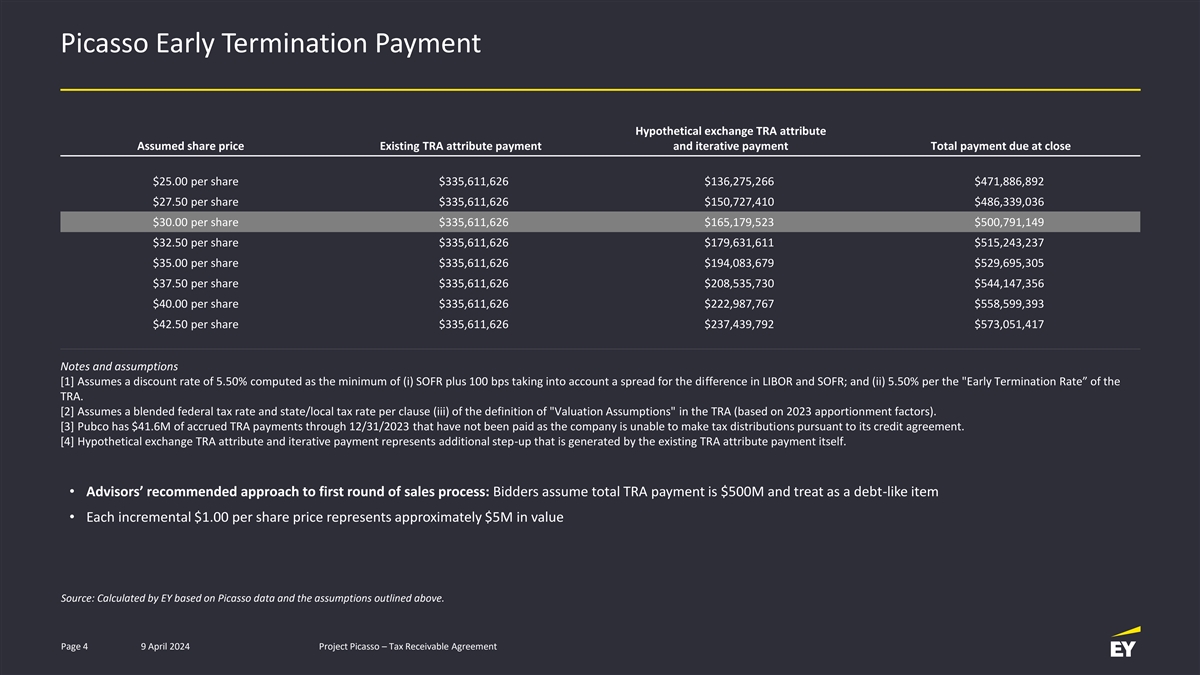

In connection with entering into the Merger Agreement, on June 6, 2024, PowerSchool and the TRA Holders (as defined

in the Tax Receivable Agreement, dated as of July 27, 2021, by and among PowerSchool, PowerSchool Holdings, LLC and the other parties identified therein (the “Tax Receivable Agreement”)) party thereto, entered into an amendment to the

Tax Receivable Agreement (the “TRA Amendment”), pursuant to which the parties agreed, among other things, to (i) amend PowerSchool’s existing Tax Receivable Agreement, such that the Tax Receivable Agreement will automatically

terminate upon the Effective Time and (ii) the TRA Holders agreed to waive certain Tax Benefit Payments (as defined in the TRA Amendment) pursuant to the Tax Receivable Agreement, including all amounts that would have otherwise become payable

to the TRA Holders in connection with the consummation of the Merger. From and after the Effective Time, no Early Termination Payment or Tax Benefit Payment (each as defined in the TRA Amendment) will be made to any TRA Holder pursuant to the Tax

Receivable Agreement.

The board of directors of PowerSchool (the “Board”) formed a special committee of the Board (the

“Special Committee”), comprised solely of independent and disinterested members of the Board, to review, evaluate and provide input on a potential sale of PowerSchool and certain alternatives thereto (including remaining an independent

company), to determine whether such a potential sale is advisable and fair to and in the best interest of PowerSchool and its stockholders and to recommend to the Board what action, if any, should be taken with respect to the potential sale of

PowerSchool. In connection with the formation of the Special Committee, the Board resolved that it would not approve any potential sale of PowerSchool that would involve the Principal Stockholders participating in an equity rollover or receiving

payments under the Tax Receivable Agreement without a prior favorable recommendation from the Special Committee. The Special Committee, as more fully described in the Information Statement (as defined below), unanimously (i) determined that it

is fair to, and in the best interests of, PowerSchool and its stockholders, and declared it advisable, to enter into the Merger Agreement providing for the Merger, with PowerSchool being the surviving corporation in the Merger in accordance with the

DGCL upon the terms and subject to the conditions set forth therein; (ii) resolved to recommend that the Board approve and adopt the Merger Agreement; and (iii) resolved to recommend that the Board submit the Merger Agreement to

PowerSchool’s stockholders for their adoption and recommend that PowerSchool’s stockholders vote in favor of the Merger Agreement. “Unaffiliated Stockholders” means the Company’s “unaffiliated security holders” as

defined under Rule 13e-3 of the Exchange Act.

The Board, acting on the unanimous

recommendation of the Special Committee, has (i) determined that it is fair to, and in the best interests of, PowerSchool and its stockholders, and declared it advisable, to enter into the Merger Agreement providing for the Merger in accordance

with the DGCL upon the terms and subject to the conditions set forth therein; (ii) approved the execution and delivery of the Merger Agreement by PowerSchool, the performance by PowerSchool of its covenants and other obligations thereunder, and

the consummation of the Merger and the other transactions contemplated by the Merger Agreement upon the terms and subject to the conditions set forth therein; (iii) directed that the adoption of the Merger Agreement be submitted for

consideration by PowerSchool’s stockholders in accordance with the Merger Agreement; and (iv) resolved to recommend that PowerSchool’s stockholders approve and adopt the Merger Agreement in accordance with the DGCL.

The adoption of the Merger Agreement by PowerSchool’s stockholders required the affirmative vote or written consent by holders of a

majority of the outstanding shares of Company Common Stock entitled to vote thereon. On June 7, 2024, Severin Topco, VEPF VI, VEPF VI-A, VEPF FAF, Onex Partners IV Select, Onex US Principals, Onex

Partners IV, Onex Partners IV GP, Onex Partners IV PV, Onex Powerschool and Pinnacle Holdings (collectively, the “Principal Stockholders”), which together on June 7, 2024 beneficially owned

3

105,321,745 shares of Class A Common Stock and 36,914,501 shares of Class B Common Stock, representing approximately 69.8% of the aggregate voting power of the issued and outstanding

shares of Company Common Stock, delivered a written consent approving and adopting in all respects the Merger Agreement and the Transactions, including the Merger. As a result, no further action by any stockholder of PowerSchool is required under

applicable law or the Merger Agreement (or otherwise) to adopt the Merger Agreement, and PowerSchool will not be soliciting your vote for or consent to the adoption of the Merger Agreement and the approval of the Transactions and will not call a

stockholders’ meeting for purposes of voting on the adoption of the Merger Agreement and the approval of the Transactions, including the Merger.

Concurrently with the filing of this Transaction Statement, PowerSchool is filing a notice of written consent and appraisal rights and

information statement (the “Information Statement”) under Regulation 14C of the Exchange Act with the SEC. The Information Statement is attached hereto as Exhibit (a)(1). A copy of the Merger Agreement is attached to the Information

Statement as Annex A. As of the date hereof, the Information Statement is in preliminary form, and is subject to completion or amendment. Terms used but not defined in this Transaction Statement have the meanings assigned to them in the Information

Statement.

Pursuant to General Instruction F to Schedule 13E-3, the information in the

Information Statement, including all annexes thereto, is expressly incorporated by reference herein in its entirety, and responses to each item herein are qualified in their entirety by the information contained in the Information Statement. The

cross-references below are being supplied pursuant to General Instruction G to Schedule 13E-3 and show the location in the Information Statement of the information required to be included in response to

the items of Schedule 13E-3.

The information concerning PowerSchool contained in, or

incorporated by reference into, this Transaction Statement and the Information Statement was supplied by PowerSchool. Similarly, all information concerning each other Filing Person contained in, or incorporated by reference into, this Transaction

Statement and the Information Statement was supplied by such Filing Person. No Filing Person, including PowerSchool, is responsible for the accuracy of any information supplied by any other Filing Person.

Item 1. Summary Term Sheet

The

information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

Item 2. Subject Company Information

(a) Name and address. The information set forth in the Information Statement under the following caption is incorporated herein

by reference:

“The Parties to the Merger Agreement”

(b) Securities. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Questions and Answers About the Merger”

“Important Information Regarding PowerSchool”

“Important Information Regarding PowerSchool—Security Ownership of Certain Beneficial Owners and Management”

(c) Trading market and price. The information set forth in the Information Statement under the following caption is incorporated

herein by reference:

“Important Information Regarding PowerSchool—Market Price of PowerSchool Class A Common Stock”

(d) Dividends. The information set forth in the Information Statement under the following caption is incorporated herein by

reference:

4

“Important Information Regarding PowerSchool—Dividends”

(e) Prior public offerings. The information set forth in the Information Statement under the following caption is incorporated

herein by reference:

“Important Information Regarding PowerSchool—Prior Public Offerings”

(f) Prior share purchases. The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Important Information Regarding PowerSchool—Prior Public Offerings”

“Important Information Regarding PowerSchool—Transactions in PowerSchool Class A Common Stock”

“Important Information Regarding PowerSchool—Past Contracts, Transactions, Negotiations and Agreements”

Item 3. Identity and Background of Filing Person

(a) — (c) Name and Address of Each Filing Person; Business and Background of Entities; Business and Background of

Natural Persons. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary—The Parties to the Merger Agreement”

“The Parties to the Merger Agreement”

“Important Information Regarding PowerSchool”

“Important Information Regarding Vista and Onex”

Item 4. Terms of the Transaction

(a) — (1) Material terms. Tender offers. Not applicable

(a) — (2) Mergers or Similar Transactions. The information set forth in the Information Statement under the

following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Plans for PowerSchool After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects on the Company if the Merger Is Not Completed”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“Special Factors—Material United States Federal Income Tax Consequences of the Merger”

“The Merger Agreement—Procedures for Receiving Merger Consideration”

“The Merger Agreement—Consideration to be Received in the Merger”

“The Merger Agreement—Conditions to Consummation of the Merger”

Annex A—Agreement and Plan of Merger

5

(c) Different terms. The information set forth in the Information Statement

under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement—Consideration to be Received in the Merger”

“The Merger Agreement—Procedure for Receiving Merger Consideration”

“The Merger Agreement—Support and Rollover Agreements”

“The Merger Agreement—TRA Amendment”

“The Merger Agreement—Indemnification and Insurance”

Annex A—Agreement and Plan of Merger

Annex D—Vista Support and Rollover Agreement

Annex E—Onex Support and Rollover Agreement

Annex F—TRA Amendment

(d)

Appraisal rights. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Questions and Answers About the Merger”

“Special Factors—Certain Effects of the Merger”

“Appraisal Rights”

Annex G—Section 262 of the General Corporation Law of the State of Delaware

(e) Provisions for unaffiliated security holders. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Special Factors—Recommendation of the Special Committee and the Board; Reasons

for the Merger”

“Provisions for Unaffiliated Stockholders”

(f) Eligibility for listing or trading. Not applicable.

Item 5. Past Contacts, Transactions, Negotiations and Agreements

(a)(1) — (2) Transactions. The information set forth in the Information Statement under the following

captions is incorporated herein by reference:

“Summary”

“Special Factors—Background of the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement”

6

“The Merger Agreement—Support and Rollover Agreements”

“The Merger Agreement—TRA Amendment”

“Important Information Regarding PowerSchool—Prior Public Offerings”

“Important Information Regarding PowerSchool—Transactions in PowerSchool Class A Common Stock”

“Important Information Regarding PowerSchool—Past Contracts, Transactions, Negotiations and Agreements”

“Important Information Regarding Vista and Onex”

Annex A—Agreement and Plan of Merger

Annex D—Vista Support and Rollover Agreement

Annex E—Onex Support and Rollover Agreement

Annex F—TRA Amendment

(b) — (c) Significant corporate events; Negotiations or contacts. The information set forth in the

Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement”

“The Merger Agreement—Support and Rollover Agreements”

“The Merger Agreement—TRA Amendment”

Annex A—Agreement and Plan of Merger

Annex D—Vista Support and Rollover Agreement

Annex E—Onex Support and Rollover Agreement

Annex F—TRA Amendment

(e)

Agreements involving the subject company’s securities. The information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement”

“The Merger Agreement—Support and Rollover Agreements”

7

“The Merger Agreement—TRA Amendment”

“Important Information Regarding PowerSchool—Transactions in PowerSchool Class A Common Stock”

“Important Information Regarding PowerSchool—Past Contracts, Transactions, Negotiations and Agreements”

Annex A—Agreement and Plan of Merger

Annex D—Vista Support and Rollover Agreement

Annex E—Onex Support and Rollover Agreement

Annex F—TRA Amendment

Item 6.

Purposes of the Transaction and Plans or Proposals

(b) Use of securities acquired. The information set forth in the

Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Plans for PowerSchool After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects on the Company if the Merger is Not Completed”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“Special Factors—Delisting and Deregistration of Class A Common Stock”

“The Merger Agreement—Consideration to be Received in the Merger”

“The Merger Agreement—Procedures for Receiving Merger Consideration”

Annex A—Agreement and Plan of Merger

(c)(1) — (8) Plans. The information set forth in the Information Statement under the following captions is

incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Plans for PowerSchool After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects on the Company if the Merger is Not Completed”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“Special Factors—Delisting and Deregistration of Class A Common Stock”

“The Merger Agreement—Consideration to be Received in the Merger”

“The Merger Agreement—Support and Rollover Agreements”

8

“The Merger Agreement—TRA Amendment”

“Important Information Regarding PowerSchool”

Annex A—Agreement and Plan of Merger

Item 7. Purposes, Alternatives, Reasons and Effects

(a) Purposes. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factor —Plans for PowerSchool After the Merger”

“Special Factors—Certain Effects of the Merger”

(b) Alternatives. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Certain Effects on PowerSchool if the Merger is Not Completed”

(c) Reasons. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

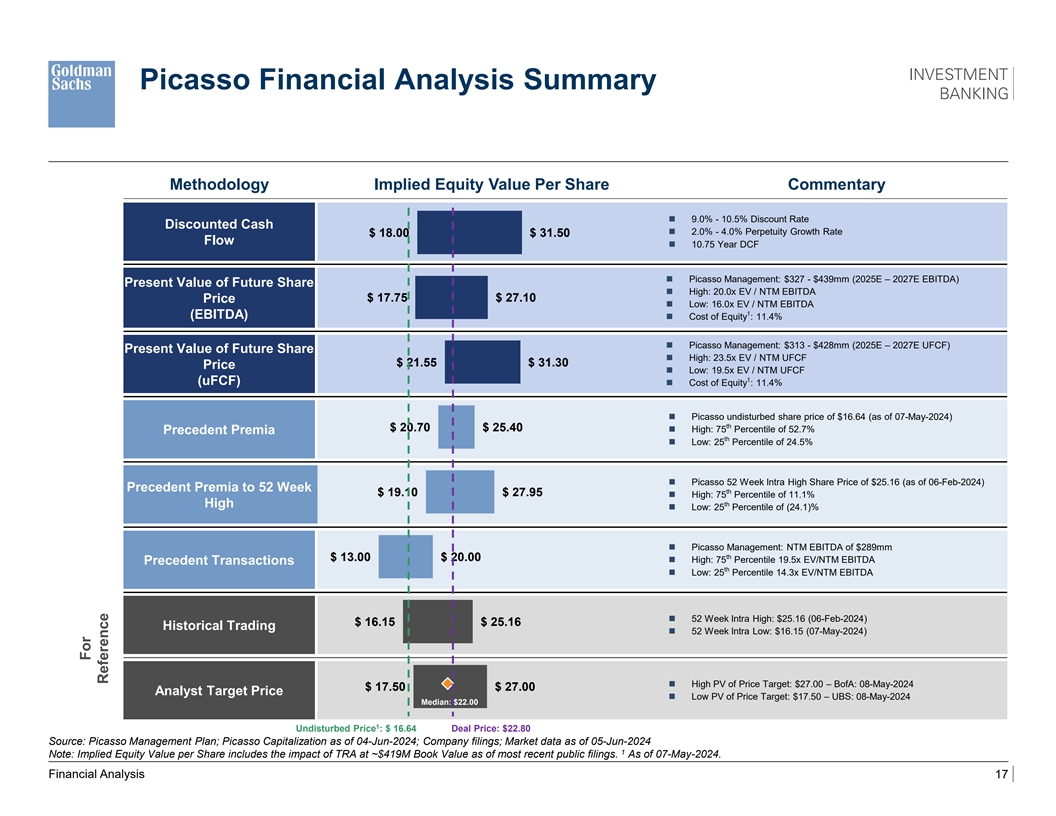

“Special Factors—Opinion of Goldman Sachs & Co. LLC”

“Special Factors—Opinion of Centerview Partners LLC”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects on the Company if the Merger is Not Completed”

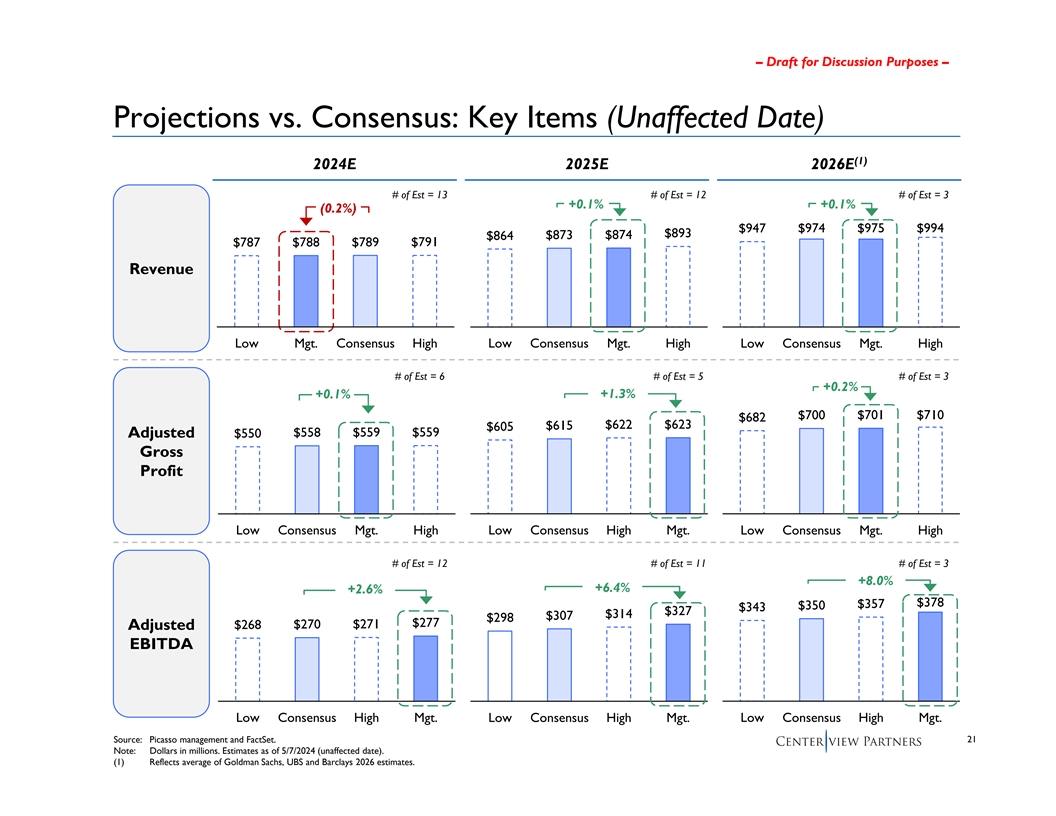

“Special Factors—Certain Company Financial Forecasts”

Annex B—Opinion of Goldman Sachs & Co. LLC

Annex C—Opinion of Centerview Partners LLC

9

(d) Effects. The information set forth in the Information Statement under the

following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Opinion of Goldman Sachs & Co. LLC”

“Special Factors—Opinion of Centerview Partners LLC”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Plans for PowerSchool After the Merger”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Effects on the Company if the Merger is Not Completed”

“Special Factors—Financing”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“Special Factors—Fees and Expenses”

“Special Factors—Delisting and Deregistration of Class A Common Stock”

“Special Factors—Material United States Federal Income Tax Consequences of the Merger”

“The Merger Agreement—Consideration to be Received in the Merger”

“The Merger Agreement—Indemnification and Insurance”

“Appraisal Rights”

Annex A—Agreement and Plan of Merger

Annex B—Opinion of Goldman Sachs & Co. LLC

Annex C—Opinion of Centerview Partners LLC

Item 8. Fairness of the Transaction

(a) — (b) Fairness; Factors considered in determining fairness. The information set forth in the

Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Opinion of Goldman Sachs & Co. LLC”

“Special Factors—Opinion of Centerview Partners LLC”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

10

“Special Factors—Certain Effects of the Merger”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

Annex B—Opinion of Goldman Sachs & Co. LLC

Annex C—Opinion of Centerview Partners LLC

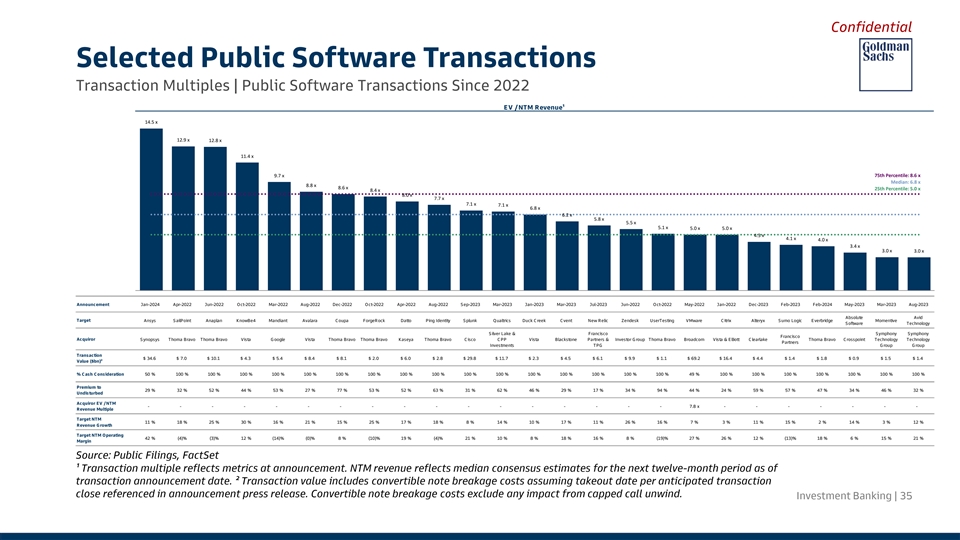

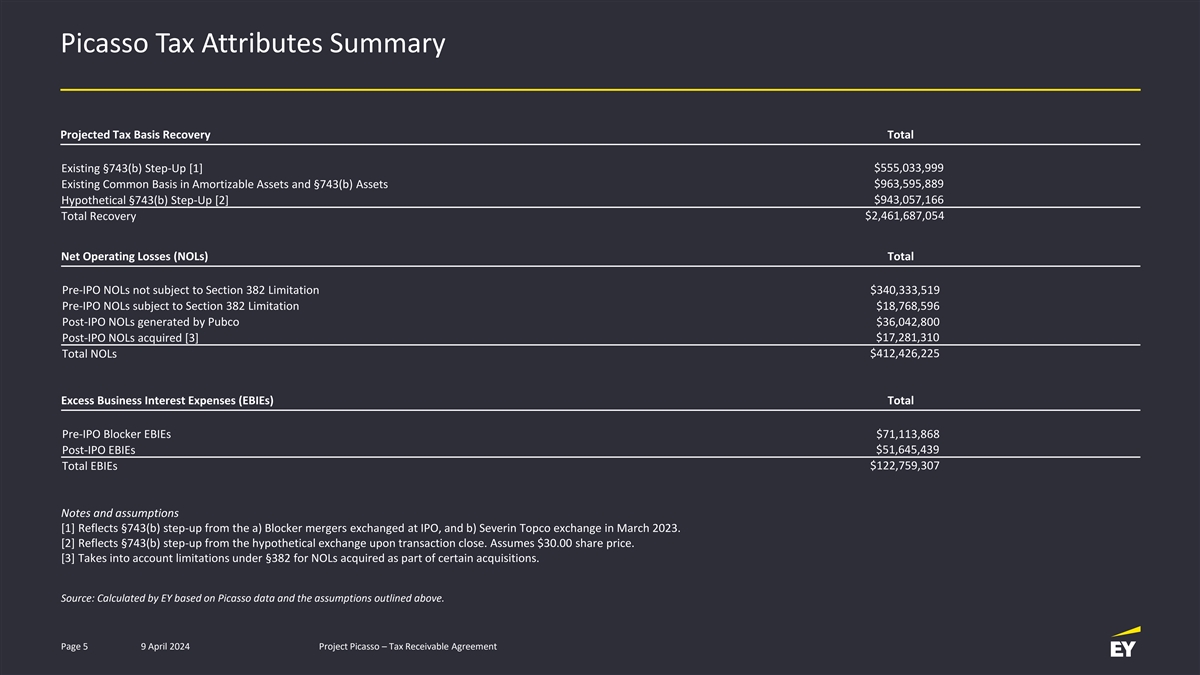

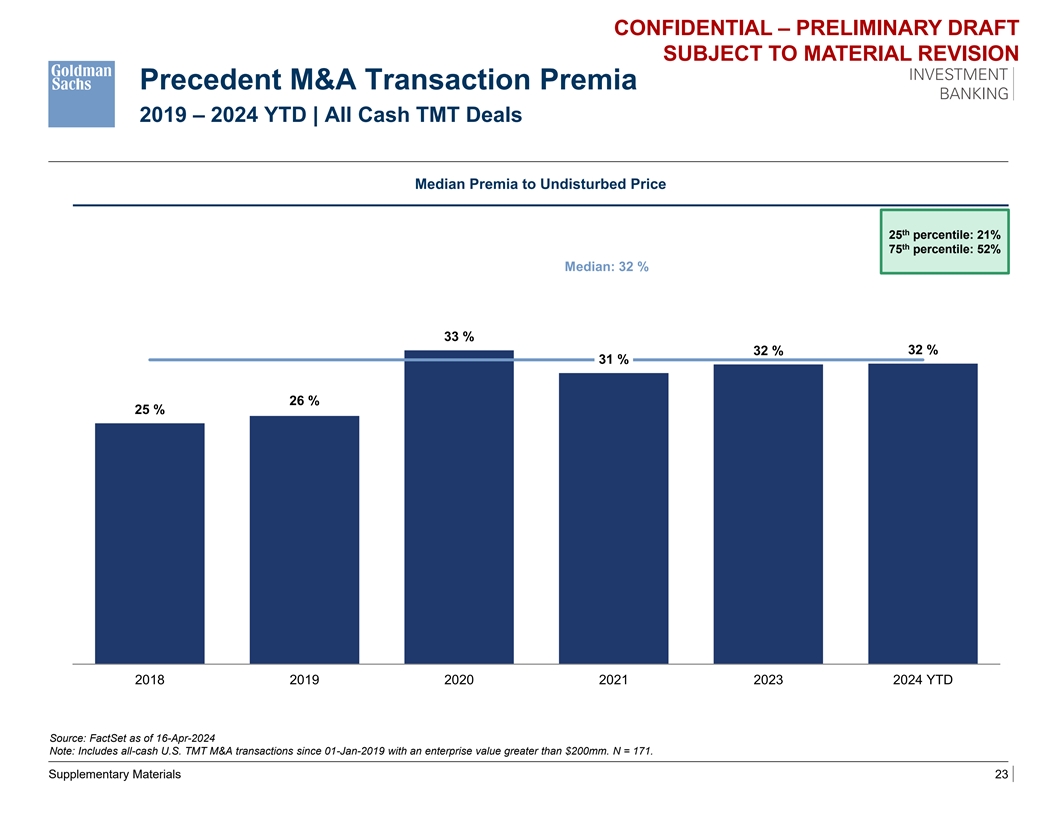

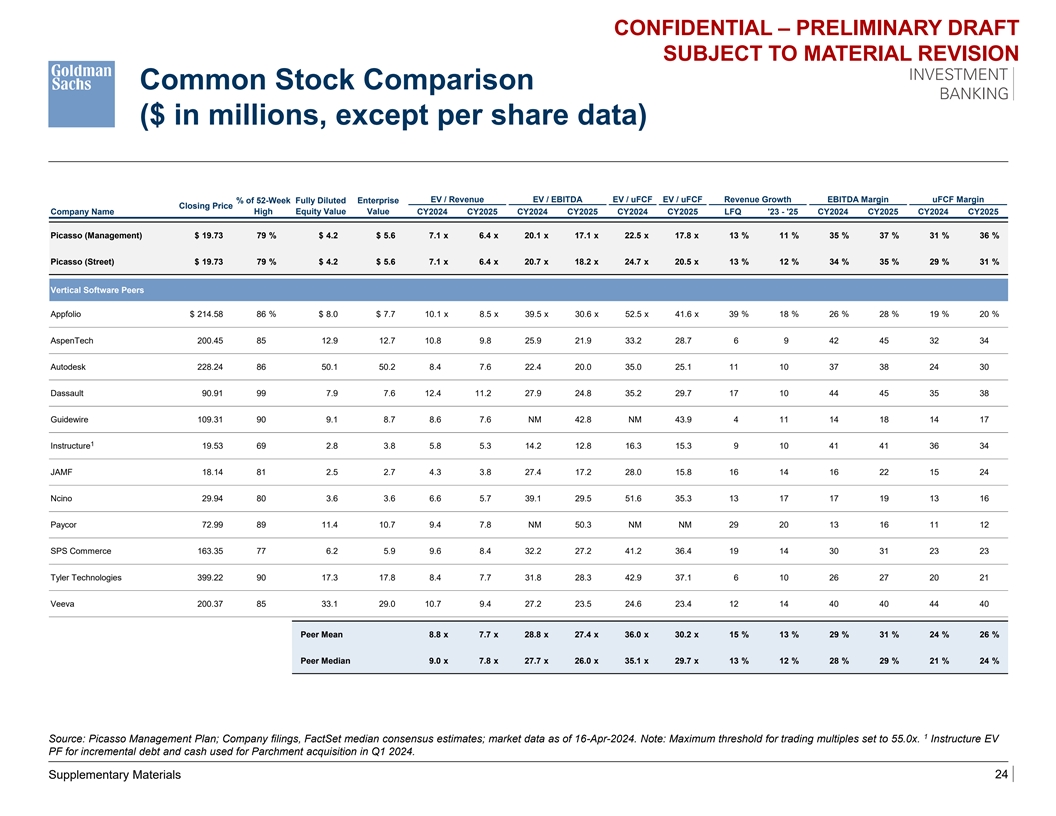

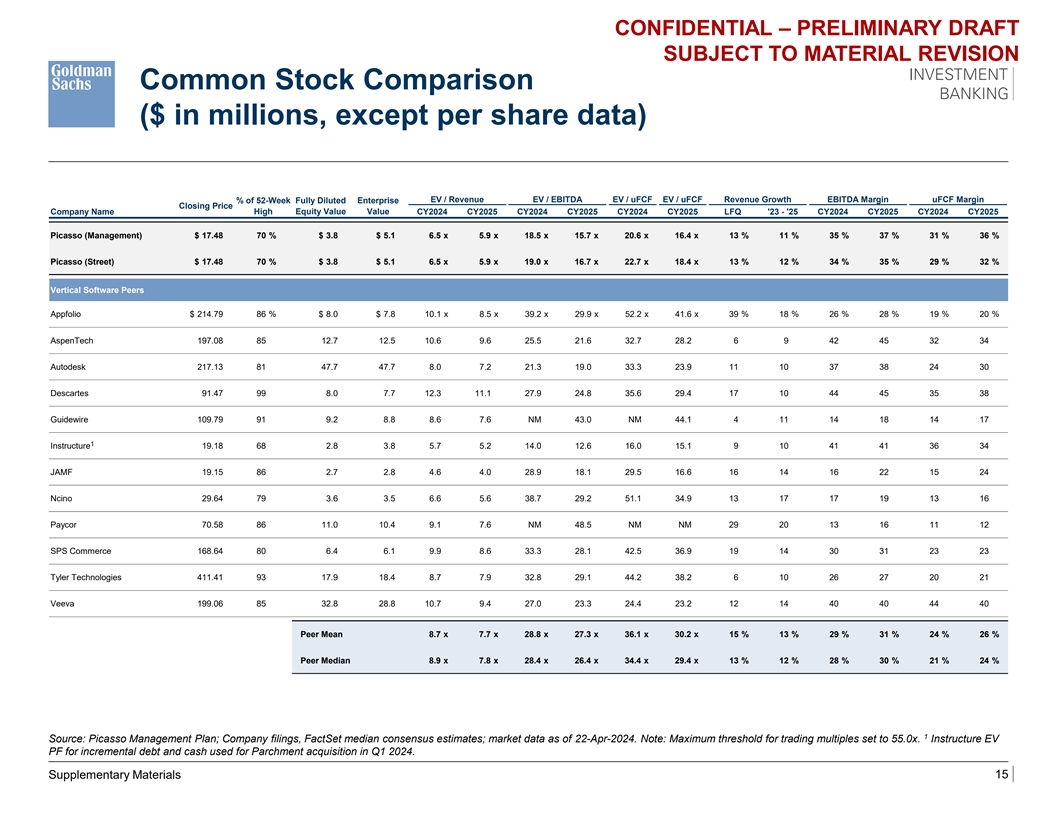

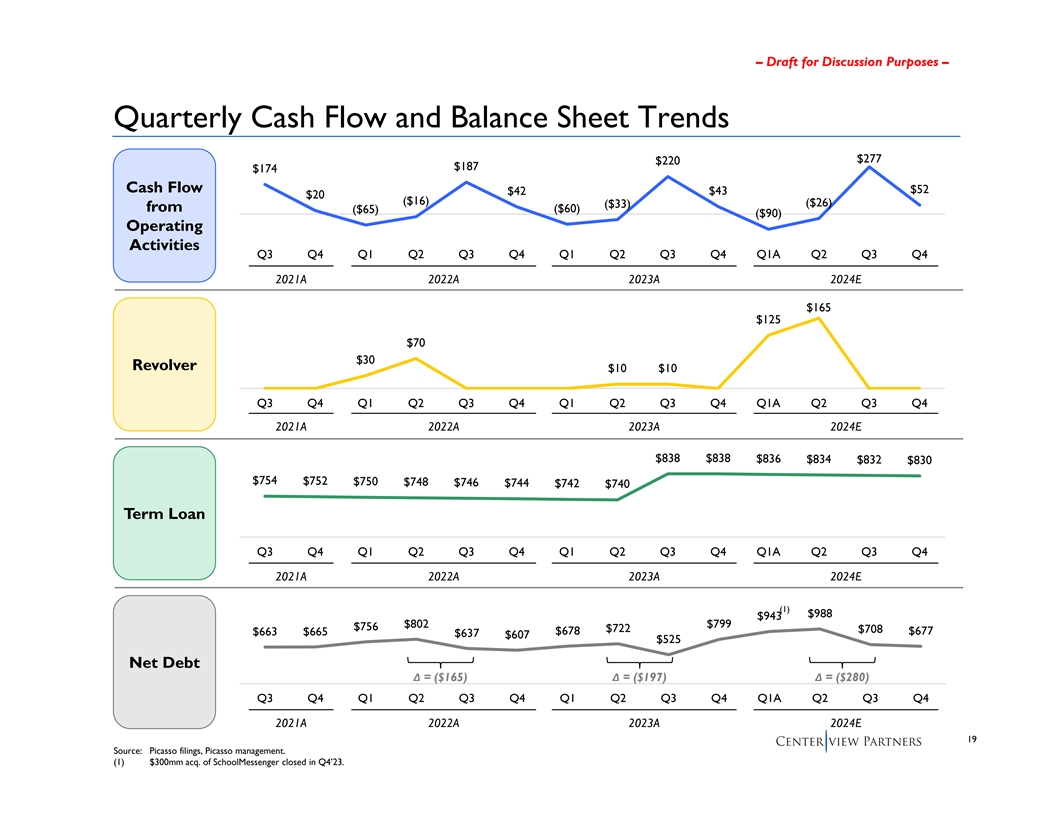

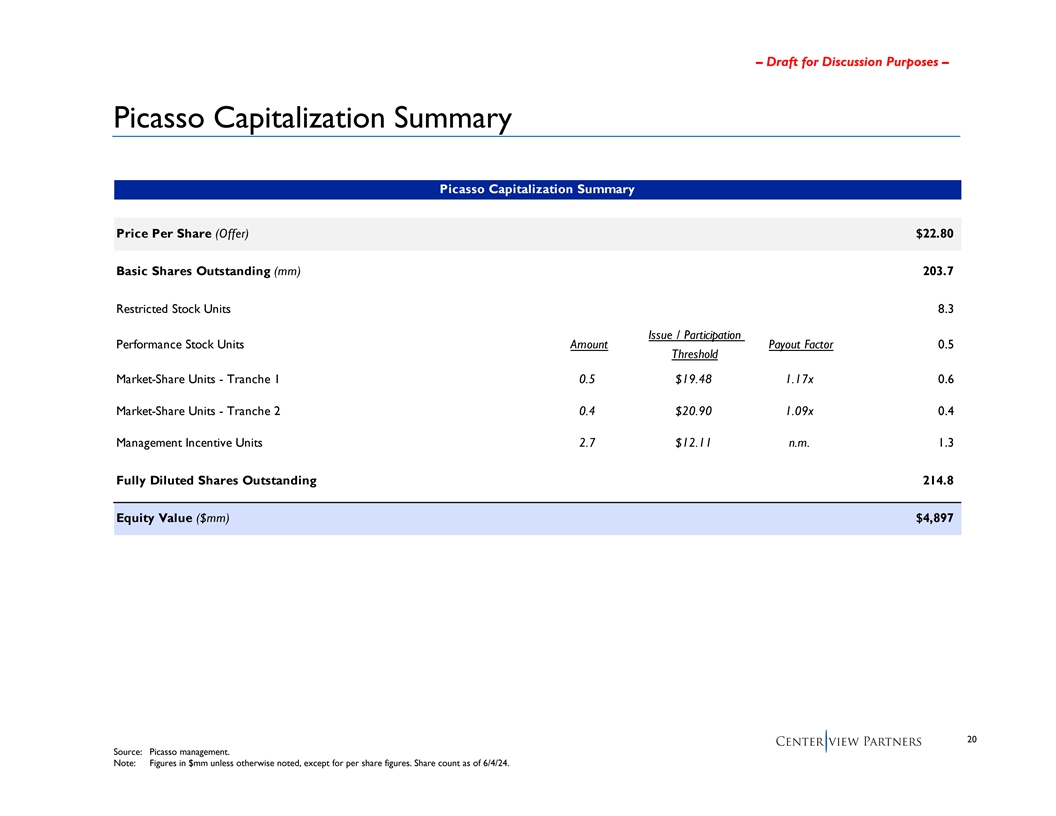

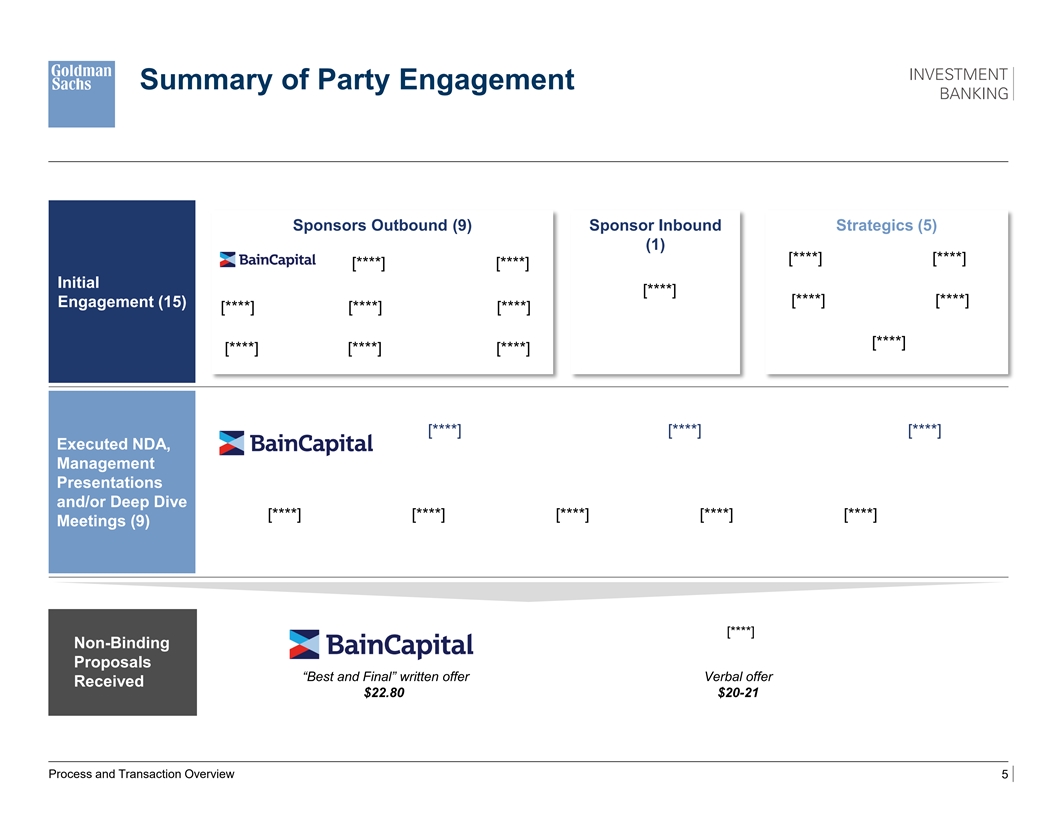

The discussion materials dated March 5, 2024, the Presentations to the Board dated April 17, 2024, April 24, 2024 and June 6, 2024, each

prepared by Goldman Sachs & Co. LLC, and the Tax Receivable Agreement Presentation dated April 9, 2024, prepared by Ernst & Young LLP, and reviewed by the Board, are filed as Exhibits (c)(iii) – (c)(vi) and Exhibit (c)(xii) and are

incorporated herein by reference.

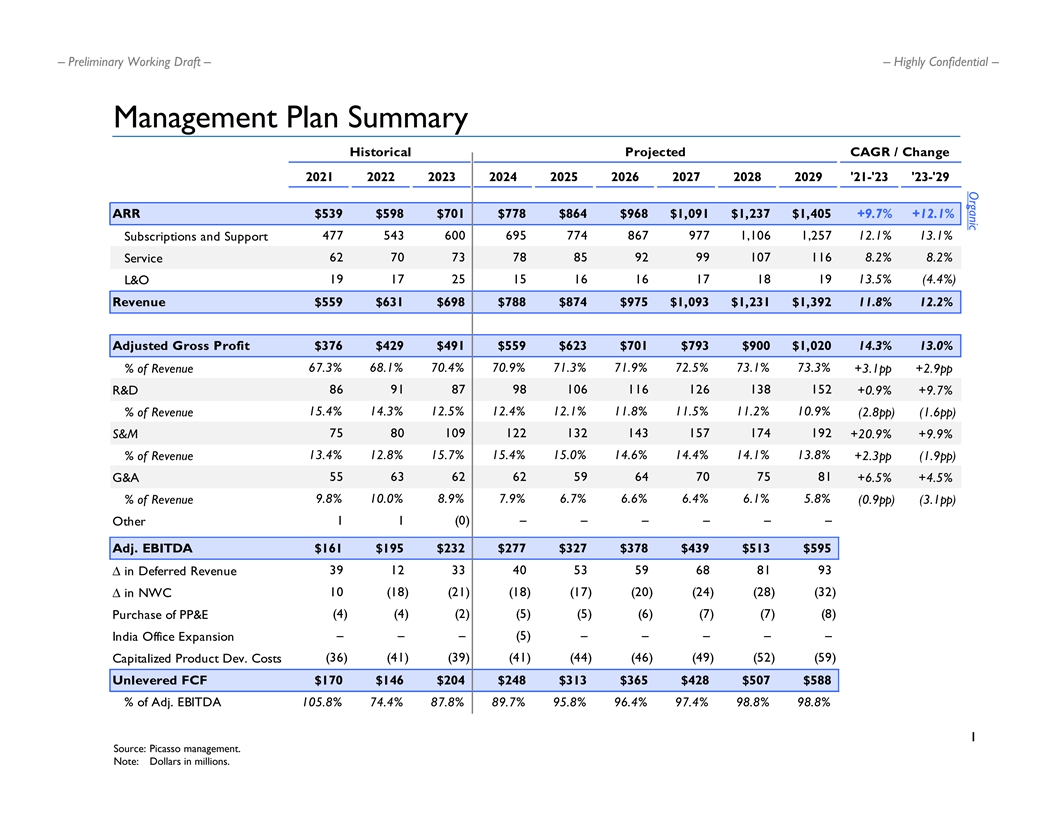

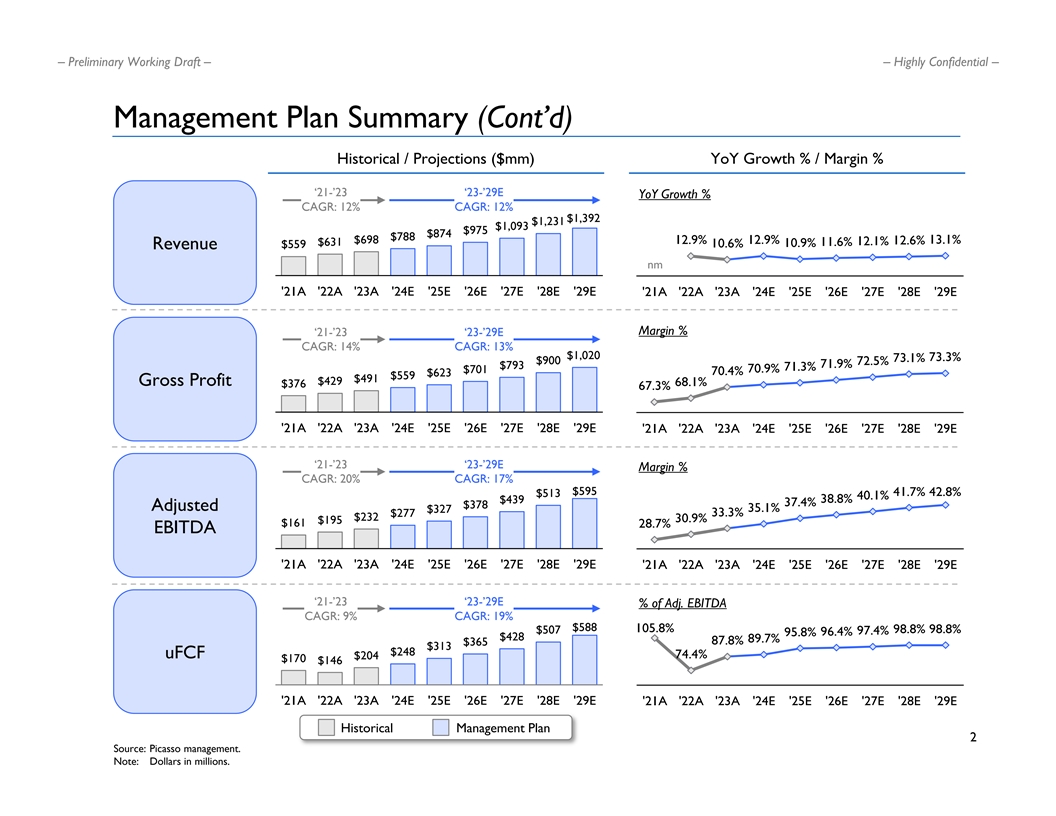

The discussion materials to the Special Committee dated May 1, 2024, May 3, 2024, May 6, 2024, June 5,

2024 and June 6, 2024, each prepared by Centerview Partners LLC and reviewed by the Special Committee, are filed as Exhibits (c)(vii) – (c)(xi) and are incorporated herein by reference.

(c) Approval of security holders. The information set forth in the Information Statement under the following captions is

incorporated herein by reference:

“Summary”

“Questions and Answers about the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Required Stockholder Approval for the Merger”

“The Merger Agreement—Company Stockholder Approval”

Annex A—Agreement and Plan of Merger

(d) Unaffiliated representative. The information set forth in the Information Statement under the following captions is

incorporated herein by reference:

“Summary”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Provisions for Unaffiliated Stockholders”

(e) Approval of directors. The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

(f) Other offers. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

11

Item 9. Reports, Opinions, Appraisals and Negotiations

(a) — (b) Report, opinion or appraisal; Preparer and summary of the report, opinion or appraisal. The

information set forth in the Information Statement under the following captions is incorporated herein by reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Opinion of Goldman Sachs & Co. LLC”

“Special Factors—Opinion of Centerview Partners LLC”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Where You Can Find More Information”

Annex B—Opinion of Goldman Sachs & Co. LLC

Annex C—Opinion of Centerview Partners LLC

The discussion materials dated March 5, 2024, the Presentations to the Board dated April 17, 2024, April 24, 2024 and June 6, 2024, each

prepared by Goldman Sachs & Co. LLC, and the Tax Receivable Agreement Presentation dated April 9, 2024, prepared by Ernst & Young LLP, and reviewed by the Board, are filed as Exhibits (c)(iii) – (c)(vi) and Exhibit (c)(xii) and are

incorporated herein by reference.

The discussion materials to the Special Committee dated May 1, 2024, May 3, 2024, May 6, 2024, June 5,

2024 and June 6, 2024, each prepared by Centerview Partners LLC and reviewed by the Special Committee, are filed as Exhibits (c)(vii) – (c)(xi) and are incorporated herein by reference.

(c) Availability of documents. The reports, opinions or appraisals referenced in this Item 9 will be made available for

inspection and copying at the principal executive offices of the Company during its regular business hours by any interested equity holder of the Company or by a representative who has been so designated in writing.

Item 10. Source and Amounts of Funds or Other Consideration

(a) — (b), (d) Source of funds; Conditions; Borrowed funds. The information set forth in the Information

Statement under the following captions is incorporated herein by reference:

“Summary”

“Special Factors—Financing”

“The Merger Agreement—Conduct of Business by PowerSchool Prior to Consummation of the Merger”

“The Merger Agreement—Conditions to Consummation of the Merger”

Annex A—Agreement and Plan of Merger

(c) Expenses. The information set forth in the Information Statement under the following captions is incorporated herein by

reference:

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Certain Effects on the Company if the Merger is Not Completed”

“Special Factors—Fees and Expenses”

“The Merger Agreement—Termination Fees and Expenses”

Annex A—Agreement and Plan of Merger

12

Item 11. Interest in Securities of the Subject Company

(a) Securities ownership. The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Summary”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement—Support and Rollover Agreements”

“Important Information Regarding PowerSchool”

“Important Information Regarding PowerSchool—Security Ownership of Certain Beneficial Owners and Management”

Annex D—Vista Support and Rollover Agreement

Annex E—Onex Support and Rollover Agreement

(b) Securities transactions. The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Special Factors—Background of the Merger”

“The Merger Agreement”

‘The Merger Agreement—Support and Rollover Agreements”

“Important Information Regarding PowerSchool—Prior Public Offerings”

“Important Information Regarding PowerSchool—Transactions in PowerSchool Class A Common Stock”

Annex A—Agreement and Plan of Merger

Annex D—Vista Support and Rollover Agreement

Annex E—Onex Support and Rollover Agreement

Item 12. The Solicitation or Recommendation

(d) Intent to tender or vote in a going-private transaction. Not applicable.

(e) Recommendation of others. Not applicable.

Item 13. Financial Information

(a)

Financial statements. The audited consolidated financial statements set forth in Item 8 of the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023 are

incorporated herein by reference.

The information set forth in the Information Statement under the following captions is incorporated

herein by reference:

“Special Factors—Certain Effects of the Merger”

“Special Factors—Certain Company Financial Forecasts”

“Important Information Regarding PowerSchool—Book Value Per Share”

“Where You Can Find More Information”

(b) Pro forma information. Not applicable.

Item 14. Persons/Assets, Retained, Employed, Compensated or Used

(a) — (b) Solicitations or recommendations; Employees and corporate assets. The information set forth in

the Information Statement under the following captions is incorporated herein by reference:

13

“Summary”

“Questions and Answers About the Merger”

“Special Factors—Background of the Merger”

“Special Factors—Recommendation of the Special Committee and the Board; Reasons for the Merger”

“Special Factors—Reasons of Vista and Onex for the Merger”

“Special Factors—Position of Vista and Onex as to the Fairness of the Merger”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“Special Factors—Fees and Expenses”

Item 15. Additional Information

(b) Golden Parachute Compensation. The information set forth in the Information Statement under the following captions is

incorporated herein by reference:

“Summary”

“Special Factors—Certain Effects of the Merger”

“Special Factors—Interests of Our Directors and Executive Officers in the Merger”

“The Merger Agreement—Consideration to be Received in the Merger”

Annex A—Agreement and Plan of Merger

(c) Other material information. The information set forth in the Information Statement, including all annexes thereto, is

incorporated herein by reference.

Item 16. Exhibits

The following exhibits are filed herewith:

|

|

|

| (a)(i) |

|

Preliminary Information Statement of PowerSchool Holdings, Inc. (included in the Schedule 14C filed on July 23, 2024 and incorporated herein by reference). |

|

|

| (a)(ii) |

|

Notice of Written Consent and Appraisal Rights (included in the Information Statement and incorporated herein by reference). |

|

|

| (b)(i) |

|

Equity Commitment Letter, dated as of June 6, 2024, by and among BCPE Polymath Buyer, Inc., Bain Capital Fund XIII, L.P. and Bain Capital Fund (Lux) XIII, SCSp. |

|

|

| (b)(ii) |

|

Limited Guarantee, dated as of June 6, 2024, entered into by Bain Capital Fund XIII, L.P. and Bain Capital Fund (Lux) XIII, SCSp in favor of PowerSchool Holdings, Inc. |

|

|

| (b)(iii) |

|

Commitment Letter, dated as of June, 2024, by and among BCPE Polymath Buyer, Inc., Ares Capital Management LLC, Blackstone Alternative Credit Advisors LP, Blue Owl Credit Advisors LLC, Golub Capital LLC, HPS Investment Partners LLC and Sixth Street Partners, LLC. |

|

|

| (c)(i) |

|

Opinion of Goldman Sachs & Co. LLC, dated June 6, 2024 (included as Annex B to the Information Statement and incorporated herein by reference). |

|

|

| (c)(ii) |

|

Opinion of Centerview Partners LLC, dated June 6, 2024 (included as Annex C to the Information Statement and incorporated herein by reference). |

|

|

| (c)(iii) |

|

Discussion Materials prepared by Goldman Sachs & Co. LLC for the Board of Directors, dated March 5, 2024. |

|

|

| (c)(iv) |

|

Tax Receivable Agreement Presentation by Ernst & Young LLP for the Board of Directors, dated April 9, 2024. |

|

|

| (c)(v)* |

|

Presentation to the Board of Directors by Goldman Sachs & Co. LLC, dated April 17, 2024.

|

14

|

|

|

| (c)(vi)* |

|

Presentation to the Board of Directors by Goldman Sachs & Co. LLC, dated April 24, 2024. |

|

|

| (c)(vii) |

|

Discussion materials prepared by Centerview Partners LLC for the Special Committee of the Board of Directors, dated May 1, 2024 |

|

|

| (c)(viii) |

|

Discussion materials prepared by Centerview Partners LLC for the Special Committee of the Board of Directors, dated May 3, 2024. |

|

|

| (c)(ix) |

|

Discussion materials prepared by Centerview Partners LLC for the Special Committee of the Board of Directors, dated May 6, 2024. |

|

|

| (c)(x) |

|

Discussion materials prepared by Centerview Partners LLC for the Special Committee of the Board of Directors, dated June 5, 2024. |

|

|

| (c)(xi) |

|

Discussion materials prepared by Centerview Partners LLC for the Special Committee of the Board of Directors, dated June 6, 2024. |

|

|

| (c)(xii)* |

|

Presentation to the Board of Directors by Goldman Sachs & Co. LLC, dated June 6, 2024. |

|

|

| (d)(i) |

|

Agreement and Plan of Merger, dated as of June 6, 2024, by and among PowerSchool Holdings, Inc., BCPE Polymath Buyer, Inc. and BCPE Polymath Merger Sub, Inc. (included as Annex A to the Information Statement and incorporated herein by reference). |

|

|

| (d)(ii) |

|

Support and Rollover Agreement, by and among PowerSchool Holdings, Inc., BCPE Polymath Buyer, Inc., and BCPE Polymath Merger Sub, Inc., Vista Consulting Group, LLC, the stockholder parties thereto and the other signatory parties thereto, dated June 6, 2024. (included as Annex D to the Information Statement and incorporated herein by reference). |

|

|

| (d)(iii) |

|

Support and Rollover Agreement, by and among PowerSchool Holdings, Inc., BCPE Polymath Buyer, Inc., and BCPE Polymath Merger Sub, Inc., Onex Partners Manager LP., the stockholder parties thereto and the other signatory parties thereto, dated June 6, 2024. (included as Annex E to the Information Statement and incorporated herein by reference). |

|

|

| (d)(iv) |

|

Amendment No. 1 to the Tax Receivable Agreement, by and among PowerSchool Holdings, Inc. and the TRA Holders parties thereto, dated June 6, 2024. (included as Annex F to the Information Statement and incorporated herein by reference). |

|

|

| (f) |

|

Section 262 of the General Corporation Law of the State of Delaware (included as Annex G to the Information Statement and incorporated herein by reference). |

|

|

| (g) |

|

None. |

|

|

| 107 |

|

Filing Fee Table. |

| * |

Certain portions of this exhibits marked with “[****]” have been redacted and separately filed with

the Securities and Exchange Commission pursuant to a request for confidential treatment. |

15

SIGNATURES

After due inquiry and to the best of the undersigned’s knowledge and belief, the undersigned certifies that the information set forth in

this statement is true, complete and correct.

|

|

|

| POWERSCHOOL HOLDINGS, INC. |

|

|

| By: |

|

/s/ Hardeep Gulati |

|

|

Name: Hardeep Gulati |

|

|

Title: Chief Executive Officer |

[Signature Page

to SC 13E-3]

16

After due inquiry and to the best of the undersigned’s knowledge and belief, the

undersigned certifies that the information set forth in this statement is true, complete and correct.

|

|

|

| VISTA EQUITY PARTNERS FUND VI, L.P. |

|

| By: Vista Equity Partners Fund VI GP, L.P. |

| Its: General Partner |

|

| By: VEPF VI GP, Ltd. |

| Its: General Partner |

|

|

| By: |

|

/s/ Robert F. Smith |

|

|

Name: Robert F. Smith |

|

|

Title: Director |

|

| VISTA EQUITY PARTNERS FUND VI-A, L.P. |

|

| By: Vista Equity Partners Fund VI GP, L.P. |

| Its: General Partner |

|

| By: VEPF VI GP, Ltd. |

| Its: General Partner |

|

|

| By: |

|

/s/ Robert F. Smith |

|

|

Name: Robert F. Smith |

|

|

Title: Director |

|

| VEPF VI FAF, L.P. |

|

| By: Vista Equity Partners Fund VI GP, L.P. |

| Its: General Partner |

|

| By: VEPF VI GP, Ltd. |

| Its: General Partner |

|

|

| By: |

|

/s/ Robert F. Smith |

|

|

Name: Robert F. Smith |

|

|

Title: Director |

|

| SEVERIN TOPCO, LLC |

|

|

| By: |

|

/s/ Hardeep Gulati |

|

|

Name: Hardeep Gulati |

|

|

Title: Chief Executive Officer |

|

| VEP GROUP, LLC |

|

|

| By: |

|

/s/ Robert F. Smith |

|

|

Name: Robert F. Smith |

|

|

Title: Managing Member |

[Signature Page

to SC 13E-3]

17

|

|

|

| By: |

|

/s/ Robert F. Smith |

|

|

Name: Robert F. Smith |

[Signature Page

to SC 13E-3]

18

After due inquiry and to the best of the undersigned’s knowledge and belief, the

undersigned certifies that the information set forth in this statement is true, complete and correct.

|

|

|

| PINNACLE HOLDINGS I L.P. |

|

| By: Pinnacle Holdings I GP Inc. |

| Its: General Partner |

|

|

| By: |

|

/s/ Laurence Goldberg |

|

|

Name: Laurence Goldberg |

|

|

Title: Vice President |

|

| ONEX PARTNERS IV SELECT LP |

|

| By: Onex Partners IV GP LLC |

| Its: General Partner |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX US PRINCIPALS LP |

|

| By: Onex American Holdings GP LLC |

| Its: General Partner |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX PARTNERS IV LP |

|

| By: Onex Partners IV GP LP |

| Its: General Partner |

|

| By: Onex Partners IV GP Limited |

| Its: General Partner |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX PARTNERS IV GP LP |

|

| By: Onex Partners IV GP Limited |

| Its: General Partner |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

[Signature Page

to SC 13E-3]

19

|

|

|

| ONEX PARTNERS IV PV LP |

|

| By: Onex Partners IV GP LP |

| Its: General Partner |

|

| By: Onex Partners IV GP Limited |

| Its: General Partner |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX POWERSCHOOL LP |

|

| By: Onex American Holdings GP LLC |

| Its: General Partner |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| OPH B LP |

|

| By: OPH B GP LLC |

| Its: General Partner |

|

| By: Onex Partners Holdings LLC |

| Its: Managing Member |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX PARTNERS CANADIAN GP INC. |

|

|

| By: |

|

/s/ David Copeland |

|

|

Name: David Copeland |

|

|

Title: Vice President |

|

| ONEX AMERICAN HOLDINGS GP LLC |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX PRIVATE EQUITY HOLDINGS LLC |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

[Signature Page

to SC 13E-3]

20

|

|

|

| ONEX PARTNERS IV GP LTD. |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX PARTNERS IV GP LLC |

|

|

| By: |

|

/s/ Joshua Hausman |

|

|

Name: Joshua Hausman |

|

|

Title: Director |

|

| ONEX CORPORATION |

|

|

| By: |

|

/s/ David Copeland |

|

|

Name: David Copeland |

|

|

Title: Managing Director, Finance |

|

|

| By: |

|

/s/ Gerald W. Schwartz |

|

|

Name: Gerald W. Schwartz |

[Signature Page

to SC 13E-3]

21

Exhibit (b)(i)

June 6, 2024

BCPE Polymath Buyer, Inc.

c/o Bain Capital Private Equity, LP

200 Clarendon Street

Boston, MA 02116

Ladies and Gentlemen:

This letter agreement (this “Agreement”) sets forth the commitment of each of Bain Capital Fund XIII, L.P., a Delaware

limited partnership, and Bain Capital Fund (Lux) XIII, SCSp, a special limited partnership organized and established under the laws of Grand Duchy of Luxembourg (each individually, a “Fund” and collectively, the

“Funds”), to purchase, directly or indirectly, on the terms and subject to the conditions contained herein, certain equity interests of BCPE Polymath Buyer, Inc., a newly formed Delaware corporation

(“Parent”), formed to acquire, hold and dispose of, directly or indirectly, equity interests of PowerSchool Holdings, Inc., a Delaware corporation (the “Company”), pursuant to the transactions

contemplated by that certain Agreement and Plan of Merger (as amended, amended and restated, supplemented or otherwise modified from time to time, the “Merger Agreement”), dated as of the date hereof, by and among Parent, the

Company and BCPE Polymath Merger Sub, Inc., a Delaware corporation (“Merger Sub”). Capitalized terms used and not otherwise defined herein shall have the meanings ascribed to such terms in the Merger Agreement.

1. Commitments. Each Fund hereby commits, severally and not jointly or jointly and severally, on the terms and subject to

conditions set forth herein, at or prior to the Closing, to purchase, or shall cause the purchase of, directly or indirectly through one or more intermediate entities, equity securities of Parent for an aggregate purchase price not to exceed such

Fund’s Pro Rata Percentage (as defined below) of $1,748,566,902 (as to each Fund, the “Individual Commitment Cap,” and in the aggregate, the “Commitment Amount”) (such commitment, the

“Commitment”), the proceeds of which, together with the net proceeds of the Debt Financing, will be used, as needed, solely to (i) fund amounts required to be paid by Parent pursuant to the last sentence of

Section 2.7(d), Section 2.8(e) and Section 2.9(b) of the Merger Agreement and (ii) without duplication, pay related fees, costs and expenses required to be paid by Parent or

Merger Sub in connection with the Merger at the Closing pursuant to the Merger Agreement (collectively, clauses (i) and (ii), “Closing Payments”). Notwithstanding anything to the contrary in this Agreement, (a) this

Agreement may not be enforced against any Fund without giving effect to its Individual Commitment Cap, and no Fund shall be liable for any amounts hereunder in excess of its Individual Commitment Cap, and (b) each Fund may allocate all or a

portion of its Commitment to one or more affiliated investment funds, affiliated separately managed accounts or affiliated investment vehicles and such Fund’s portion of the Commitment Amount will be reduced by its Pro Rata Percentage of any

amounts actually contributed to Parent by such other Persons (and not returned) at or prior to the Closing, so long as such assignment would not reasonably be expected to (i) prevent, impair or delay the consummation of the transactions

contemplated by the Merger Agreement or (ii) require any additional regulatory filings, of which the failure to obtain would prevent, impair or delay the consummation of the transactions contemplated by the Merger

1

Agreement; provided, however, that any such assignment shall not relieve such Fund of any of its obligations under this letter (including its obligation to fund its Individual Commitment Cap of

the Commitment hereunder), except to the extent performed at Closing by such affiliated investment funds, affiliated separately managed accounts or affiliated investment vehicles. All payments hereunder shall be made in lawful money of the United

States, in immediately available funds.

2. Conditions. Each Fund’s obligation to fund its Pro Rata Percentage of the

Commitment Amount shall be subject to (i) the execution and delivery of the Merger Agreement by the Parties to the Merger Agreement, (ii) satisfaction or valid waiver of each of the conditions to Parent and Merger Sub’s obligations to

effect the Closing set forth in Section 7.1 and Section 7.2 of the Merger Agreement (in each case, other than any conditions that by their nature are to be satisfied at the Closing, but

subject to the prior or substantially concurrent satisfaction or valid waiver of such conditions), (iii) the substantially simultaneous consummation of the Closing in accordance with the terms of the Merger Agreement, (iv) the substantially

contemporaneous funding of the full amount of the Debt Financing in accordance with the terms of the Debt Commitment Letter and (v) the consummation of the Rollover immediately prior to or substantially concurrent with the consummation of the

Closing pursuant to the terms of the Merger Agreement and the Support and Rollover Agreement.

3. Limited Guarantee.

Concurrently with the execution and delivery of this Agreement, the Funds have executed and delivered to the Company a limited guarantee pursuant to which the Funds have agreed, on the terms and subject to the conditions therein, to guarantee

certain of Parent’s payment obligations under the Merger Agreement (the “Limited Guarantee”). Each Fund acknowledges and agrees that if the conditions described in Section 2 hereof are

satisfied, the Company may seek an order of specific performance to enforce each Fund’s obligation to fund its Pro Rata Percentage of the Commitment Amount hereunder, pursuant to (and on the terms and subject to the conditions of)

Section 9.9(b)(ii) of the Merger Agreement (the “Specific Performance Rights”). Other than the Specific Performance Rights and the other Retained Claims (as defined in the Limited Guarantee), the

Company’s right to receive payment from Parent of the Guaranteed Obligations (as defined in the Limited Guarantee), subject to the Cap (as defined in the Limited Guarantee) and otherwise on the terms and subject to the conditions of the Limited

Guarantee, is and shall be the sole and exclusive direct or indirect remedy (whether at law or in equity) available to the Company, its Subsidiaries, any of their respective directors, officers, employees, and Affiliates, and each of the Rollover

Stockholders and any other security holder of the Company who has executed and delivered a Support and Rollover Agreement and any of their respective Affiliates (each such Person, a “Company Related Party”) (or available to

any Person claiming by, through, or on behalf or for the benefit of any of the Company Related Parties) against the Funds or any other Non-Recourse Party (as defined in the Limited Guarantee) with respect to

any claim (whether sounding in contract or tort, under statute or otherwise) arising under or related to the Merger Agreement, the Limited Guarantee, this Agreement or the transactions contemplated hereby or thereby or related negotiations,

including without limitation in connection with any breach or alleged breach by Parent or Merger Sub of any obligation under or related to the Merger Agreement, whether or not any such breach or alleged breach is caused by the Funds’ breach of

their obligations under this Agreement and any breach or alleged breach by the Funds of any obligation under or related to the Limited Guarantee or this Agreement. Each Fund agrees, solely in the context of Section 9.9(b)

of the Merger Agreement, not to oppose the granting of an injunction or specific performance on the basis that (i) the Company has an adequate remedy at law or (ii) an award of specific performance is not an appropriate remedy for any

reason at law or in equity.

2

4. Confidentiality. This Agreement shall be treated as confidential and is

being provided to Parent solely in connection with the transactions contemplated by the Merger Agreement. This Agreement may not be used, circulated, quoted or otherwise referred to in any document (other than the Limited Guarantee and the Merger

Agreement) by Parent, the Company or their respective Affiliates except with the prior written consent of Parent and the Funds in each instance; provided, that no such written consent is required for any disclosure of the existence of this

Agreement (i) to the extent required by applicable Law (provided, that to the extent permissible by applicable Law, the disclosing party shall use its commercially reasonable efforts to give the

non-disclosing parties prior notice of such disclosure and, upon any such other party’s request, shall use commercially reasonable efforts to obtain confidential treatment for the existence and terms of

this letter) or in connection with any litigation related to the Merger Agreement or the transactions contemplated hereby or thereby, (ii) in connection with seeking the approval, consent, or waiver from, or in connection with the filing of any

notices or similar responses, in each case with any Governmental Authority as required by the Merger Agreement, or (iii) to representatives of Parent or the Company who reasonably need to know of the existence of this Agreement in connection

with the transactions contemplated hereby. Notwithstanding the foregoing, this Agreement may be provided to certain investment funds managed or controlled by Affiliates of Bain Capital Private Equity, LP, and the existence of this Agreement may be

disclosed by them to (x) their respective Affiliates and representatives who are subject to confidentiality obligations and (y) to the extent required by Law.

5. Representations and Warranties. Each Fund hereby represents and warrants to Parent that (a) it is duly organized, validly

existing and in good standing under the laws of the jurisdiction of its organization, (b) it has all requisite power and authority to execute, deliver and perform this Agreement, (c) the execution, delivery and performance of this

Agreement by it has been duly and validly authorized and approved by all necessary general partner, manager or other organizational action by such Fund, (d) this Agreement has been duly and validly executed and delivered by such Fund and

(assuming due execution and delivery of this Agreement, the Merger Agreement and the Limited Guarantee by all the other parties hereto and thereto) constitutes a legal, valid and binding obligation of such Fund, enforceable against such Fund in

accordance with its terms, subject to (i) the effects of bankruptcy, insolvency, fraudulent conveyance, reorganization, moratorium or other similar laws affecting creditors’ rights generally, and (ii) general equitable principles

(whether considered in a proceeding in equity or at law), (e) to the extent, if any, that such Fund’s governing documents or other agreements limit the amount such Fund may commit to any one investment, such Fund’s Pro Rata Percentage of

the Commitment Amount is less than the maximum amount that such Fund is permitted to invest in any one portfolio investment pursuant to the terms of such governing documents or other agreements, (f) such Fund has uncalled capital commitments or

otherwise has available funds in excess of the sum of such Fund’s Pro Rata Percentage of the Commitment Amount hereunder plus the aggregate amount of all other commitments and obligations it currently has outstanding and (g) the execution,

delivery and performance by such Fund of this Agreement does not (i) violate such Fund’s agreement of limited partnership or other organizational documents, (ii) violate any Law or judgment applicable to it, or (iii) result in

any violation of, or default (with or without notice or lapse of time, or both) under, or give rise to a right of termination, cancellation or acceleration of any obligation or to the loss of any benefit under, any Contract to which it is a party,

except where such violation or default would not prevent such Fund’s ability to perform its obligations hereunder.

3

6. Parties in Interest; Enforceability. This Agreement (a) is solely for

the benefit of, and shall only be binding upon, the parties hereto and their respective successors and permitted assigns and (b) is not intended to, and does not, confer upon any other Person any benefits, rights or remedies, except that

(i) the Company is an express third-party beneficiary hereof solely in respect of (x) the Specific Performance Rights described in Section 3 of this Agreement and (y) the rights expressly provided for in

Sections 7 and 12 of this Agreement and (ii) each Non-Recourse Party is an express third-party beneficiary hereof and may rely upon and enforce the provisions of Sections 3 and

13 hereof. Neither Parent’s creditors nor any Person claiming by, through, or on behalf or for the benefit of Parent, the Company or any of their respective Affiliates shall have any right to enforce this Agreement or to cause Parent to

enforce this Agreement.

7. Amendment. No amendment, modification or waiver of any provision of this Agreement will be

enforceable unless approved in writing by Parent, the Funds and the Company. No failure or delay by any such Person in exercising any right, power or privilege in connection with this Agreement shall operate as a waiver thereof nor shall any single

or partial exercise thereof, preclude any other or further exercise thereof or the exercise of any other right, power or privilege, and no waiver of any of the provisions of this Agreement shall be deemed or shall constitute, a waiver of any other

provisions, whether or not similar, nor shall any waiver constitute a continuing waiver.

8. Termination. This Agreement and

all obligations of each Fund to fund its Pro Rata Percentage of the Commitment Amount will terminate automatically and immediately upon the earliest to occur of (a) the consummation of the Closing (at which time such obligations shall be

discharged) and the funding in full of the Commitment hereunder, subject to any reduction in accordance with Section 1 (at which time all such obligations shall be discharged), (b) any valid termination of the Merger Agreement pursuant to

Article VIII thereof, (c) payment by the Parent or the Guarantors (as defined in the Limited Guarantee) of any Guaranteed Obligations, subject to the Cap (as defined in the Limited Guarantee), and (d) the commencement of a claim by any

Company Related Party (or any Person claiming by, through or on behalf or for the benefit of any of the foregoing) against any Fund or any Non-Recourse Party under this Agreement, the Limited Guarantee or the

Merger Agreement (other than the Company asserting any Retained Claim against the applicable Non-Recourse Party(ies) to the extent such Retained Claim may be asserted pursuant to

Section 8 of the Limited Guarantee).

9. Headings; Construction. The descriptive headings contained

in this Agreement are for convenience of reference only and are not intended to be part of or to affect the meaning or interpretation of this Agreement. Each party acknowledges that it and its respective counsel have reviewed this Agreement and that

any rule of construction to the effect that any ambiguities are to be resolved against the drafting party shall not be employed in the interpretation of this Agreement.

10. Governing Law; Jurisdiction; Venue; Waiver of Jury Trial.

(a) This Agreement and all actions, proceedings, causes of action, claims or counterclaims (whether based on contract,

tort, statute or otherwise) based upon, arising

4

out of or relating to this Agreement or in the negotiation, administration, performance and enforcement thereof (including any claim or cause of action based upon, arising out of or related to

any representation or warranty made in connection with this Agreement or as an inducement to enter into this Agreement), shall be governed by, and construed in accordance with the Laws of the State of Delaware, including its statutes of limitations,

without giving effect to any choice or conflict of laws provision or rule (whether of the State of Delaware or any other jurisdiction) that would cause the application of the Laws, including any statutes of limitations, of any jurisdiction other

than the State of Delaware.

(b) Each of the parties to this Agreement (a) irrevocably consents to the service

of the summons and complaint and any other process (whether inside or outside the territorial jurisdiction of the Chosen Courts) in any Legal Proceeding relating to the Merger or this Agreement, for and on behalf of itself or any of its properties

or assets, in accordance with Section 9.2 of the Merger Agreement or in such other manner as may be permitted by applicable Law, and nothing in this Section 10 will affect the right of any Party to

serve legal process in any other manner permitted by applicable Law; (b) irrevocably and unconditionally consents and submits itself and its properties and assets in any Legal Proceeding to the exclusive general jurisdiction of the Court of

Chancery of the State of Delaware and any state appellate court therefrom within the State of Delaware (or, if the Court of Chancery of the State of Delaware declines to accept jurisdiction over a particular matter, any other state or federal court

within the State of Delaware) (the “Chosen Courts”) in the event that any dispute or controversy arises out of this Agreement or the transactions contemplated hereby; (c) agrees that it shall not attempt to deny or defeat such

personal jurisdiction by motion or other request for leave from any such court; (d) agrees that any Legal Proceeding arising in connection with this Agreement or the transactions contemplated hereby shall be brought, tried and determined only

in the Chosen Courts; (e) waives any objection that it may now or hereafter have to the venue of any such Legal Proceeding in the Chosen Courts or that such Legal Proceeding was brought in an inconvenient court and agrees not to plead or claim

the same; and (f) agrees that it shall not bring any Legal Proceeding relating to this Agreement or the transactions contemplated hereby in any court other than the Chosen Courts. Each of the parties to this Agreement agrees that a final

judgment in any Legal Proceeding in the Chosen Courts will be conclusive and may be enforced in other jurisdictions by suit on the judgment or in any other manner provided by applicable Law.

(c) EACH PARTY HERETO ACKNOWLEDGES AND AGREES THAT ANY CONTROVERSY THAT MAY ARISE PURSUANT TO THIS AGREEMENT IS LIKELY TO

INVOLVE COMPLICATED AND DIFFICULT ISSUES, AND THEREFORE EACH PARTY HEREBY IRREVOCABLY AND UNCONDITIONALLY WAIVES ANY RIGHT THAT SUCH PARTY MAY HAVE TO A TRIAL BY JURY IN RESPECT OF ANY LEGAL PROCEEDING (WHETHER FOR BREACH OF CONTRACT, TORTIOUS

CONDUCT OR OTHERWISE) DIRECTLY OR INDIRECTLY ARISING OUT OF OR RELATING TO THIS AGREEMENT. EACH PARTY ACKNOWLEDGES AND AGREES THAT (i) NO REPRESENTATIVE, AGENT OR ATTORNEY OF ANY OTHER PARTY HAS REPRESENTED, EXPRESSLY OR OTHERWISE, THAT SUCH

OTHER PARTY WOULD NOT, IN THE EVENT OF LITIGATION, SEEK TO ENFORCE THE FOREGOING WAIVER; (ii) IT

5

UNDERSTANDS AND HAS CONSIDERED THE IMPLICATIONS OF THIS WAIVER; (iii) IT MAKES THIS WAIVER VOLUNTARILY; AND (iv) IT HAS BEEN INDUCED TO ENTER INTO THIS AGREEMENT BY, AMONG OTHER THINGS,

THE MUTUAL WAIVERS AND CERTIFICATIONS IN THIS SECTION 10.

11. Entire Agreement; Integration. This

Agreement, the Merger Agreement, the Limited Guarantee and the Confidentiality Agreement constitute the entire agreement of the parties with respect to the subject matter hereof, and supersedes all prior agreements, understandings and statements,

written or oral, between the Funds or any of their Affiliates, on the one hand, and Parent or any of its Affiliates, on the other, with respect to the transactions contemplated hereby.

12. No Assignment. This Agreement, and any of the rights, interests or obligations hereunder, may not be assigned, in whole or in

part, by Parent or any Fund without the prior written consent of the Funds and the Company; provided, that, each Fund may assign all or a portion of its respective obligations to fund the Commitment Amount to any Person that agrees to assume

such Fund’s obligations hereunder or otherwise pursuant to and in compliance with the terms set forth in Section 1 hereof. The granting of such consent in a given instance shall be solely in the discretion of the Funds

and the Company and, if granted, shall not constitute a waiver of the requirement to obtain the Funds’ or the Company’s consent with respect to any subsequent assignment. Any purported assignment of this Agreement or the Commitment in

contravention of this Section 12 shall be void.

13. No Recourse against Affiliates, etc.

Notwithstanding anything that may be expressed or implied in this Agreement, by its acceptance hereof Parent covenants, acknowledges and agrees that (a) no Person other than each Fund (and their respective permitted assignees, if applicable)

shall have any obligation hereunder (whether of an equitable, contractual, tort, statutory or other nature), (b) notwithstanding that each Fund is a limited partnership, no recourse hereunder or under any documents or instruments delivered in

connection herewith may be sought or had against any Non-Recourse Party, whether by the enforcement of any judgment or assessment or by any legal or equitable proceeding or by virtue of any statute, regulation

or other applicable law, and (c) no liability whatsoever will attach to, be imposed on or otherwise be incurred by any Non-Recourse Party in connection with this Agreement for any obligation of each Fund

under this Agreement or in connection with the Commitment, or any claim based on, in respect of, or by reason of this Agreement or the Commitment; provided, however, that nothing in this Section 13 is intended

or shall be construed to limit the contractual obligations of each Fund under the Limited Guarantee or the contractual obligations of Parent under the Merger Agreement.

14. Counterparts. This Agreement may be executed in any number of counterparts (including by DocuSign or by .pdf delivered via

email), and each such counterpart when executed will be deemed an original instrument and all such counterparts shall together constitute one and the same agreement.

15. Pro Rata Percentage. Each party hereto acknowledges and agrees that (a) this Agreement is not intended to, and does not,

create any agency, partnership, fiduciary or joint venture relationship between or among any of the parties hereto and neither this Agreement nor any other document or agreement entered into by any party hereto relating to the subject matter hereof

shall be construed to suggest otherwise, (b) the obligations of each of the Funds under this

6

Agreement are solely contractual in nature and (c) the determination of each Fund was independent of each other. Notwithstanding anything to the contrary contained in this Agreement, the

liability of each Fund hereunder shall be several, not joint or joint and several, based upon its respective Pro Rata Percentage, and no Fund shall be obligated to contribute any amounts hereunder in excess of its Pro Rata Percentage of the

Commitment Amount. The “Pro Rata Percentage” of each Fund is as set forth below:

|

|

|

|

|

| Bain Capital Fund XIII, L.P. |

|

|

87.069 |

% |

| Bain Capital Fund (Lux) XIII, SCSp |

|

|

12.931 |

% |

16. Notices. All notices and other communications hereunder must be in writing and will be deemed

to have been duly delivered and received hereunder (i) four (4) Business Days after being sent by registered or certified mail, return receipt requested, postage prepaid; (ii) one Business Day after being sent for next Business Day

delivery, fees prepaid, via a reputable nationwide overnight courier service; or (iii) immediately upon delivery by electronic mail or by hand (with a written or electronic confirmation of delivery), in each case to the intended recipient as

set forth below:

If to the Funds:

Bain

Capital Fund XIII, L.P.

Bain Capital Fund (Lux) XIII, SCSp

c/o Bain Capital Private Equity, LP